Downloaded 1,809 times

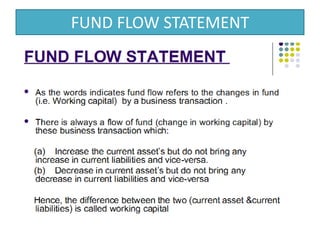

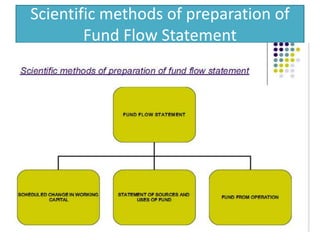

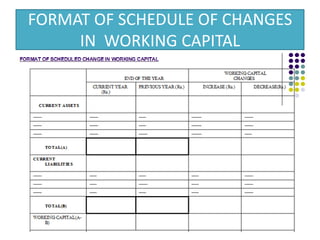

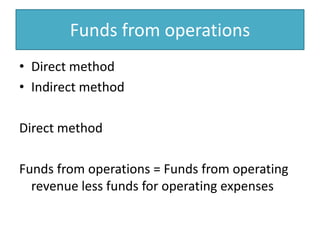

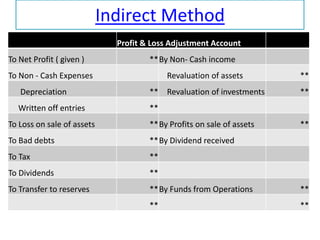

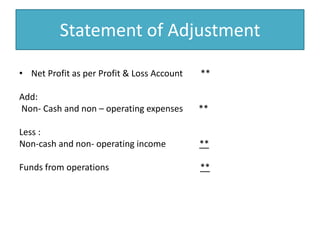

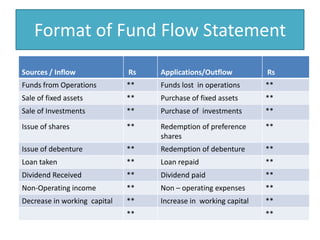

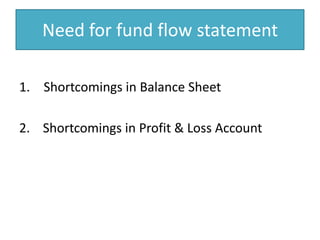

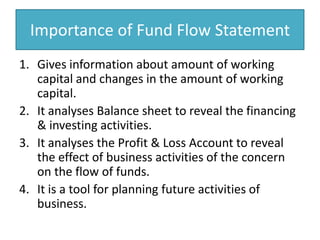

The document discusses the preparation and format of a fund flow statement. It explains that a fund flow statement can be prepared using either the direct method, which calculates funds from operations directly, or the indirect method, which makes adjustments to net profit in the income statement. The fund flow statement is important because it identifies changes in working capital and reveals how business activities have affected the flow of funds, providing useful information for planning future activities not shown in other financial statements.