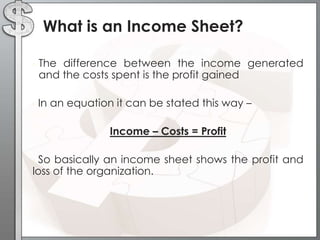

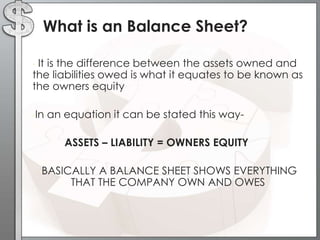

This presentation provides an overview of basic finance concepts including income sheets, balance sheets, and cash flow monitoring. It explains that an income sheet shows a company's profits and losses, a balance sheet shows the company's assets and liabilities, and a cash flow statement shows where a company's money comes from and goes. It also outlines steps for developing a budget, including setting goals, defining the budget's scope, quantifying assumptions, and building the budget. Tips are provided for top-down and bottom-up budgeting approaches.