Download to read offline

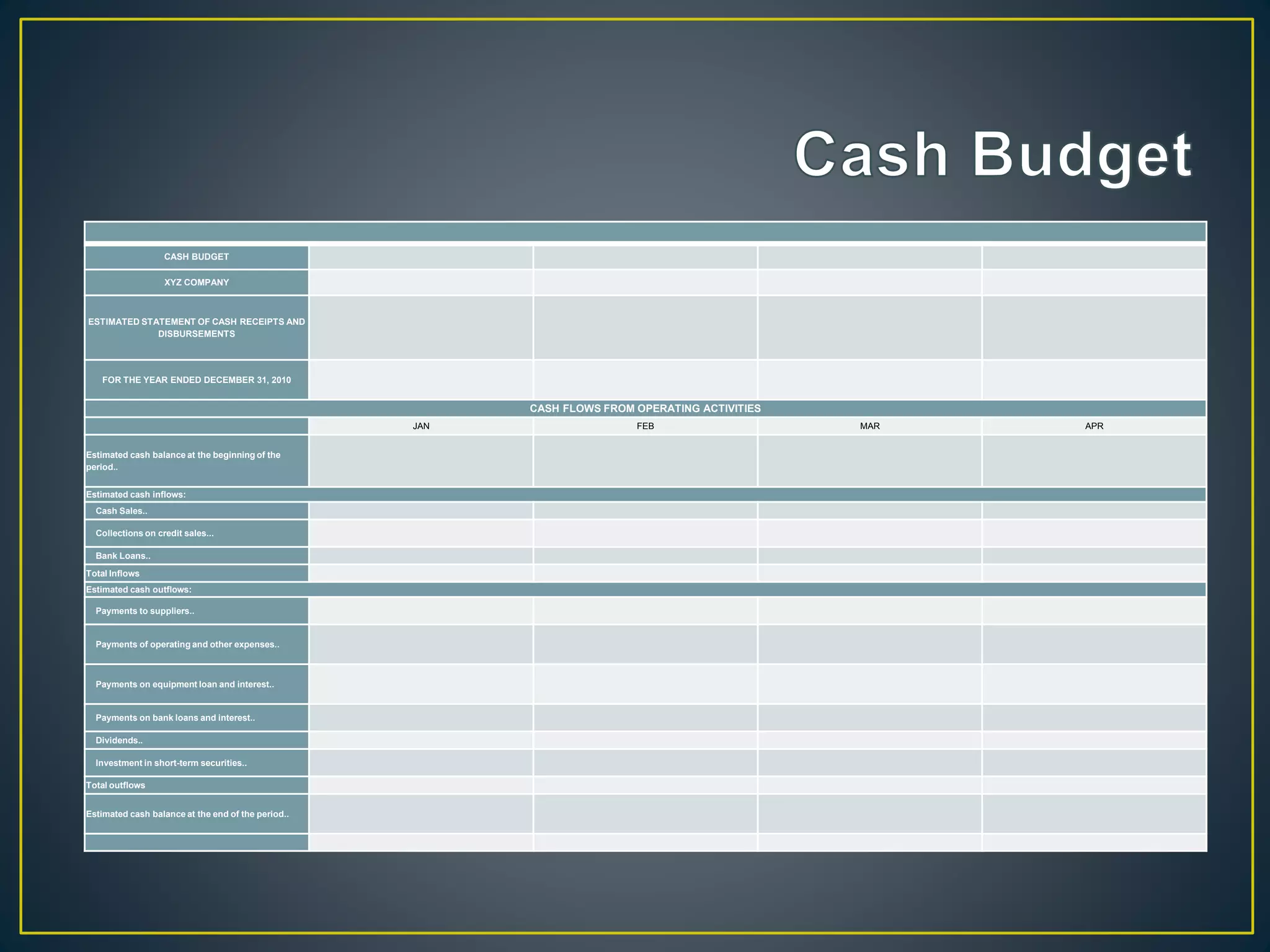

The document discusses the purpose and components of a cash budget. A cash budget projects sources and uses of cash over a future period to determine if a company will have enough cash to meet its needs. It contains a beginning cash balance as well as projected cash receipts from sales, collections, and asset sales. It also includes planned cash expenditures from budgets like materials, labor, overhead, selling and administration. The cash budget calculates any excess or deficiency and determines if additional financing is required.