Introduction to FinancialStatements

What is financial statement?

Financial statement is a structured representation of the

financial position (Balance Sheet), financial performance

(Income Statement) of an entity and the inflow and outflow

of cash (cash flow statement).

The objective of financial statements is to provide

information about

the financial position,

financial performance and

cash flows of an entity

Financial statements is also help to assess the probability

that an enterprise will be able to make future cash.

3.

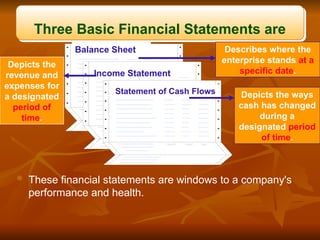

Three Basic FinancialStatements are

These financial statements are windows to a company's

performance and health.

Income Statement

Balance Sheet

Statement of Cash Flows

Describes where the

enterprise stands at a

specific date.

Depicts the

revenue and

expenses for

a designated

period of

time.

Depicts the ways

cash has changed

during a

designated period

of time.

4.

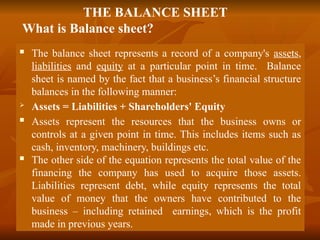

THE BALANCE SHEET

Whatis Balance sheet?

The balance sheet represents a record of a company's assets,

liabilities and equity at a particular point in time. Balance

sheet is named by the fact that a business’s financial structure

balances in the following manner:

Assets = Liabilities + Shareholders' Equity

Assets represent the resources that the business owns or

controls at a given point in time. This includes items such as

cash, inventory, machinery, buildings etc.

The other side of the equation represents the total value of the

financing the company has used to acquire those assets.

Liabilities represent debt, while equity represents the total

value of money that the owners have contributed to the

business – including retained earnings, which is the profit

made in previous years.

Why do weneed Balance sheet?

Because

Balance sheet provides investors with a snapshot of a company's

health as of the date provided on the financial statement.

If a company assets are large relative to liabilities, it's in

good shape. Conversely, if a company with a large amount of

liabilities relative to assets has risk to creditors.

The higher the debt ratio, the greater risk will be associated

with the firm's operation. In addition, high debt to assets ratio

may indicate low borrowing capacity of a firm, which in turn

will lower the firm's financial flexibility.

7.

THE INCOME STATEMENT

Whatis Income Statement?

The income statement shows an information about the

revenues, expenses and profit that was generated as a result

of the business' operations for that period and it measures a

company's performance over a specific time frame.

The components of income Statement are:

Revenue (how much the company earned)

Expenses (how much the company has spent)

Net Income before and after Tax (the profits of the

company)

8.

Because

Incomestatement answers the question, "How well

is the company's business?

“Does it performing well?

Basically, the question is "Is it making money?"

Firms with low expenses and high profits relative

to revenues are typically more desirable for

investment because it brings more money directly

to a shareholder.

Why do we need an Income Statement ?

9.

The statementof cash flows represents a record of a

business' cash inflows and outflows over a period of time.

It is the most sensitive statement and it focuses on the

following cash-related activities:

Operating Cash Flow: Cash generated from day-to-day

business operations.

Cash from Investing: Cash used for investing in assets,

as well as the proceeds from the sale of other

businesses, equipment or long-term assets

Cash from financing: Cash paid or received from the

issuing and borrowing of funds

THE STATEMENT OF CASH FLOWS

What is statement of cash flow?

10.

Statement ofcash flows is very important to investors, because

It shows how much actual cash a company has generated.

It shows the ability of firms to generate cash. Many

companies have shown “profits” on the income statement

but struggled later because of insufficient cash flows.

Because, the income statement includes non-cash revenues

or expenses, which the statement of cash flows excludes.

It shows correct figures of firms, because cash flow

statement is very difficult for a business to manipulate its

cash situation. Earnings can be manipulated, but it's tough to

“fake” cash in the bank. For this reason some investors use

the cash flow statement as a more conservative measure of

a company's performance.

Why do we need Statement of Cash Flows ?

11.

The threefinancial statements (Balance sheet, Income

statement and cash flow statement) are all related.

The changes of assets and liabilities that is indicated on

the balance sheet are also reflected in the revenues and

expenses which are stated on the income statement,

which shows the company’s gains or losses.

Cash flows provide more information about cash assets

listed on a balance sheet and are related, but not

equivalent, to net income shown on the income

statement.

Therefore, no one financial statement tells the

complete story of firms.

Bringing the financial statements All Together

12.

ACCOUNTING PRINCIPLES

Certain accountingprinciples that are

important for an understanding of

financial statements and how professional

judgment by accountants may affect the

application of those principles are shown in

the next slides

13.

The concept ofbusiness entity

ABC Company

A business entity is separated from

the personal affairs of its owner.

14.

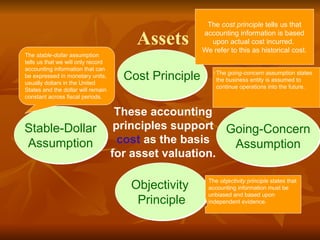

Assets

Cost Principle

Going-Concern

Assumption

Objectivity

Principle

Stable-Dollar

Assumption

These accounting

principlessupport

cost as the basis

for asset valuation.

The cost principle tells us that

accounting information is based

upon actual cost incurred.

We refer to this as historical cost.

The objectivity principle states that

accounting information must be

unbiased and based upon

independent evidence.

The stable-dollar assumption

tells us that we will only record

accounting information that can

be expressed in monetary units,

usually dollars in the United

States and the dollar will remain

constant across fiscal periods.

The going-concern assumption states

the business entity is assumed to

continue operations into the future.

15.

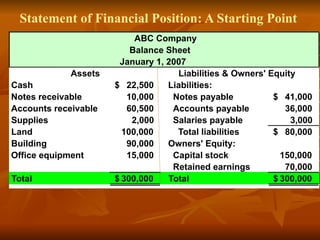

Statement of FinancialPosition: A Starting Point

ABC Company

Balance Sheet

January 1, 2007

Assets Liabilities & Owners' Equity

Cash 22,500

$ Liabilities:

Notes receivable 10,000 Notes payable 41,000

$

Accounts receivable 60,500 Accounts payable 36,000

Supplies 2,000 Salaries payable 3,000

Land 100,000 Total liabilities 80,000

$

Building 90,000 Owners' Equity:

Office equipment 15,000 Capital stock 150,000

Retained earnings 70,000

Total 300,000

$ Total 300,000

$

16.

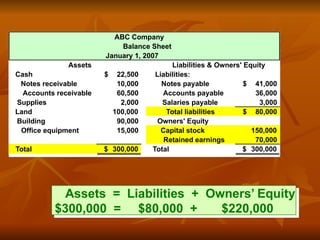

Assets = Liabilities+ Owners’ Equity

$300,000 = $80,000 + $220,000

ABC Company

Balance Sheet

January 1, 2007

Assets Liabilities & Owners' Equity

Cash 22,500

$ Liabilities:

Notes receivable 10,000 Notes payable 41,000

$

Accounts receivable 60,500 Accounts payable 36,000

Supplies 2,000 Salaries payable 3,000

Land 100,000 Total liabilities 80,000

$

Building 90,000 Owners' Equity

Office equipment 15,000 Capital stock 150,000

Retained earnings 70,000

Total 300,000

$ Total 300,000

$

17.

Business transactions affectthe elements

of the accounting equation:

Assets = Liabilities + Owners’ Equity

In the next slides will demonstrate how certain business

transactions affect the elements of the accounting equation

EXAMPLE TRANSACTION.ppt

18.

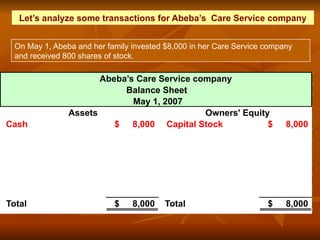

Let’s analyze sometransactions for Abeba’s Care Service company

On May 1, Abeba and her family invested $8,000 in her Care Service company

and received 800 shares of stock.

Abeba’s Care Service company

Balance Sheet

May 1, 2007

Assets

Cash 8,000

$ Capital Stock 8,000

$

Total 8,000

$ Total 8,000

$

Owners' Equity

19.

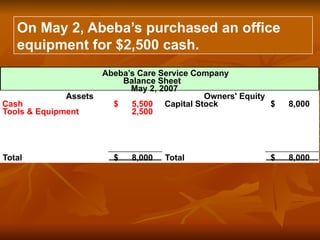

On May 2,Abeba’s purchased an office

equipment for $2,500 cash.

Abeba’s Care Service Company

Balance Sheet

May 2, 2007

Assets

Cash 5,500

$ Capital Stock 8,000

$

Tools & Equipment 2,500

Total 8,000

$ Total 8,000

$

Owners' Equity

20.

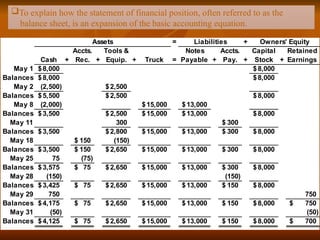

Assets = Liabilities+

Cash +

Accts.

Rec. +

Tools &

Equip. + Truck =

Notes

Payable +

Accts.

Pay. +

Capital

Stock +

Retained

Earnings

May 1 8,000

$ 8,000

$

Balances 8,000

$ 8,000

$

May 2 (2,500) 2,500

$

Balances 5,500

$ 2,500

$ 8,000

$

May 8 (2,000) 15,000

$ 13,000

$

Balances 3,500

$ 2,500

$ 15,000

$ 13,000

$ 8,000

$

May 11 300 300

$

Balances 3,500

$ 2,800

$ 15,000

$ 13,000

$ 300

$ 8,000

$

May 18 150

$ (150)

Balances 3,500

$ 150

$ 2,650

$ 15,000

$ 13,000

$ 300

$ 8,000

$

May 25 75 (75)

Balances 3,575

$ 75

$ 2,650

$ 15,000

$ 13,000

$ 300

$ 8,000

$

May 28 (150) (150)

Balances 3,425

$ 75

$ 2,650

$ 15,000

$ 13,000

$ 150

$ 8,000

$

May 29 750 750

Balances 4,175

$ 75

$ 2,650

$ 15,000

$ 13,000

$ 150

$ 8,000

$ 750

$

May 31 (50) (50)

Balances 4,125

$ 75

$ 2,650

$ 15,000

$ 13,000

$ 150

$ 8,000

$ 700

$

Owners' Equity

To explain how the statement of financial position, often referred to as the

balance sheet, is an expansion of the basic accounting equation.

21.

Assets = Liabilities+

Cash +

Accts.

Rec. +

Tools &

Equip. + Truck =

Notes

Payable +

Accts.

Pay. +

Capital

Stock +

Retained

Earnings

May 1 8,000

$ 8,000

$

Balances 8,000

$ 8,000

$

May 2 (2,500) 2,500

$

Balances 5,500

$ 2,500

$ 8,000

$

May 8 (2,000) 15,000

$ 13,000

$

Balances 3,500

$ 2,500

$ 15,000

$ 13,000

$ 8,000

$

May 11 300 300

$

Balances 3,500

$ 2,800

$ 15,000

$ 13,000

$ 300

$ 8,000

$

May 18 150

$ (150)

Balances 3,500

$ 150

$ 2,650

$ 15,000

$ 13,000

$ 300

$ 8,000

$

May 25 75 (75)

Balances 3,575

$ 75

$ 2,650

$ 15,000

$ 13,000

$ 300

$ 8,000

$

May 28 (150) (150)

Balances 3,425

$ 75

$ 2,650

$ 15,000

$ 13,000

$ 150

$ 8,000

$

May 29 750 750

Balances 4,175

$ 75

$ 2,650

$ 15,000

$ 13,000

$ 150

$ 8,000

$ 750

$

May 31 (50) (50)

Balances 4,125

$ 75

$ 2,650

$ 15,000

$ 13,000

$ 150

$ 8,000

$ 700

$

Owners' Equity

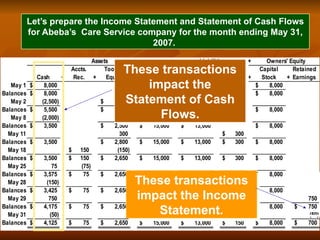

These transactions

impact the

Statement of Cash

Flows.

These transactions

impact the Income

Statement.

Let’s prepare the Income Statement and Statement of Cash Flows

for Abeba’s Care Service company for the month ending May 31,

2007.

22.

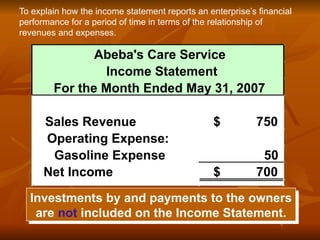

Investments by andpayments to the owners

are not included on the Income Statement.

To explain how the income statement reports an enterprise’s financial

performance for a period of time in terms of the relationship of

revenues and expenses.

Abeba's Care Service

Income Statement

For the Month Ended May 31, 2007

Sales Revenue 750

$

Operating Expense:

Gasoline Expense 50

Net Income 700

$

23.

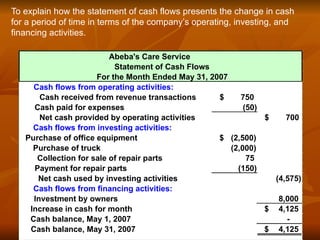

To explain howthe statement of cash flows presents the change in cash

for a period of time in terms of the company’s operating, investing, and

financing activities.

Abeba's Care Service

Statement of Cash Flows

For the Month Ended May 31, 2007

Cash flows from operating activities:

Cash received from revenue transactions 750

$

Cash paid for expenses (50)

Net cash provided by operating activities 700

$

Cash flows from investing activities:

Purchase of office equipment (2,500)

$

Purchase of truck (2,000)

Collection for sale of repair parts 75

Payment for repair parts (150)

Net cash used by investing activities (4,575)

Cash flows from financing activities:

Investment by owners 8,000

Increase in cash for month 4,125

$

Cash balance, May 1, 2007 -

Cash balance, May 31, 2007 4,125

$

24.

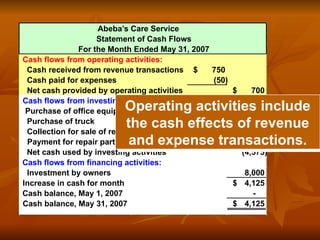

Abeba’s Care Service

Statementof Cash Flows

For the Month Ended May 31, 2007

Cash flows from operating activities:

Cash received from revenue transactions 750

$

Cash paid for expenses (50)

Net cash provided by operating activities 700

$

Cash flows from investing activities:

Purchase of office equipment (2,500)

$

Purchase of truck (2,000)

Collection for sale of repair parts 75

Payment for repair parts (150)

Net cash used by investing activities (4,575)

Cash flows from financing activities:

Investment by owners 8,000

Increase in cash for month 4,125

$

Cash balance, May 1, 2007 -

Cash balance, May 31, 2007 4,125

$

Operating activities include

the cash effects of revenue

and expense transactions.

25.

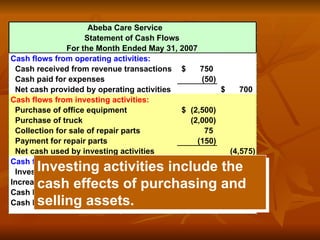

Abeba Care Service

Statementof Cash Flows

For the Month Ended May 31, 2007

Cash flows from operating activities:

Cash received from revenue transactions 750

$

Cash paid for expenses (50)

Net cash provided by operating activities 700

$

Cash flows from investing activities:

Purchase of office equipment (2,500)

$

Purchase of truck (2,000)

Collection for sale of repair parts 75

Payment for repair parts (150)

Net cash used by investing activities (4,575)

Cash flows from financing activities:

Investment by owners 8,000

Increase in cash for month 4,125

$

Cash balance, May 1, 2007 -

Cash balance, May 31, 2007 4,125

$

Investing activities include the

cash effects of purchasing and

selling assets.

26.

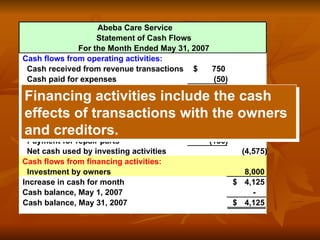

Abeba Care Service

Statementof Cash Flows

For the Month Ended May 31, 2007

Cash flows from operating activities:

Cash received from revenue transactions 750

$

Cash paid for expenses (50)

Net cash provided by operating activities 700

$

Cash flows from investing activities:

Purchase of office equipment (2,500)

$

Purchase of truck (2,000)

Collection for sale of repair parts 75

Payment for repair parts (150)

Net cash used by investing activities (4,575)

Cash flows from financing activities:

Investment by owners 8,000

Increase in cash for month 4,125

$

Cash balance, May 1, 2007 -

Cash balance, May 31, 2007 4,125

$

Financing activities include the cash

effects of transactions with the owners

and creditors.

27.

Assets = Liabilities+

Cash +

Accts.

Rec. +

Tools &

Equip. + Truck =

Notes

Payable +

Accts.

Pay. +

Capital

Stock +

Retained

Earnings

May 1 8,000

$ 8,000

$

Balances 8,000

$ 8,000

$

May 2 (2,500) 2,500

$

Balances 5,500

$ 2,500

$ 8,000

$

May 8 (2,000) 15,000

$ 13,000

$

Balances 3,500

$ 2,500

$ 15,000

$ 13,000

$ 8,000

$

May 11 300 300

$

Balances 3,500

$ 2,800

$ 15,000

$ 13,000

$ 300

$ 8,000

$

May 18 150

$ (150)

Balances 3,500

$ 150

$ 2,650

$ 15,000

$ 13,000

$ 300

$ 8,000

$

May 25 75 (75)

Balances 3,575

$ 75

$ 2,650

$ 15,000

$ 13,000

$ 300

$ 8,000

$

May 28 (150) (150)

Balances 3,425

$ 75

$ 2,650

$ 15,000

$ 13,000

$ 150

$ 8,000

$

May 29 750 750

Balances 4,175

$ 75

$ 2,650

$ 15,000

$ 13,000

$ 150

$ 8,000

$ 750

$

May 31 (50) (50

Balances 4,125

$ 75

$ 2,650

$ 15,000

$ 13,000

$ 150

$ 8,000

$ 700

$

Owners' Equity

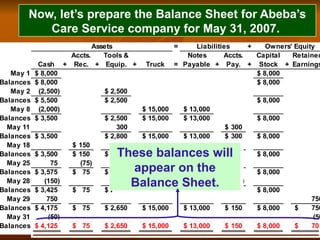

Now, let’s prepare the Balance Sheet for Abeba’s

Care Service company for May 31, 2007.

These balances will

appear on the

Balance Sheet.

28.

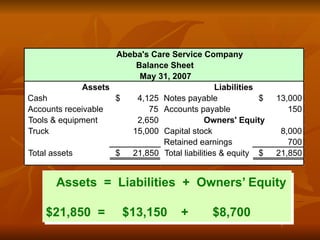

Assets = Liabilities+ Owners’ Equity

$21,850 = $13,150 + $8,700

Cash 4,125

$ Notes payable 13,000

$

Accounts receivable 75 Accounts payable 150

Tools & equipment 2,650

Truck 15,000 Capital stock 8,000

Retained earnings 700

Total assets 21,850

$ Total liabilities & equity 21,850

$

Assets Liabilities

Owners' Equity

Abeba's Care Service Company

Balance Sheet

May 31, 2007

29.

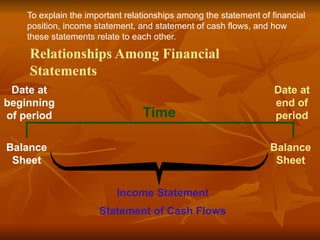

Relationships Among Financial

Statements

Dateat

beginning

of period

Date at

end of

period

Balance

Sheet

Balance

Sheet

Time

Income Statement

Statement of Cash Flows

To explain the important relationships among the statement of financial

position, income statement, and statement of cash flows, and how

these statements relate to each other.

30.

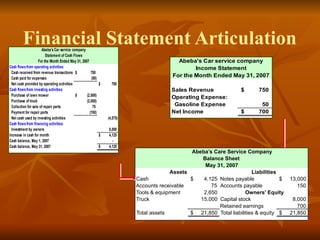

Financial Statement Articulation

Abeba'sCar service company

Statement of Cash Flows

For the Month Ended May 31, 2007

Cash flowsfrom operating activities:

Cash received from revenue transactions 750

$

Cash paid for expenses (50)

Net cash provided by operating activities 700

$

Cash flowsfrom investing activities:

Purchase of lawn mower (2,500)

$

Purchase of truck (2,000)

Collection for sale of repair parts 75

Payment for repair parts (150)

Net cash used by investing activities (4,575)

Cash flowsfrom financing activities:

Investment by owners 8,000

Increase in cash for month 4,125

$

Cash balance, May 1, 2007 -

Cash balance, May 31, 2007 4,125

$

Abeba's Car service company

Income Statement

Sales Revenue 750

$

Operating Expense:

Gasoline Expense 50

Net Income 700

$

For the Month Ended May 31, 2007

Cash 4,125

$ Notes payable 13,000

$

Accounts receivable 75 Accounts payable 150

Tools & equipment 2,650

Truck 15,000 Capital stock 8,000

Retained earnings 700

Total assets 21,850

$ Total liabilities & equity 21,850

$

Assets Liabilities

Owners' Equity

Abeba’s Care Service Company

Balance Sheet

May 31, 2007

31.

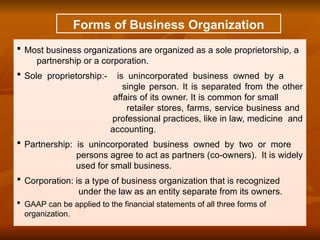

Forms of BusinessOrganization

Sole

Proprietorships Partnerships Corporations

32.

Forms of BusinessOrganization

Most business organizations are organized as a sole proprietorship, a

partnership or a corporation.

Sole proprietorship:- is unincorporated business owned by a

single person. It is separated from the other

affairs of its owner. It is common for small

retailer stores, farms, service business and

professional practices, like in law, medicine and

accounting.

Partnership: is unincorporated business owned by two or more

persons agree to act as partners (co-owners). It is widely

used for small business.

Corporation: is a type of business organization that is recognized

under the law as an entity separate from its owners.

GAAP can be applied to the financial statements of all three forms of

organization.

33.

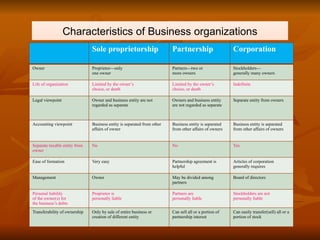

Characteristics of Businessorganizations

Sole proprietorship Partnership Corporation

Owner Proprietor—only

one owner

Partners—two or

more owners

Stockholders—

generally many owners

Life of organization Limited by the owner’s

choice, or death

Limited by the owner’s

choice, or death

Indefinite

Legal viewpoint Owner and business entity are not

regarded as separate

Owners and business entity

are not regarded as separate

Separate entity from owners

Accounting viewpoint Business entity is separated from other

affairs of owner

Business entity is separated

from other affairs of owners

Business entity is separated

from other affairs of owners

Separate taxable entity from

owner

No No Yes

Ease of formation Very easy Partnership agreement is

helpful

Articles of corporation

generally requires

Management Owner May be divided among

partners

Board of directors

Personal liability

of the owner(s) for

the business’s debts

Proprietor is

personally liable

Partners are

personally liable

Stockholders are not

personally liable

Transferability of ownership Only by sale of entire business or

creation of different entity

Can sell all or a portion of

partnership interest

Can easily transfer(sell) all or a

portion of stock

34.

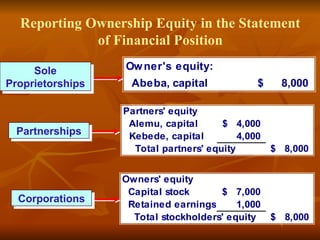

Reporting Ownership Equityin the Statement

of Financial Position

Owner's equity:

Abeba, capital 8,000

$

Sole

Proprietorships

Partners' equity

Alemu, capital 4,000

$

Kebede, capital 4,000

Total partners' equity 8,000

$

Partnerships

Owners' equity

Capital stock 7,000

$

Retained earnings 1,000

Total stockholders' equity 8,000

$

Corporations

Editor's Notes

#3 There are three fundamental financial statements used in accounting.

The income statement shows revenues and expenses.

The balance sheet is a listing of all asset, liability, and equity account balances that do not appear on the income statement.

The statement of cash flows shows how the company receives and spends its cash.

#11 All the financial statements are interrelated. We can start with the balance sheet at the beginning of an accounting period, analyze the income and cash flows of the company, and arrive at the ending balances that will appear on the balance sheet.

#13 The business entity principle states that the transactions of individual owners of a business and those of the business must be separate.

#14 The cost principle tells us that accounting information is based upon actual cost incurred. We refer to this as historical cost.

The going-concern assumption states that in the absence of information to the contrary, the business entity is assumed to continue operations into the foreseeable future.

The objectivity principle states that accounting information must be unbiased and based upon independent evidence.

The stable-dollar assumption tells us that we will only record accounting information that can be expressed in monetary units, usually dollars in the United States.

#15 The balance sheet is an inventory of assets, liabilities, and equity at the end of the month. Our total assets are equal to three hundred thousand dollars. This includes cash of twenty-two thousand five hundred dollars, notes receivable of ten thousand dollars, supplies of two thousand dollars, and the balances in the remaining asset accounts.

Liabilities include notes payable of forty-one thousand, accounts payable of thirty-six thousand and salaries payable of three thousand dollars. The accounts in the owners’ equity section of the balance sheet are capital stock of one hundred-fifty thousand dollars and retained earnings of seventy thousand dollars.

Notice that the total assets are equal to the total liabilities plus owners’ equity.

#16 The basic accounting equation states that assets are equal to liabilities plus equity of a company. The equation makes sense because it states that assets must be equal to the claims against those assets.

There are two broad categories of claims against an asset: Claims by creditors (called liabilities), or after all creditor claims are satisfied, the residual owners (the stockholders) have a claim on those assets.

#18 Part I

On May 1st, Jill Jones and her family invested $8,000 in JJ’s Lawn Care Service and received 800 shares of stock in return. Let’s see how the balance sheet would look immediately after this transaction.

Part II

The cash account of JJ’s Lawn Care increased by eight thousand dollars and the capital stock of the company also increased by eight thousand dollars. Notice that the basic accounting equation is in balance. Total assets are equal to total liabilities plus owners’ equity.

#19 Part I

On the 2nd of May, JJ’s Lawn Care purchased a riding lawn mower for $2,500 cash. Let’s see how the balance sheet looks now.

Part II

The cash account has been reduced by the $2,500 spent and the tools and equipment account has been increased by the same amount. One asset, cash, was merely traded for another, the riding lawn mower. Owners’ equity is not changed by the transaction and the basic accounting equation is still in balance.

#20 All of these transactions have been placed on this slide, in the appropriate columns for the accounts they’ve impacted. Let’s verify the balance in each account and get ready to prepare the financial statements for JJ’s Lawn Care.

#21 Part I

All of the transactions that impacted the cash account will appear on the statement of cash flows.

Part II

The revenues and expenses that caused the change in retained earnings will appear on the income statement of the company.

Part II

Let’s begin by preparing the income statement and statement of cash flows for JJ’s Lawn Care for the period ended May 31, 2007.

#22 Part I

JJ’s Lawn care has one revenue for services for $750, and one expense for gasoline of $50. So the net income for the month of May is $700. Remember, net income is the excess of revenues over expenses incurred during the accounting period.

Part II

Investments by owners and payments to owners do not appear on the income statement. These amounts appear on the company’s balance sheet.

#23 Here is the statement of cash flows for JJ’s Lawn Care for the month ended May 31, 2007. Notice the three sections of the statement. If there was beginning balance for cash this balance should be add with the balance of cash change during the period and the result will be its ending cash balance for that period.

#24 Cash flows from operating activities include the $700 in net income calculated on the previous screen.

#25 JJ’s had a cash outflow for investing activities. The company invested in the riding lawn mower, truck, and repair parts; however, the company recovered some of the cost of repair parts by selling them to ABC Lawns.

#26 The only financing activity was the original investment by the owners of JJ’s Lawn Care.

The cash inflows and outflows resulted in an increase in cash of $4,125 during the month. Because the cash account had a zero balance at the beginning of the month, the ending balance in the cash account is $4,125.

Let’s finish by preparing the balance sheet for JJ’s Lawn Care.

#27 Here are the account balances to use when preparing the balance sheet.

#28 Part I

Asset accounts are listed on the left side of the balance sheet and the liabilities and owners’ equity accounts on the right.

Feel free to go back to the previous screen and see all the account balances that appear on the balance sheet.

Part II

As a final check, make sure that the accounting equation is still in balance. The total assets of $21,850 is exactly equal to the total of the company’s liabilities plus owners’ equity. Notice that the balance sheet lists all assets, liabilities, and equities on a certain date. In this example, the date is May 31, 2007.

#29 All the financial statements are interrelated. We can start with the balance sheet at the beginning of an accounting period, analyze the income and cash flows of the company, and arrive at the ending balances that will appear on the balance sheet.

Let’s see how this works in the JJ’s Lawn Care example.

#30 Part I

This is the balance sheet for JJ’s Lawn Care at the end of May.

Part II

Net income impacts the retained earnings of the company.

Part III

The statement of cash flows not only provides the balance in the cash account, but also details information about the acquisition and disposition of assets and liabilities as well as changes in the owners’ equity balance. It’s clear to see how all the financial statements articulate with each other.

#31 There are three general forms of business operations.

A proprietorship is a business owned by just one individual.

A partnership is owned by two or more individuals. Some partnerships have several thousand partners.

A corporation is owned by individuals who normally are not active in the day-to-day operations of that business. For example, you may become an owner of IBM by purchasing shares of stock on the New York Stock Exchange. While you are a part owner, you do not necessarily work for IBM nor are you active in the operations of the company.

#34 Part I

The owners’ equity section of the balance sheet will look different for each type of business entity. For a sole proprietorship, there will be a capital account for the owner, and a drawing account to record payments to the owner.

Part II

For a partnership, each partner has a separate account, where changes are tracked over time. There’s also a separate drawing account for payments made to each partner.

Part II

To review, a corporation will show owners’ contributions in the capital stock account and accumulated earnings of the company in the retained earnings account.

You should be able to tell the form of business by looking at the equity section of a balance sheet.