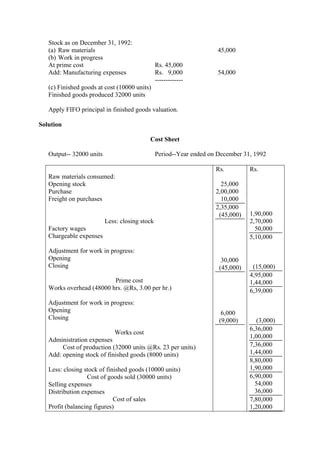

Downloaded 794 times

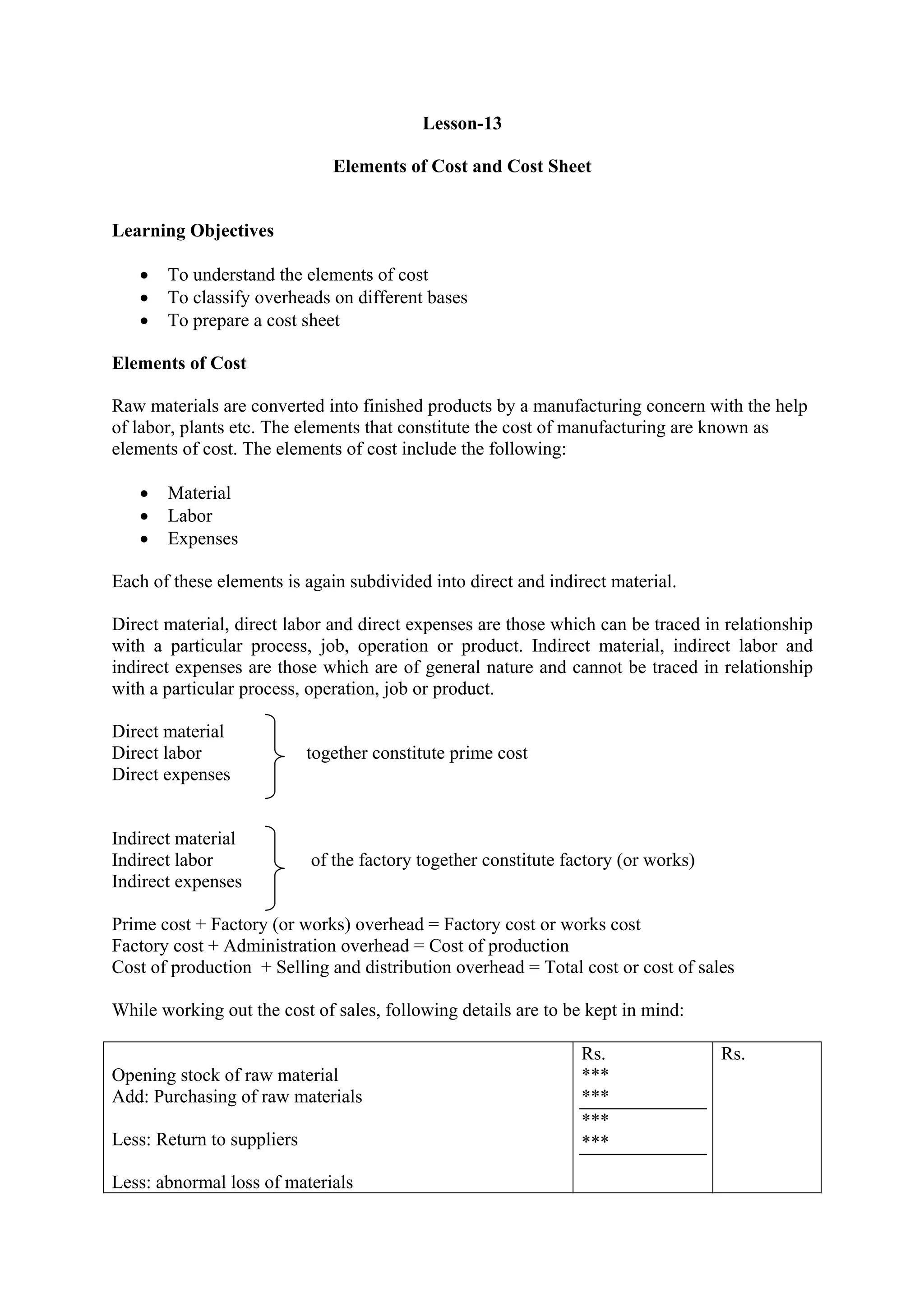

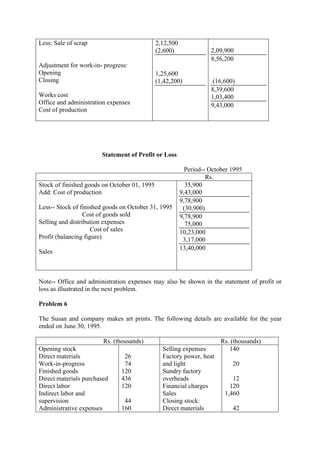

![Other data are:

Selling expenses

General and administration expenses

Sales for the month

Rs.

3,500

2,500

75,000

You are required to:

(i) Compute the value of raw material purchased.

(ii) Prepare a cost statement showing the various elements of cost and also the profit

earned.

Solution

(i) Statement Computing the Value of Raw Materials Purchased

Cost of goods sold

Add: closing stock of finished goods

Less: opening stock of finished goods

Works cost of cost of production

Add: closing stock of work in progress

Less: opening stock of work in progress

Less: works overhead (100/175 x direct labor, i.e. 100/175x17500)

Prime cost

Less: direct labor

Raw materials consumed

Add: closing stock of raw materials

Less: opening stock of raw materials

Values of raw material purchased

Rs.

56,000

19,000

75,000

(17,600)

57,400

14,500

71,900

(10,500)

61,400

(10,000)

51,400

(17,500)

33,900

10,600

44,500

(8,000)

36,500

(ii) Cost Statement

Period-- April 1992

Raw materials consumed [as in (i) above]

Direct labor

Prime labor

Works overhead

Adjustment for work in progress:

Opening 10,500

Closing (14,500)

------------

Works cost or cost of production

Rs.

33,900

17,500

51,400

10,000

61,400

(4,000)

57,400](https://image.slidesharecdn.com/elementsofcostsheet-140705050104-phpapp01/85/Elements-of-cost-sheet-22-320.jpg)

The document outlines the elements of cost in manufacturing, detailing direct and indirect costs including materials, labor, and various overhead expenses. It also classifies costs into fixed, variable, and semi-variable categories, emphasizing the importance of understanding cost behavior for accurate financial analysis. Multiple problem examples illustrate how to prepare cost sheets and analyze manufacturing costs.