Meaning, Nature AndScope Of Cost Accounting. Differentiate

Cost Accounting From Management Accounting And Financial

Accounting. Cost Concepts And Numerical On Preparation Of

Cost Sheet. Type Of Cost And Role Of Cost In Decision Making.

3.

Cost Accounting IsA Branch Of Accounting Focused On Capturing, Analyzing, And Controlling

A Company’s Costs. It Involves Recording All Costs Associated With Production, Operation, Or

Services, Such As Material, Labor, And Overhead. The Primary Objective Is To Determine The

Cost Of Goods Or Services, Aiding Management In Pricing, Budgeting, And Decision-making.

Cost Accounting Methods, Like Job Costing, Process Costing, And Activity-based Costing,

Provide Insights Into Cost Behavior And Profitability. By Identifying Inefficiencies And Cost-

saving Opportunities, It Supports Effective Financial Planning And Control.

COST ACCOUNTING

4.

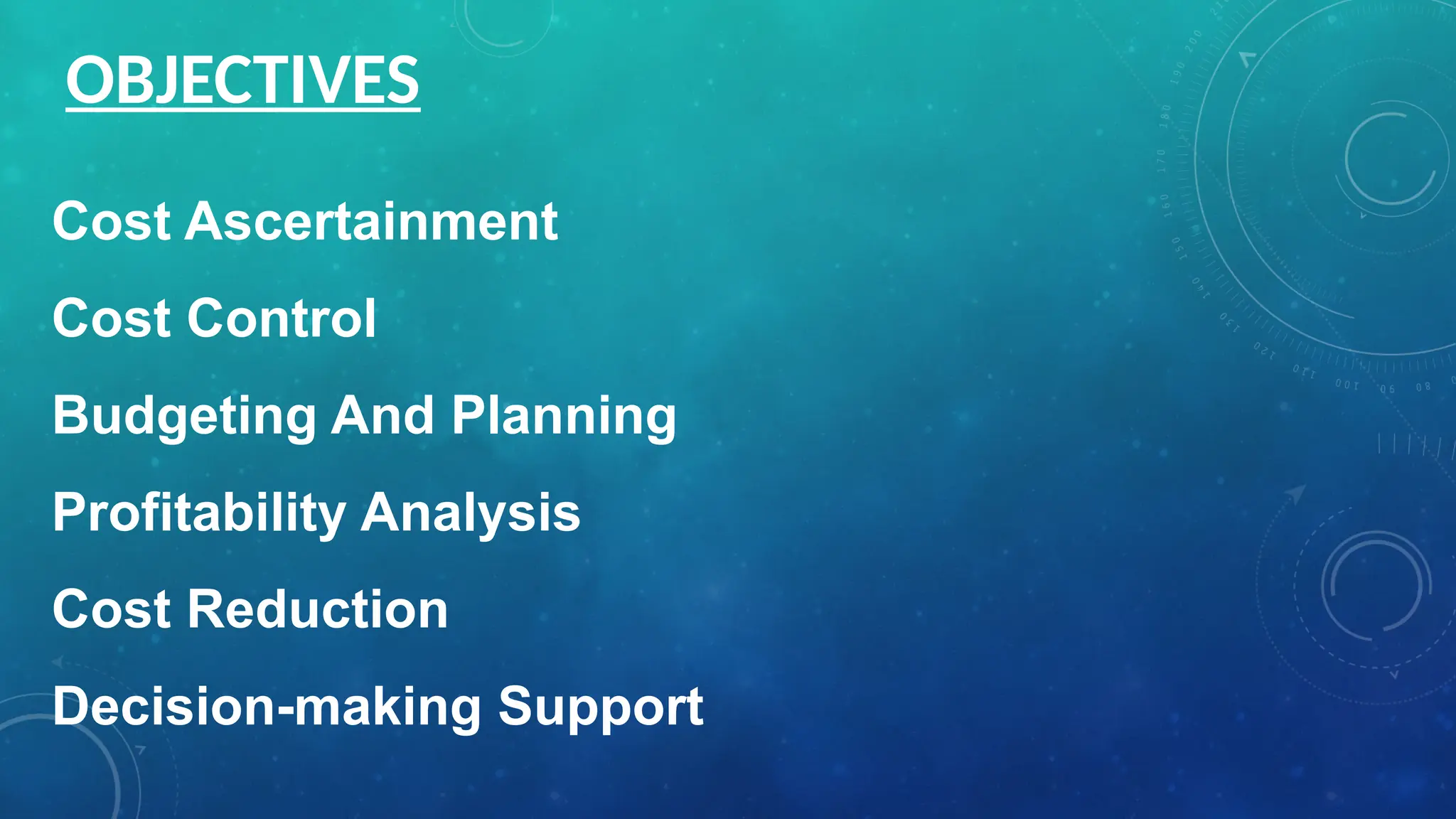

1.Cost Ascertainment AndClassification

2. Cost Control And Monitoring

3. Cost Reduction

4.Budgeting And Forecasting

5. Profitability Analysis

6. Decision-making Support

SCOPE OF COST ACCOUNTING

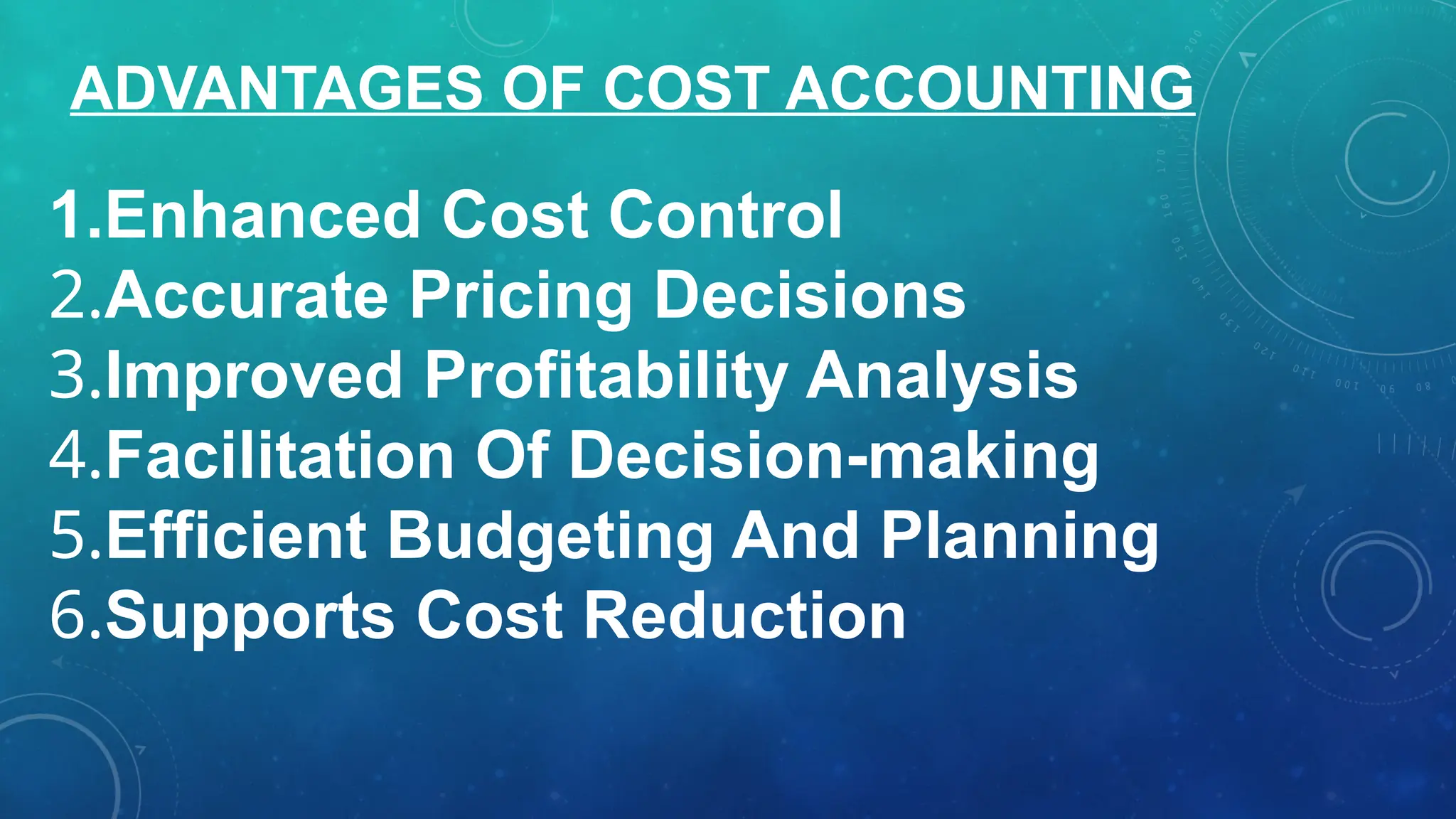

1.Enhanced Cost Control

2.AccuratePricing Decisions

3.Improved Profitability Analysis

4.Facilitation Of Decision-making

5.Efficient Budgeting And Planning

6.Supports Cost Reduction

ADVANTAGES OF COST ACCOUNTING

7.

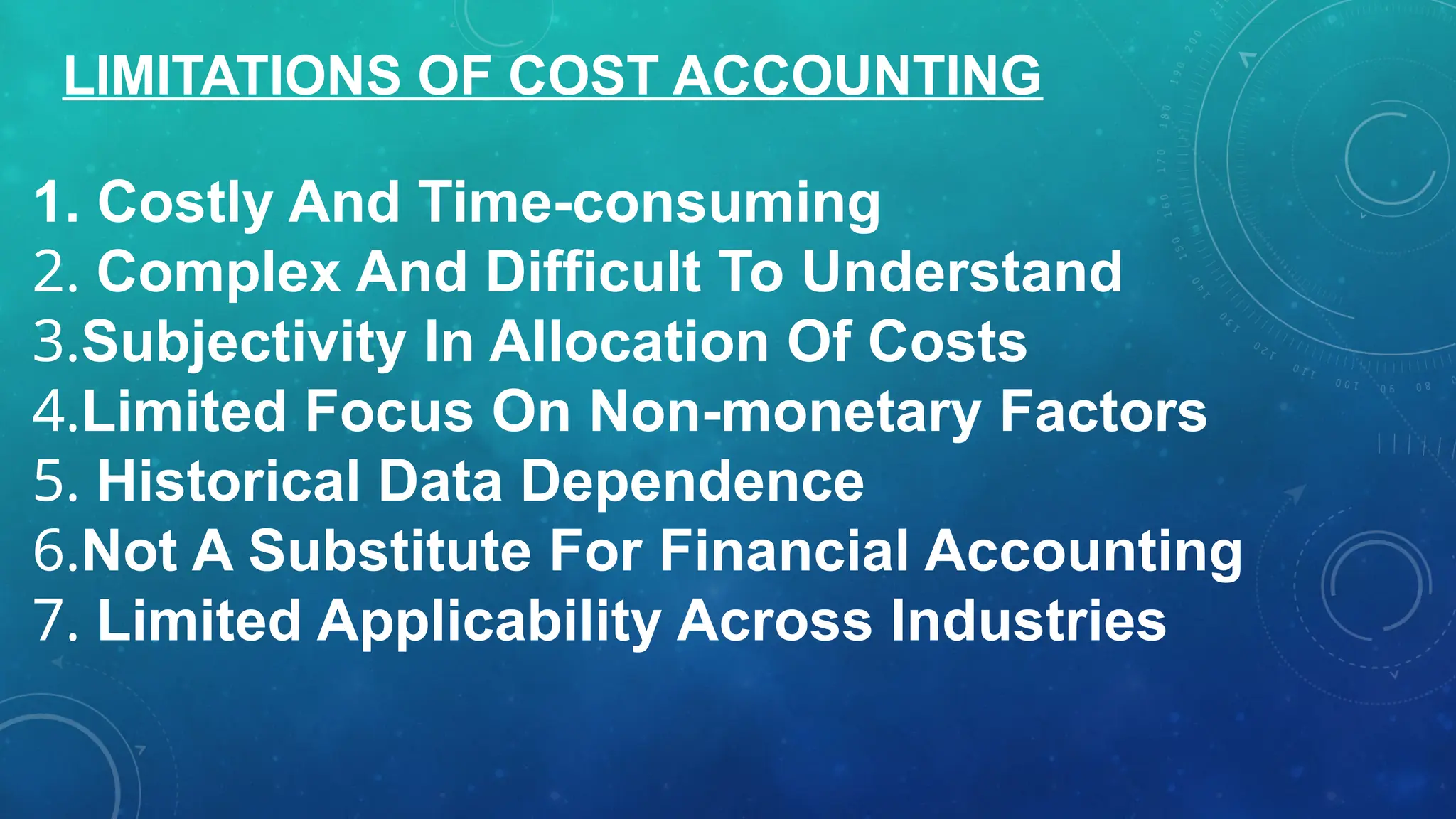

1. Costly AndTime-consuming

2. Complex And Difficult To Understand

3.Subjectivity In Allocation Of Costs

4.Limited Focus On Non-monetary Factors

5. Historical Data Dependence

6.Not A Substitute For Financial Accounting

7. Limited Applicability Across Industries

LIMITATIONS OF COST ACCOUNTING

8.

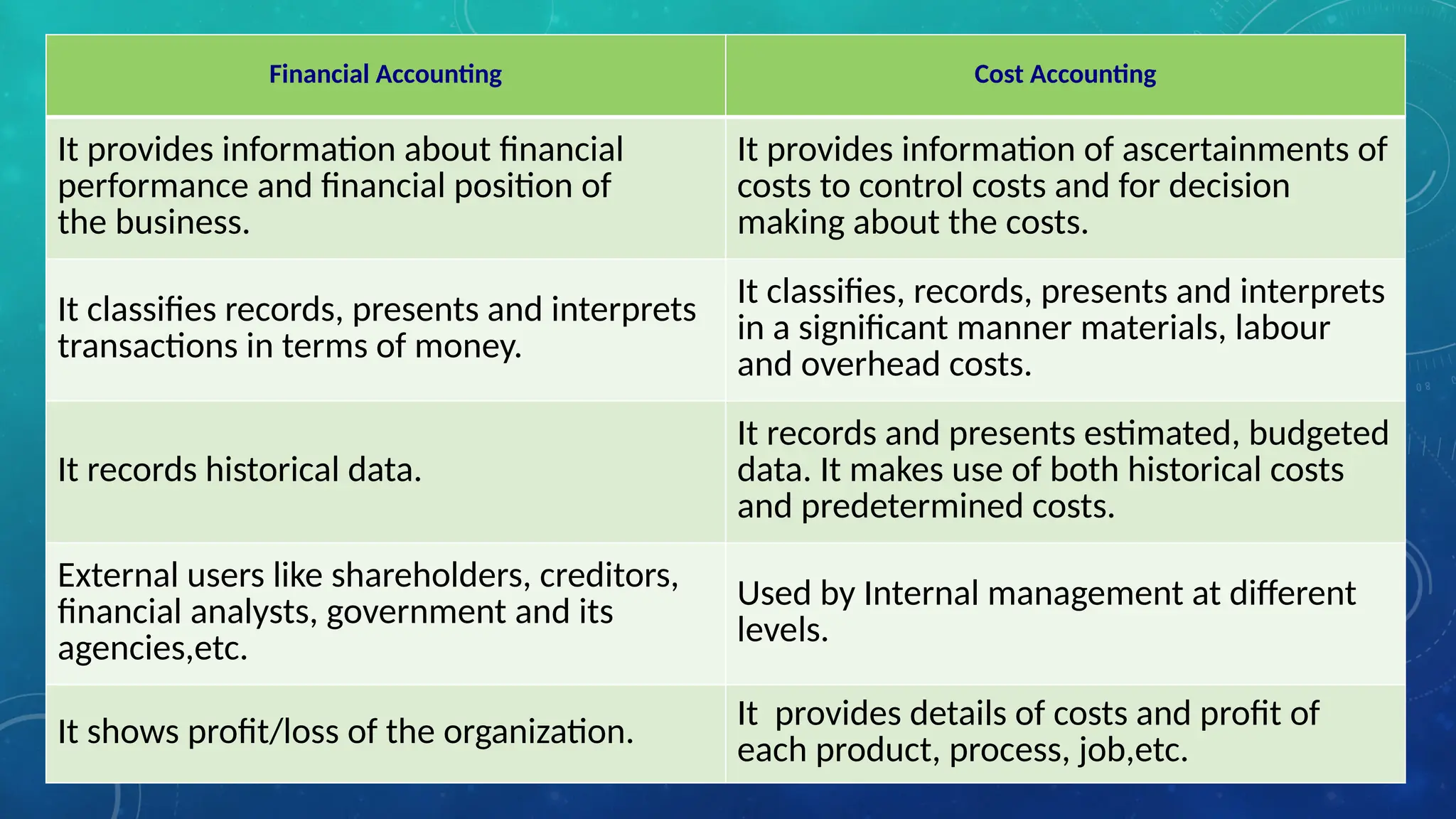

Financial Accounting CostAccounting

It provides information about financial

performance and financial position of

the business.

It provides information of ascertainments of

costs to control costs and for decision

making about the costs.

It classifies records, presents and interprets

transactions in terms of money.

It classifies, records, presents and interprets

in a significant manner materials, labour

and overhead costs.

It records historical data.

It records and presents estimated, budgeted

data. It makes use of both historical costs

and predetermined costs.

External users like shareholders, creditors,

financial analysts, government and its

agencies,etc.

Used by Internal management at different

levels.

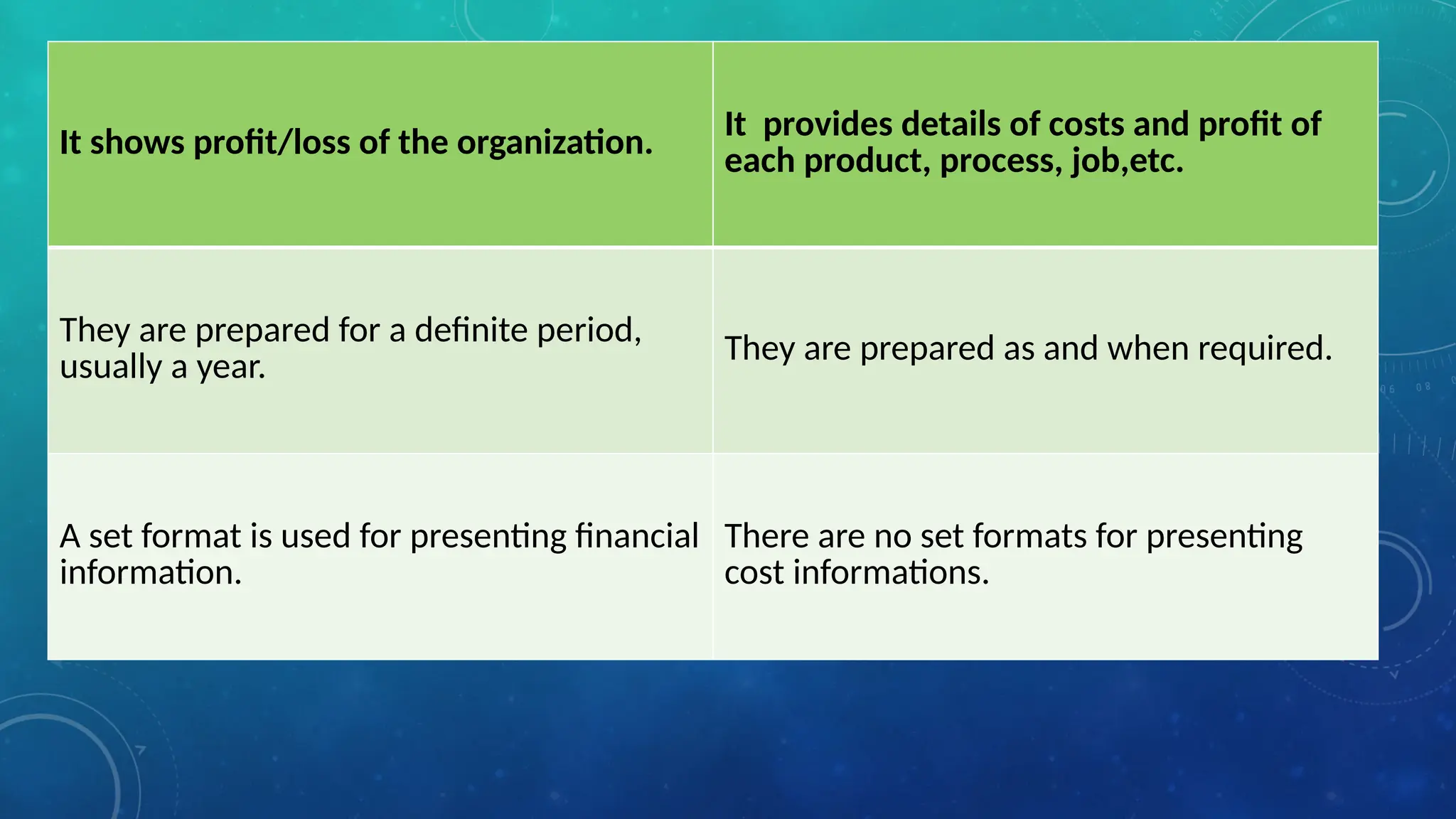

It shows profit/loss of the organization.

It provides details of costs and profit of

each product, process, job,etc.

9.

It shows profit/lossof the organization.

It provides details of costs and profit of

each product, process, job,etc.

They are prepared for a definite period,

usually a year.

They are prepared as and when required.

A set format is used for presenting financial

information.

There are no set formats for presenting

cost informations.

10.

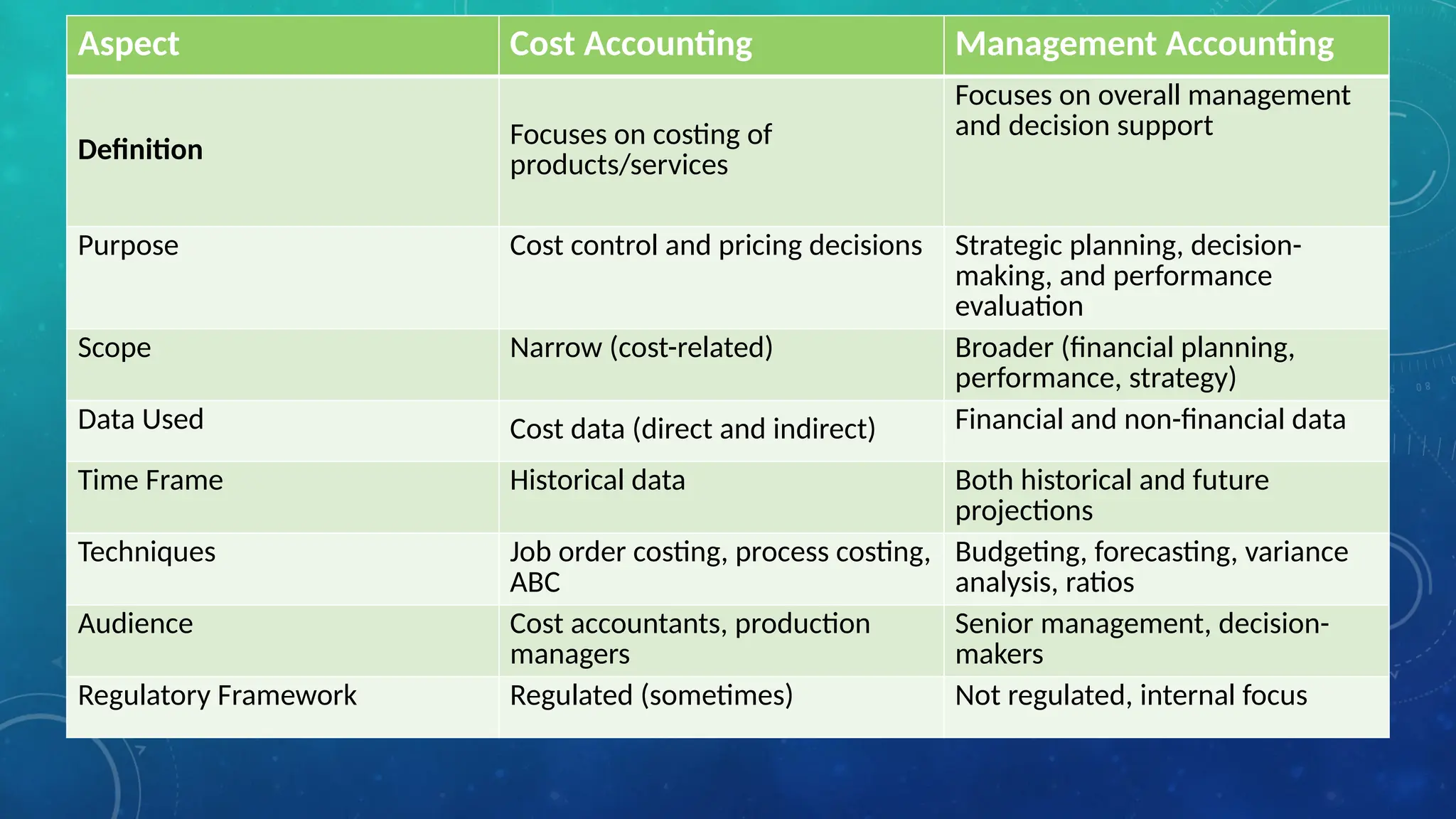

Aspect Cost AccountingManagement Accounting

Definition Focuses on costing of

products/services

Focuses on overall management

and decision support

Purpose Cost control and pricing decisions Strategic planning, decision-

making, and performance

evaluation

Scope Narrow (cost-related) Broader (financial planning,

performance, strategy)

Data Used Cost data (direct and indirect) Financial and non-financial data

Time Frame Historical data Both historical and future

projections

Techniques Job order costing, process costing,

ABC

Budgeting, forecasting, variance

analysis, ratios

Audience Cost accountants, production

managers

Senior management, decision-

makers

Regulatory Framework Regulated (sometimes) Not regulated, internal focus

12.

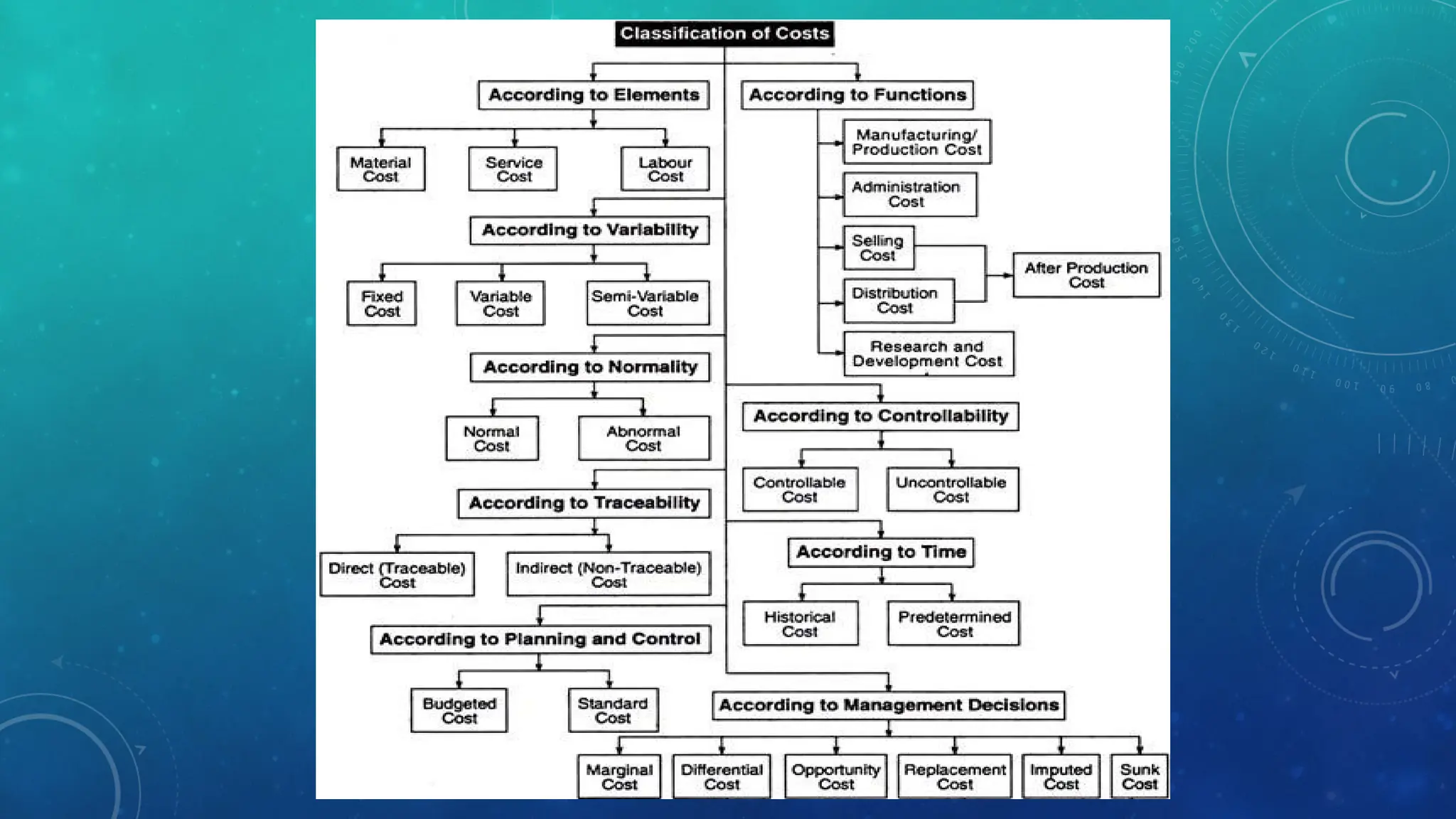

TYPES OF COST

DirectCost

Direct costs can be easily identified as per the expenditure on cost objects. So, for example, if we pick how much expenditure a

business has had on purchasing the raw materials inventory, we will be able to directly point out.

Indirect Cost

In the case of indirect costs, the challenge is that we can’t identify the costs as per the cost object. So, for example, if we try to

understand how much rent is given for sitting the machinery in a place, we won’t be able to do it because the rent is paid for the

entire space, not for a particular place.

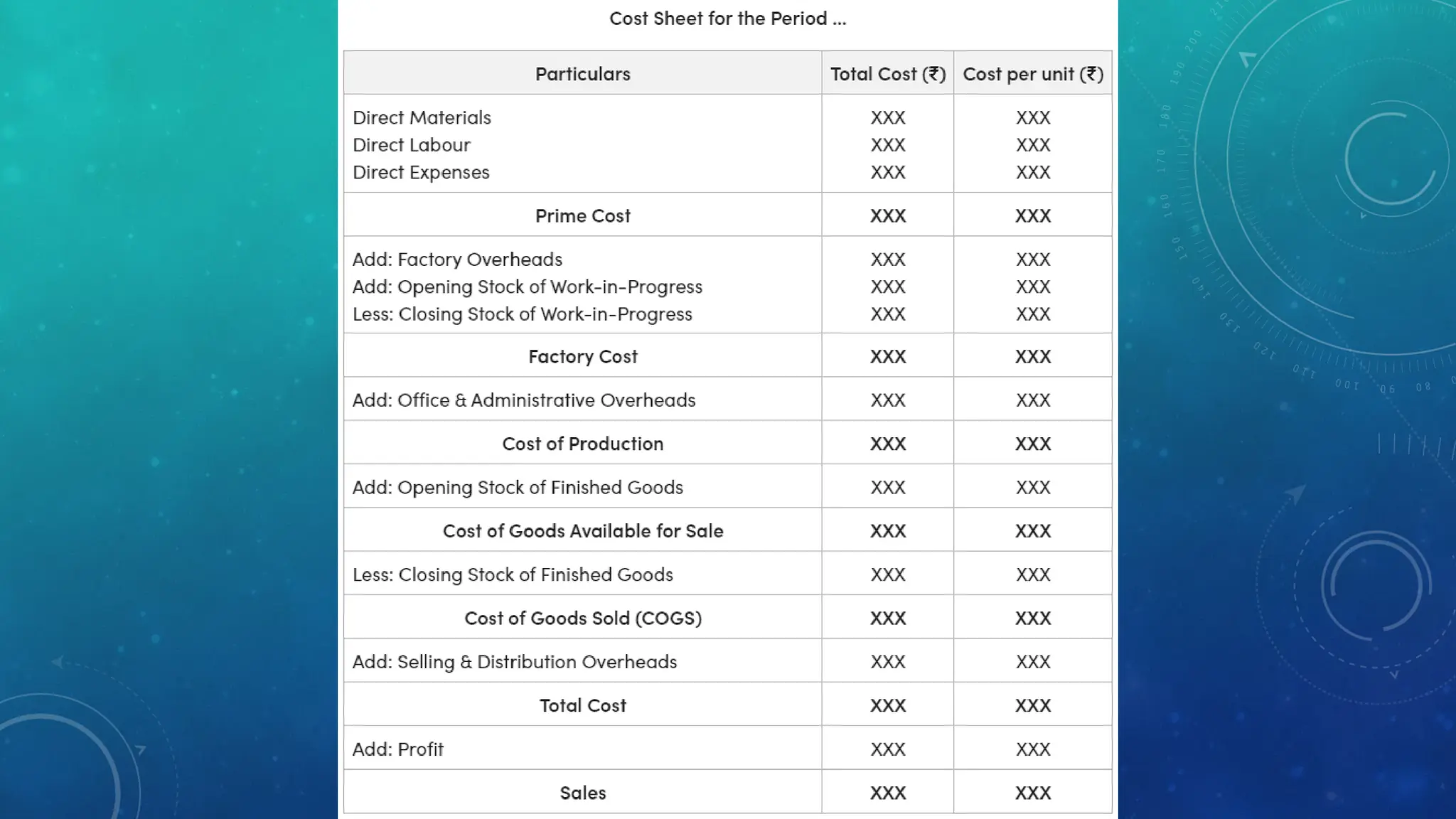

Prime Cost

Prime costs are a firm’s expenses directly related to the materials and labor used in production. It refers to a manufactured

product’s costs, which are calculated to ensure the best profit margin for a company. The prime cost calculates the direct costs of

raw materials and labor that are involved in the production of a good. Direct costs do not include indirect expenses, such as

advertising and administrative costs.

Prime cost = Direct raw materials + Direct labour

Production Cost

Production costs refer to all of the direct and indirect costs businesses face from manufacturing a product or providing a service.

Production costs can include a variety of expenses, such as labor, raw materials, consumable manufacturing supplies, and

general overhead.

13.

• Direct LaborCosts

• Direct labor consists of the fully burdened cost of all labor directly involved in the

production of goods. This usually means those people working on production lines or in

work cells. Other types of production labor are recorded within the category of factory

overhead costs.

• Direct Material Costs

• Direct materials consists of those materials consumed as part of the production process,

including the cost of normal scrap that occurs as part of the process.

• Factory Overhead Costs

• Factory overhead consists of those costs required to maintain the production function,

but which are not directly consumed on individual units. Examples are utilities,

insurance, materials management salaries, production salaries, maintenance wages, and

quality assurance wages.

14.

• Administration Cost

•Administrative expenses refer to the costs incurred by a company or organization that include, but are not limited to, the

salaries and benefits of the administrative workers within the company or organization, as well as rent and managerial

compensation. Also known as General and Administrative expenses, the costs are categorized separately from Sales &

Marketing and Research costs.

• Administrative Expenses

• Managerial team

• IT team

• Executive compensation

• Rent of equipment and buildings

Non-Administrative Expenses

• Manufacturers

• Developers

• Engineers

• Sales Team

15.

• Selling andDistribution Cost

• The term ‘distribution‘ is widely used in relation to the whole operation of getting goods into the hands of the

consumer, and thus covers the two functions of sales promotion and delivery. The expression ‘distribution costs’,

however, may be considered as relating only to delivery.

• Selling Costs: The cost incurred in promoting sales and retaining customers. Selling expenses are those expenses which

are incurred to promote sales and service to customers. Thus, selling overhead includes Salesmen’s Salaries,

Commission, Travelling expenses, Cost of advertisement, Posters, Cost of price list and catalogue, Debt collection

charges, Bad debts, Free gift, Showrooms expenses, After-sale service, Legal expenses for recovering debt, etc.

• Distribution Costs: The cost of the process which begins with making the packed product available for dispatch and

ends with making the reconditioned returned empty package available for re-uses. Distribution expenses, on the other

hand, are those which are incurred for warehousing and storage, packing for goods sent and making the goods

available for delivery to customers. So, in broader sense of the item, distributions expenses include- Cost of storing,

Cost of warehousing, Cost of packing, Cost of delivery, and Cost of preparation of challan.

16.

Fixed Cost

• Inaccounting and economics, fixed costs, also known as indirect costs or overhead costs, are

business expenses that are not dependent on the level of goods or services produced by the

business. They tend to be recurring, such as interest or rents being paid per month. These

costs also tend to be capital costs. This is in contrast to variable costs, which are volume-

related (and are paid per quantity produced) and unknown at the beginning of the accounting

year. Fixed costs have an effect on the nature of certain variable costs. Variable Cost

Variable Cost

• A variable cost is a cost that varies in relation to either production volume or the amount of

services provided. If no production or services are provided, then there should be no variable

costs. If production or services are increasing, then variable costs should also increase.

• Semi-variable Cost

• In such mixed cost, the fixed part will occur irrespective of the production level; even in the

case of zero production activities, a fixed cost will still occur. However, the variable part of such

costs is dependent on the level of production work carried by the entity and increases in

proportion to the production levels. That means that semi-variable costs can be calculated by

adding the fixed costs and the variable costs (based on the level of production).

20.

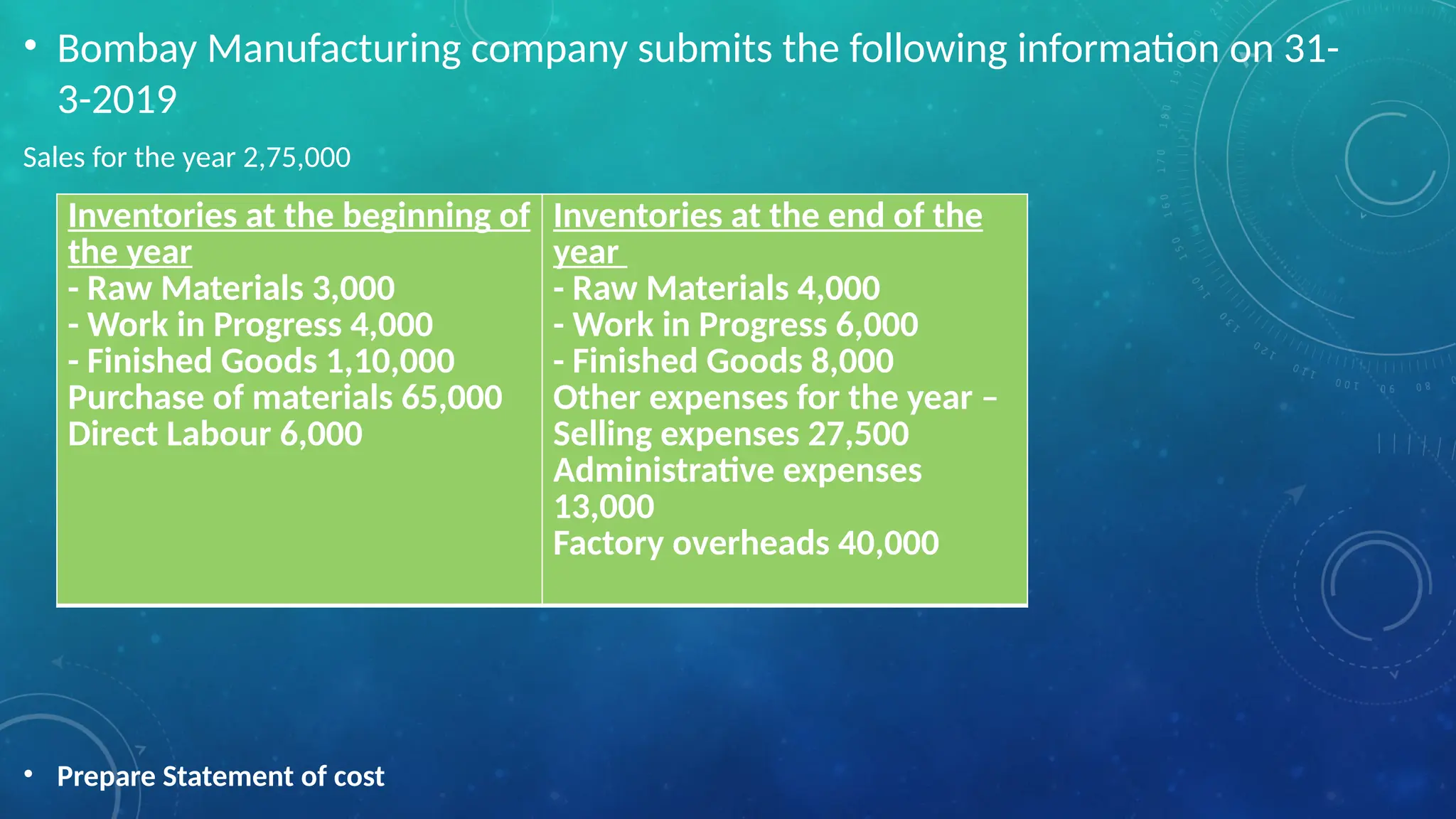

• Bombay Manufacturingcompany submits the following information on 31-

3-2019

Sales for the year 2,75,000

• Prepare Statement of cost

Inventories at the beginning of

the year

- Raw Materials 3,000

- Work in Progress 4,000

- Finished Goods 1,10,000

Purchase of materials 65,000

Direct Labour 6,000

Inventories at the end of the

year

- Raw Materials 4,000

- Work in Progress 6,000

- Finished Goods 8,000

Other expenses for the year –

Selling expenses 27,500

Administrative expenses

13,000

Factory overheads 40,000

21.

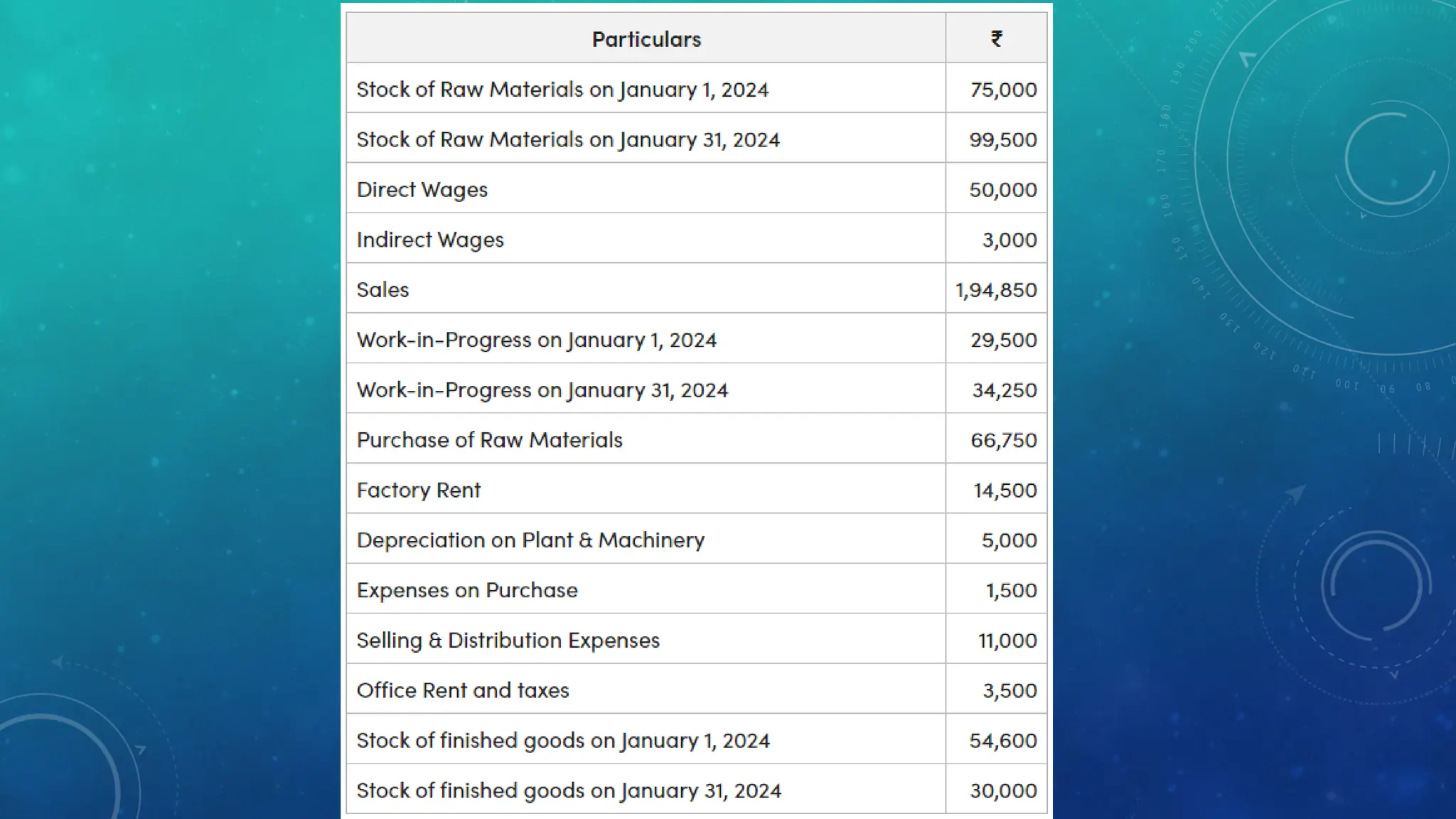

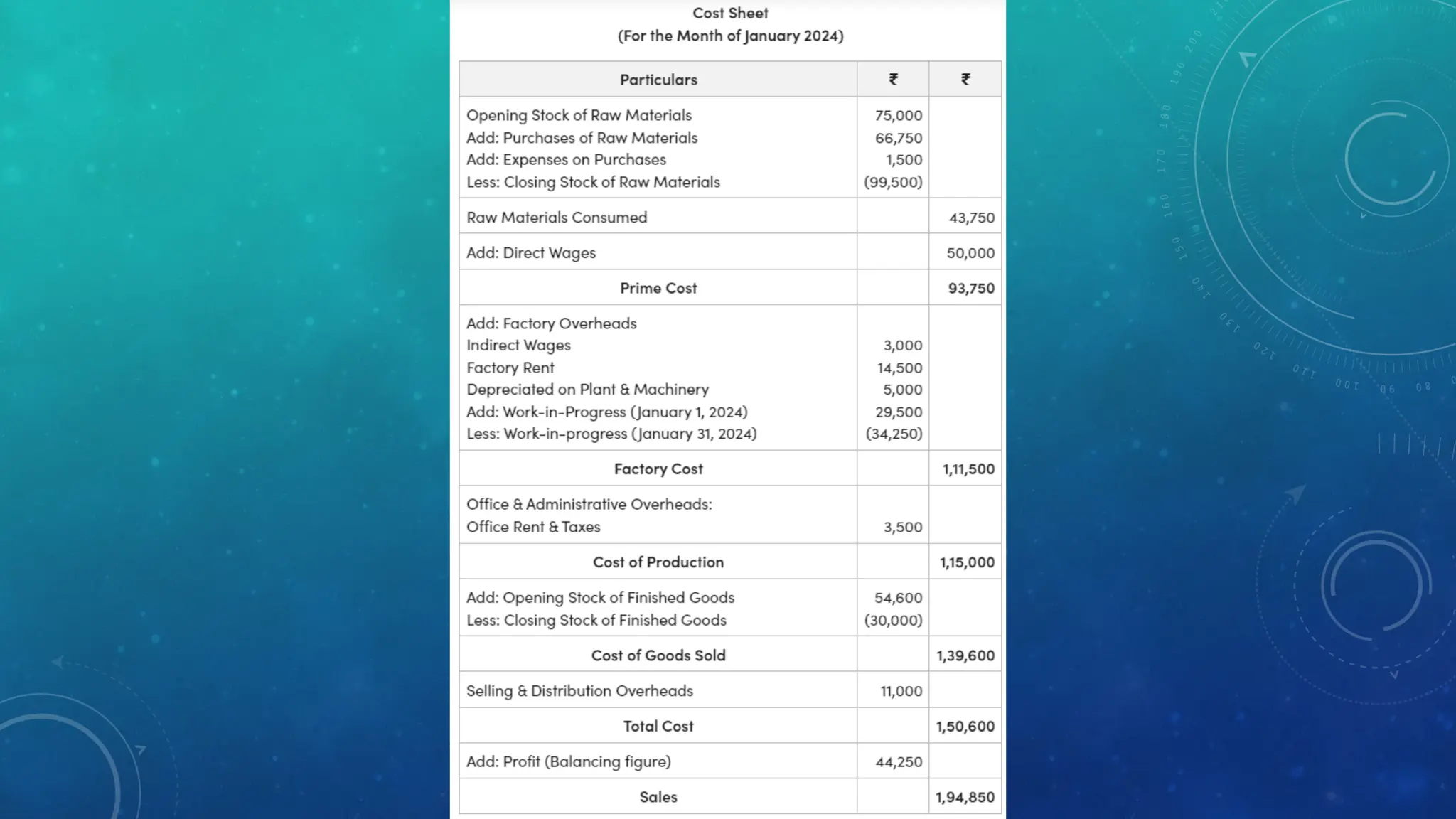

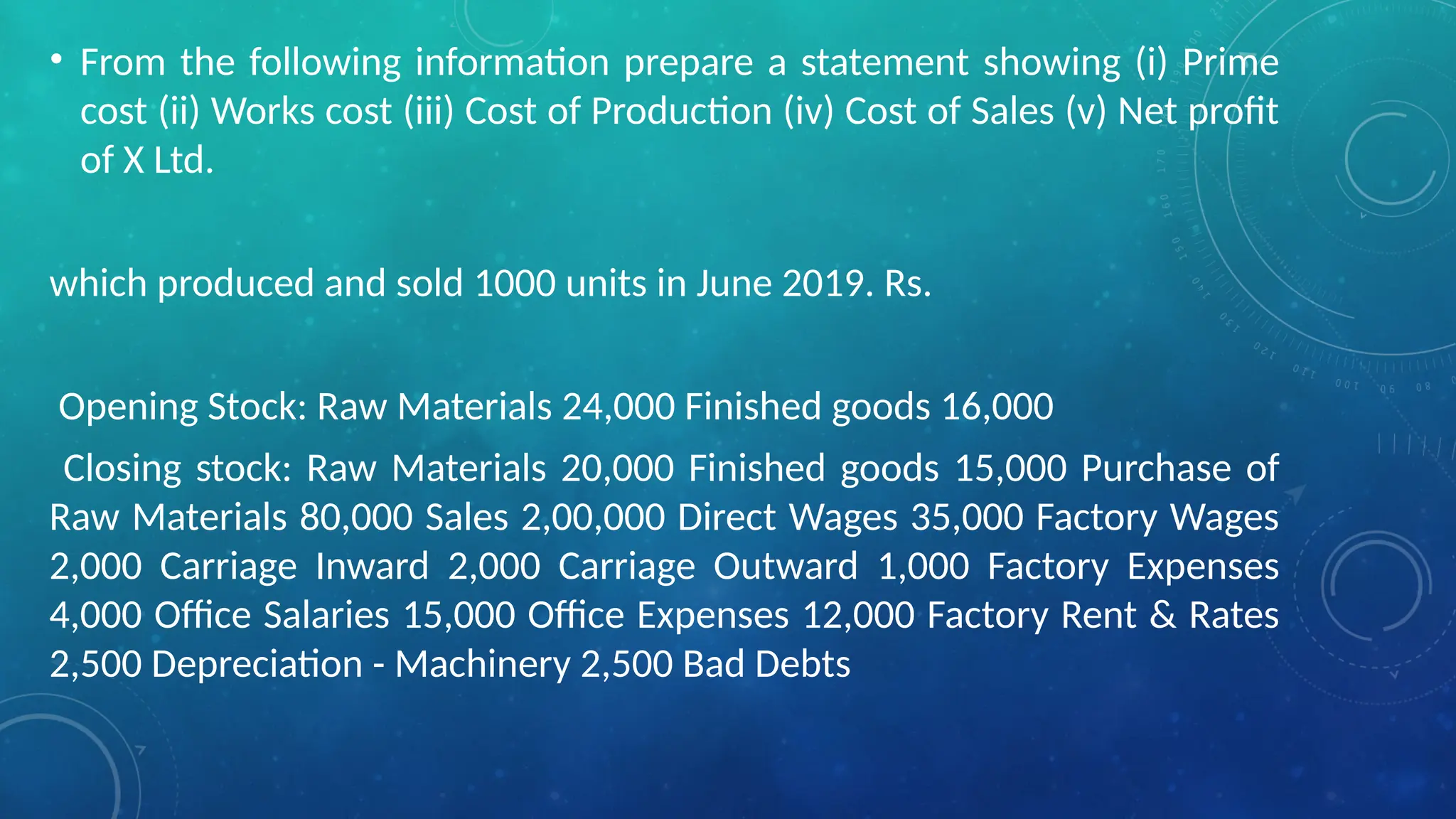

• From thefollowing information prepare a statement showing (i) Prime

cost (ii) Works cost (iii) Cost of Production (iv) Cost of Sales (v) Net profit

of X Ltd.

which produced and sold 1000 units in June 2019. Rs.

Opening Stock: Raw Materials 24,000 Finished goods 16,000

Closing stock: Raw Materials 20,000 Finished goods 15,000 Purchase of

Raw Materials 80,000 Sales 2,00,000 Direct Wages 35,000 Factory Wages

2,000 Carriage Inward 2,000 Carriage Outward 1,000 Factory Expenses

4,000 Office Salaries 15,000 Office Expenses 12,000 Factory Rent & Rates

2,500 Depreciation - Machinery 2,500 Bad Debts

22.

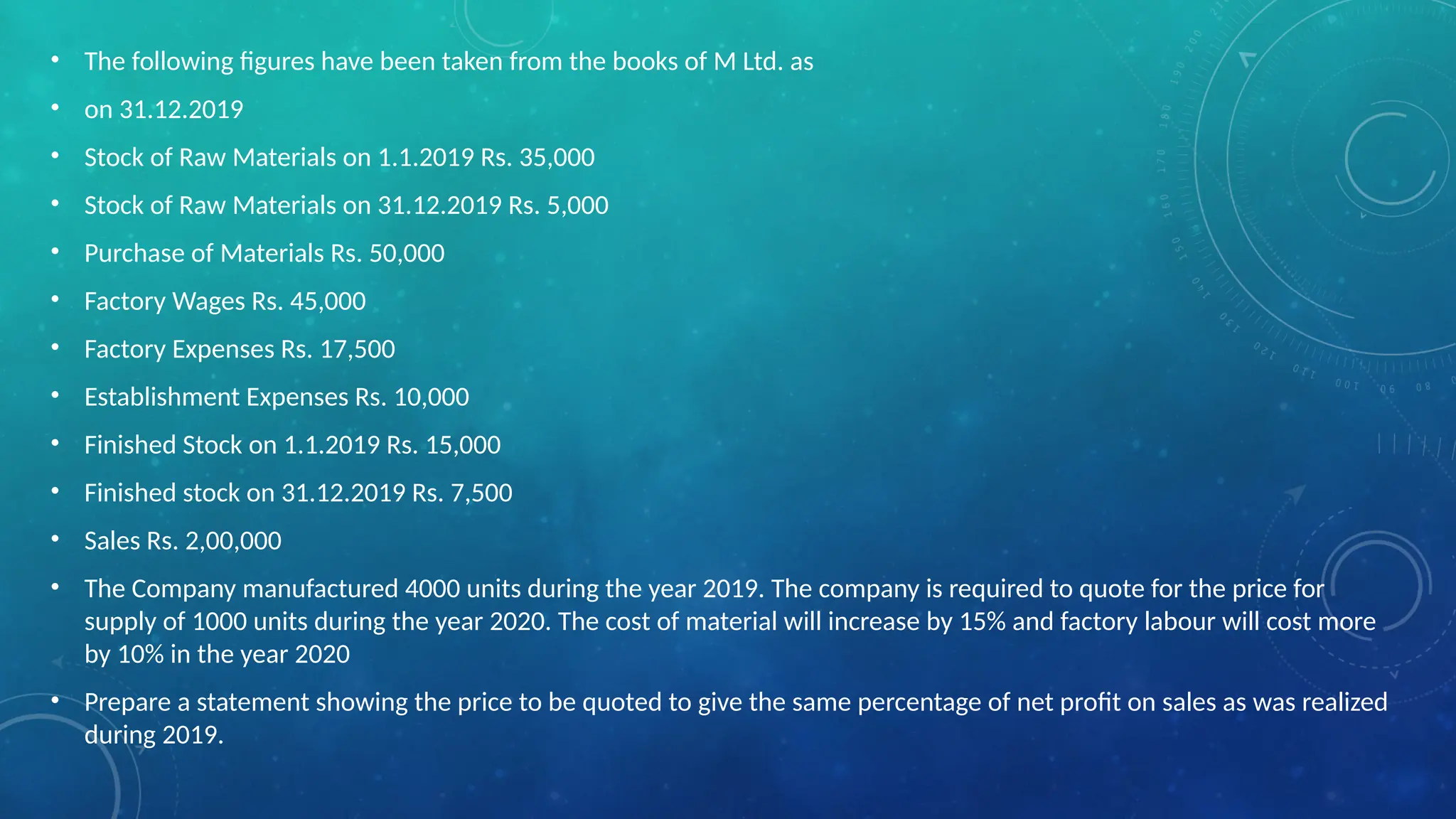

• The followingfigures have been taken from the books of M Ltd. as

• on 31.12.2019

• Stock of Raw Materials on 1.1.2019 Rs. 35,000

• Stock of Raw Materials on 31.12.2019 Rs. 5,000

• Purchase of Materials Rs. 50,000

• Factory Wages Rs. 45,000

• Factory Expenses Rs. 17,500

• Establishment Expenses Rs. 10,000

• Finished Stock on 1.1.2019 Rs. 15,000

• Finished stock on 31.12.2019 Rs. 7,500

• Sales Rs. 2,00,000

• The Company manufactured 4000 units during the year 2019. The company is required to quote for the price for

supply of 1000 units during the year 2020. The cost of material will increase by 15% and factory labour will cost more

by 10% in the year 2020

• Prepare a statement showing the price to be quoted to give the same percentage of net profit on sales as was realized

during 2019.