Downloaded 45 times

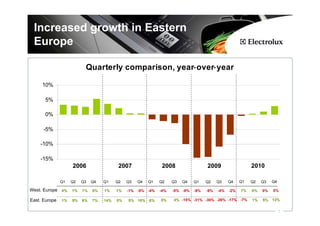

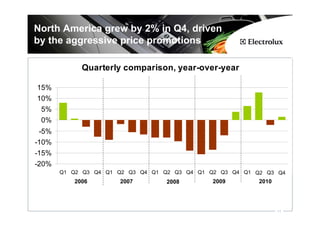

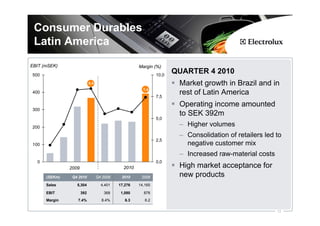

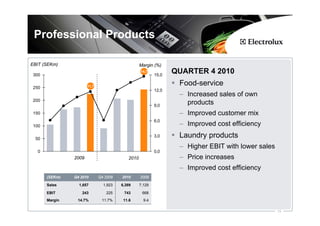

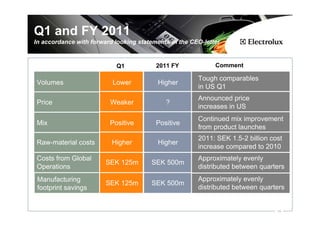

The document presents the financial results and operational highlights of Electrolux for Q4 2010, noting a net sales increase of 7.2% and an EBIT margin decline due to raw material challenges and price pressures. It highlights the company's performance in various regions, including growth in Latin America and Asia/Pacific, while facing declines in Europe and North America. Forward-looking statements indicate expectations for future pricing and cost dynamics amid market uncertainties.

![[ls머트리얼즈]LS Materials 417200 Algorithm Investment Report](https://cdn.slidesharecdn.com/ss_thumbnails/lsmaterials417200algorithminvestmentreport-260202182715-66072c7b-thumbnail.jpg?width=640&height=640&fit=bounds)