Downloaded 33 times

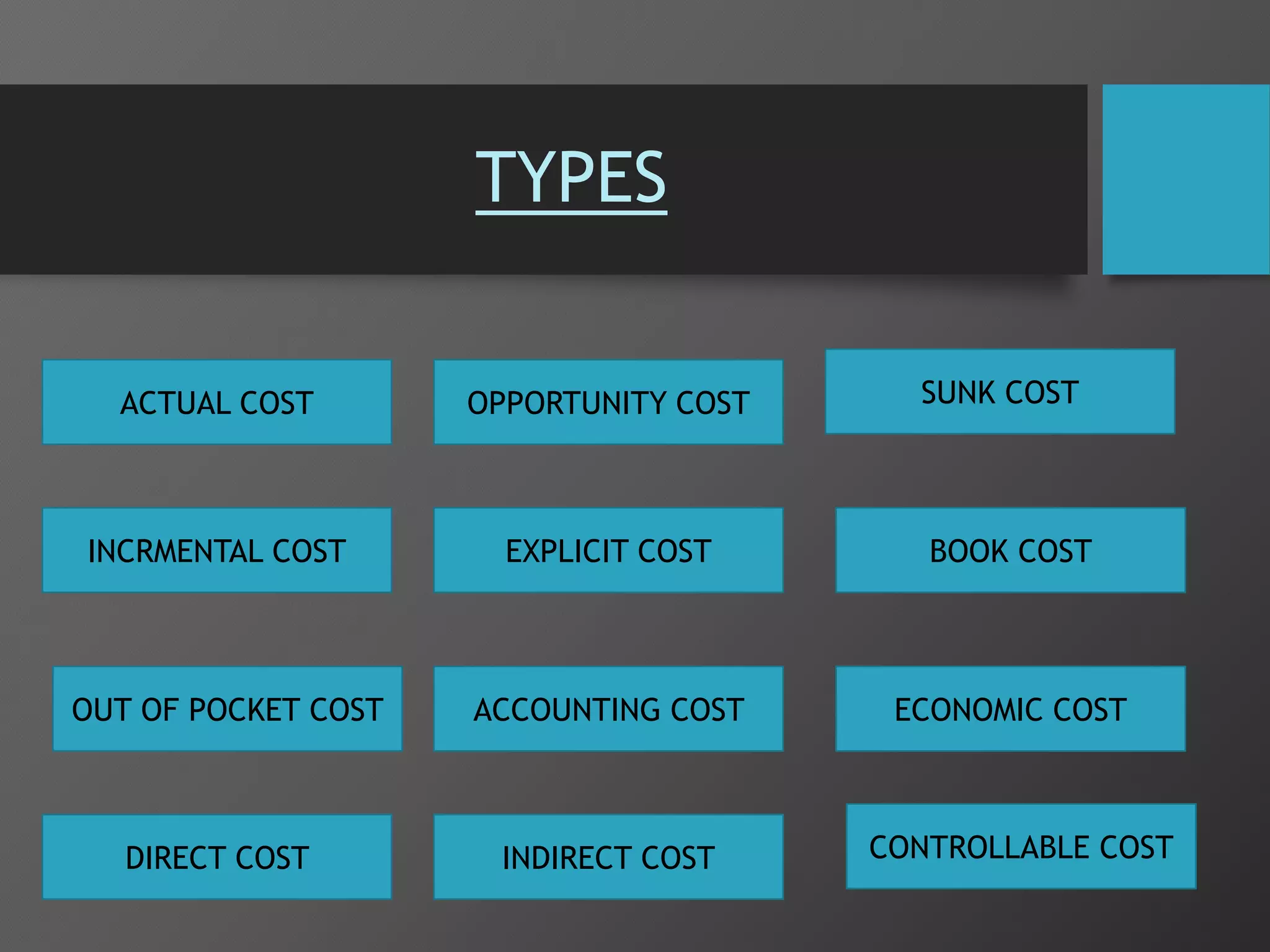

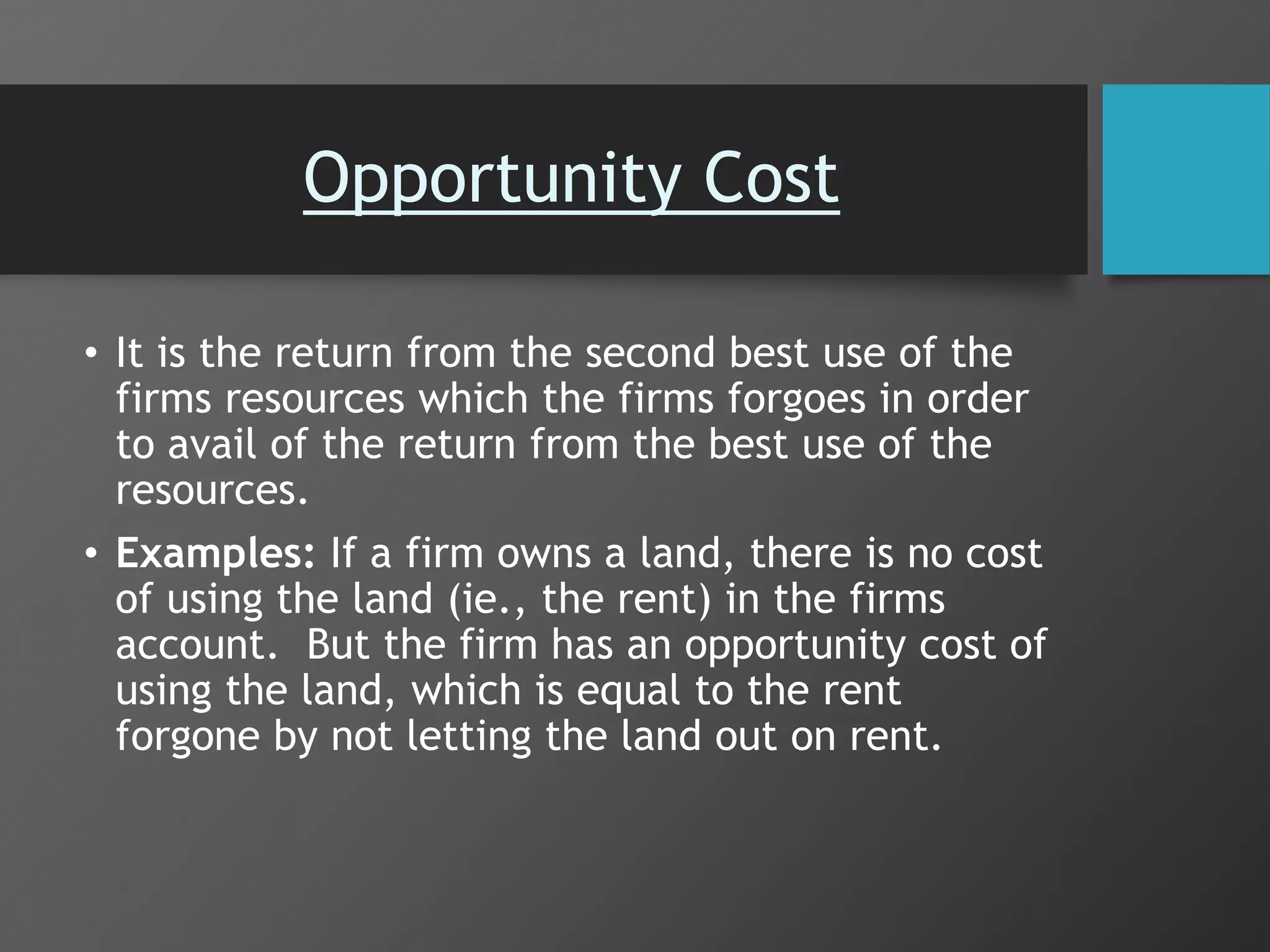

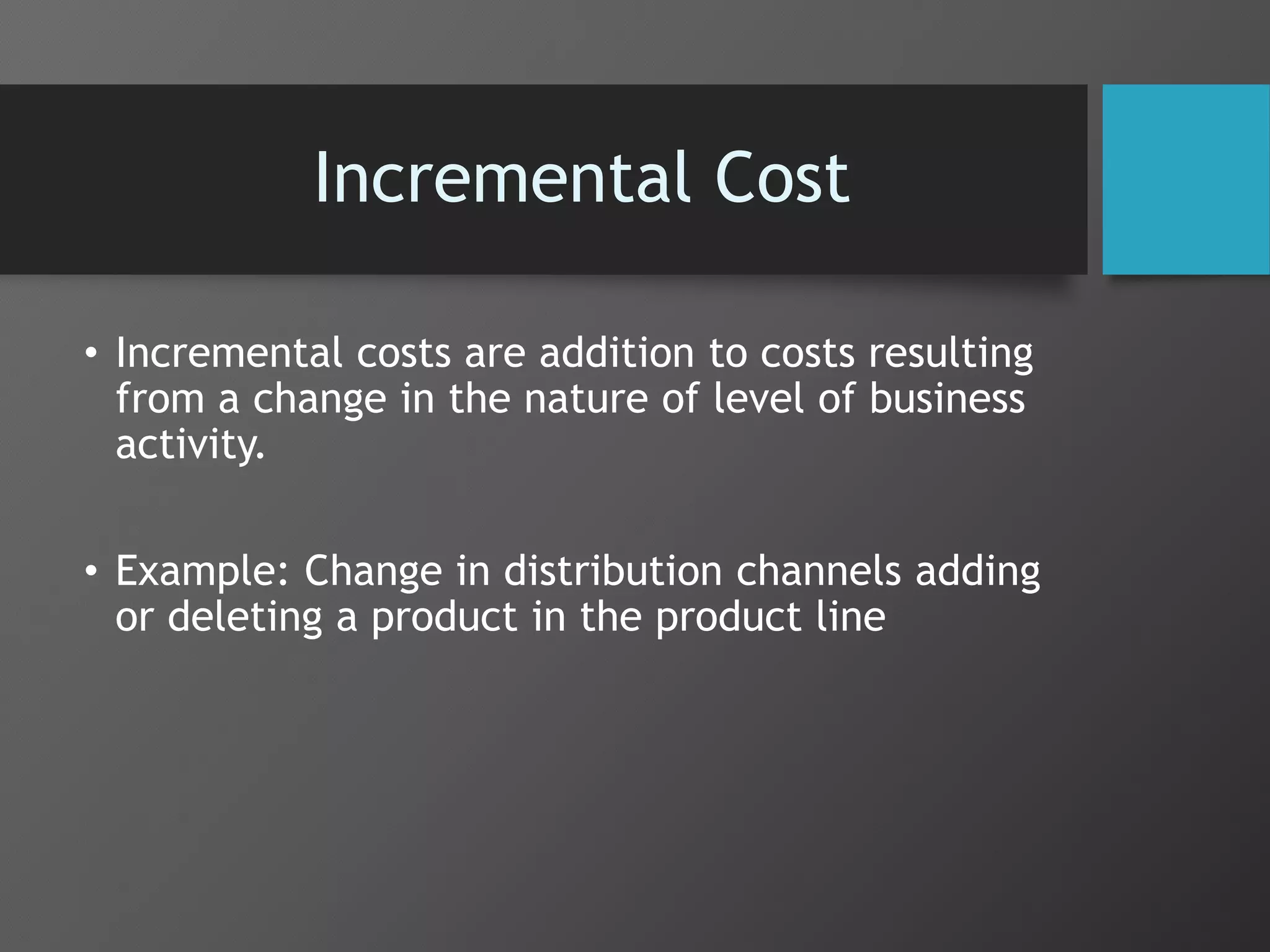

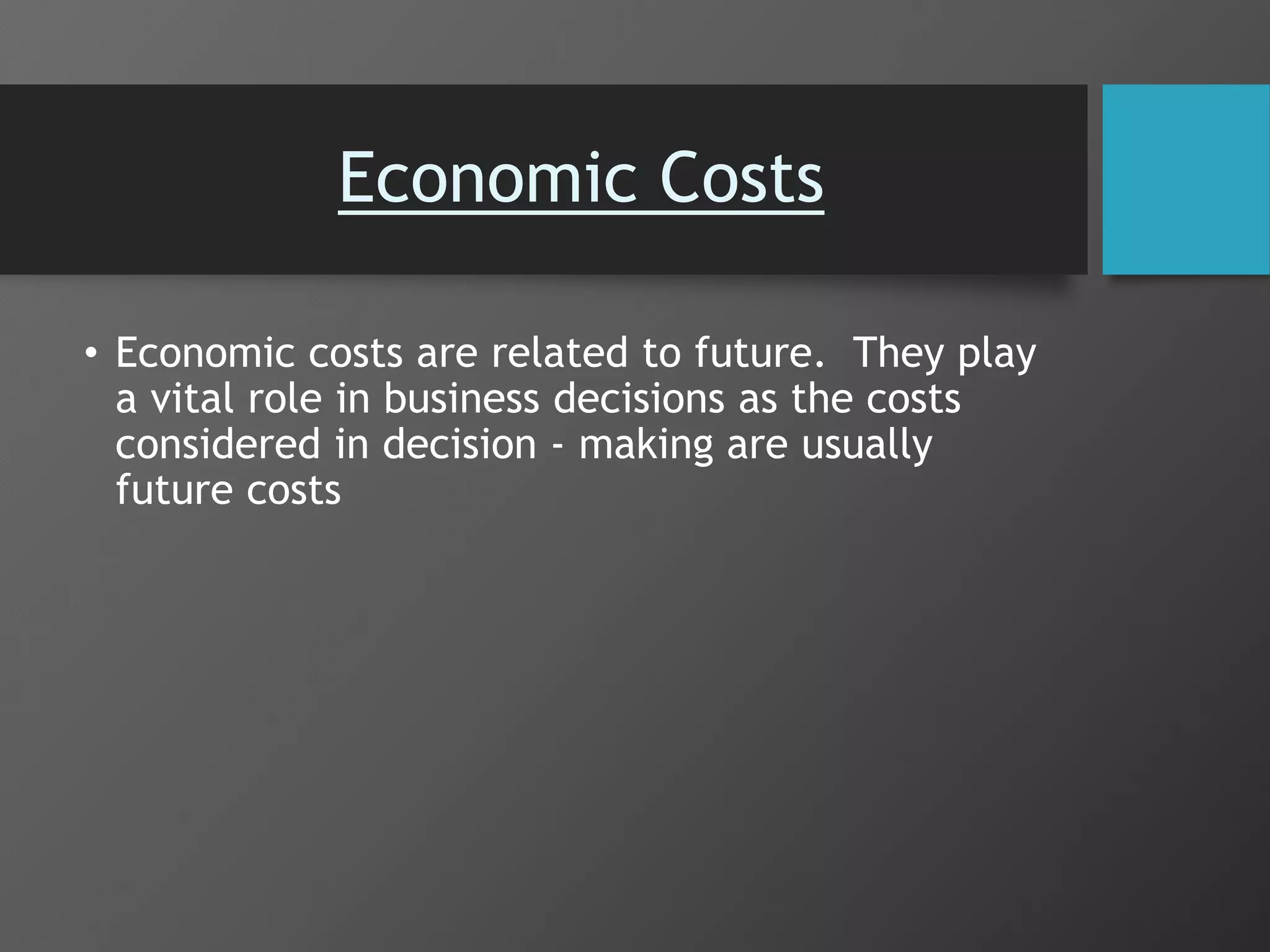

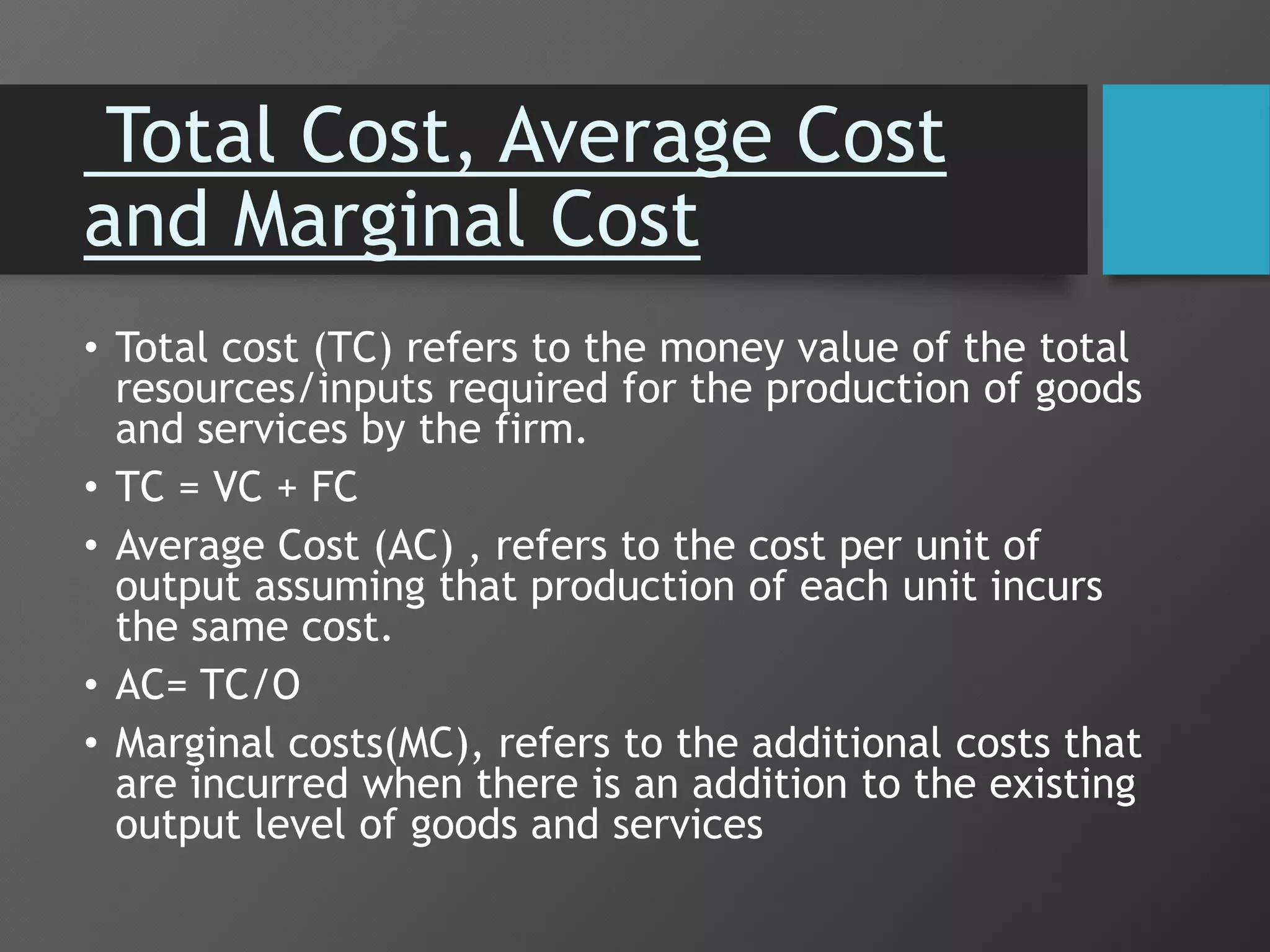

This document provides an overview of different types of costs that are relevant for business. It defines key cost terms like actual cost, opportunity cost, sunk cost, incremental cost, explicit cost, implicit cost, book cost, out of pocket costs, accounting costs, economic costs, direct costs, indirect costs, controllable costs, non-controllable costs, historical costs, replacement costs, shutdown costs, abandonment costs, urgent costs, business costs, fixed costs, variable costs, total costs, average costs, marginal costs, short run costs, and long run costs. Examples are provided for most cost types.