1. A VAR model comprises multiple time series and is an extension of the autoregressive model that allows for feedback between variables.

2. The optimal lag length is chosen using information criteria like AIC and BIC to balance model fit and complexity.

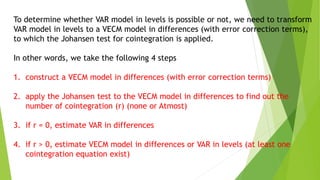

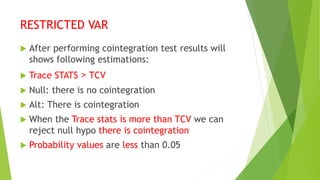

3. Cointegration testing determines whether variables have a long-run relationship and whether a VECM or VAR in differences should be specified.

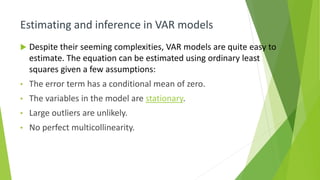

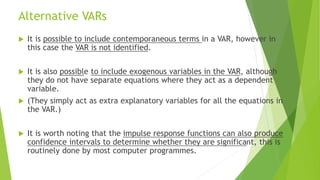

![Sample VAR Result

OLS estimation of a single equation in the Unrestricted VAR

******************************************************************************

Dependent variable is TBILL

127 observations used for estimation from 1960Q2 to 1991Q4

Regressor Coefficient Standard Error T-Ratio [Prob]

TBILL(-1) .96200 .067845 14.1795 [.000]

R10(-1) -.015333 .068439 -.22404 [.823]

K .36563 .23386 1.5635 [.120]

R-Squared .90159 R-Bar-Squared .90000

Akaike Info. Criterion -165.9593 Schwarz Bayesian Criterion -170.22

Serial Correlation*CHSQ( 4)= 22.3179[.000]

Dependent variable is R10

******************************************************************************

Regressor Coefficient Standard Error T-Ratio[Prob]

TBILL(-1) .11106 .039920 2.7821[.006]

R10(-1) .87432 .040269 21.7117[.000]

K .26981 .13760 1.9608[.052]

R-Squared .96507 R-Bar-Squared .96451

Akaike Info. Criterion -98.6049 Schwarz Bayesian Criterion -102.8712

Serial Correlation*CHSQ( 4)= 8.6481[.071]](https://image.slidesharecdn.com/ders7-230105135300-fa5b9b59/85/ders-7-1-VAR-pptx-55-320.jpg)

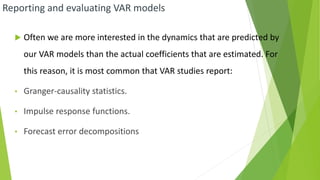

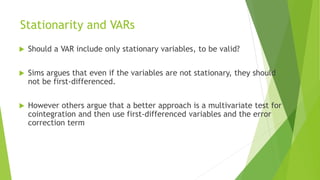

![Granger Causality Test

******************************************************************************

Dependent variable is R10

List of the variables deleted from the regression: TBILL (-1)

127 observations used for estimation from 1960Q2 to 1991Q4

******************************************************************************

Regressor Coefficient Standard Error T-Ratio [Prob]

R10(-1) .97627 .017142 56.9508 [.000]

K .20365 .13914 1.4637 [.146]

******************************************************************************

Joint test of zero restrictions on the coefficients of deleted variables:

F Statistic F( 1, 124)= 7.7400[.006]

Dependent variable is TBILL

List of the variables deleted from the regression: R10(-1)

Regressor Coefficient Standard Error T-Ratio [Prob]

TBILL(-1) .94817 .028025 33.8328 [.000]

K .33727 .19589 1.7217 [.088]

******************************************************************************

Joint test of zero restrictions on the coefficients of deleted variables:

F Statistic F( 1, 124)= .050192[.823]

*****************************************************************************](https://image.slidesharecdn.com/ders7-230105135300-fa5b9b59/85/ders-7-1-VAR-pptx-59-320.jpg)