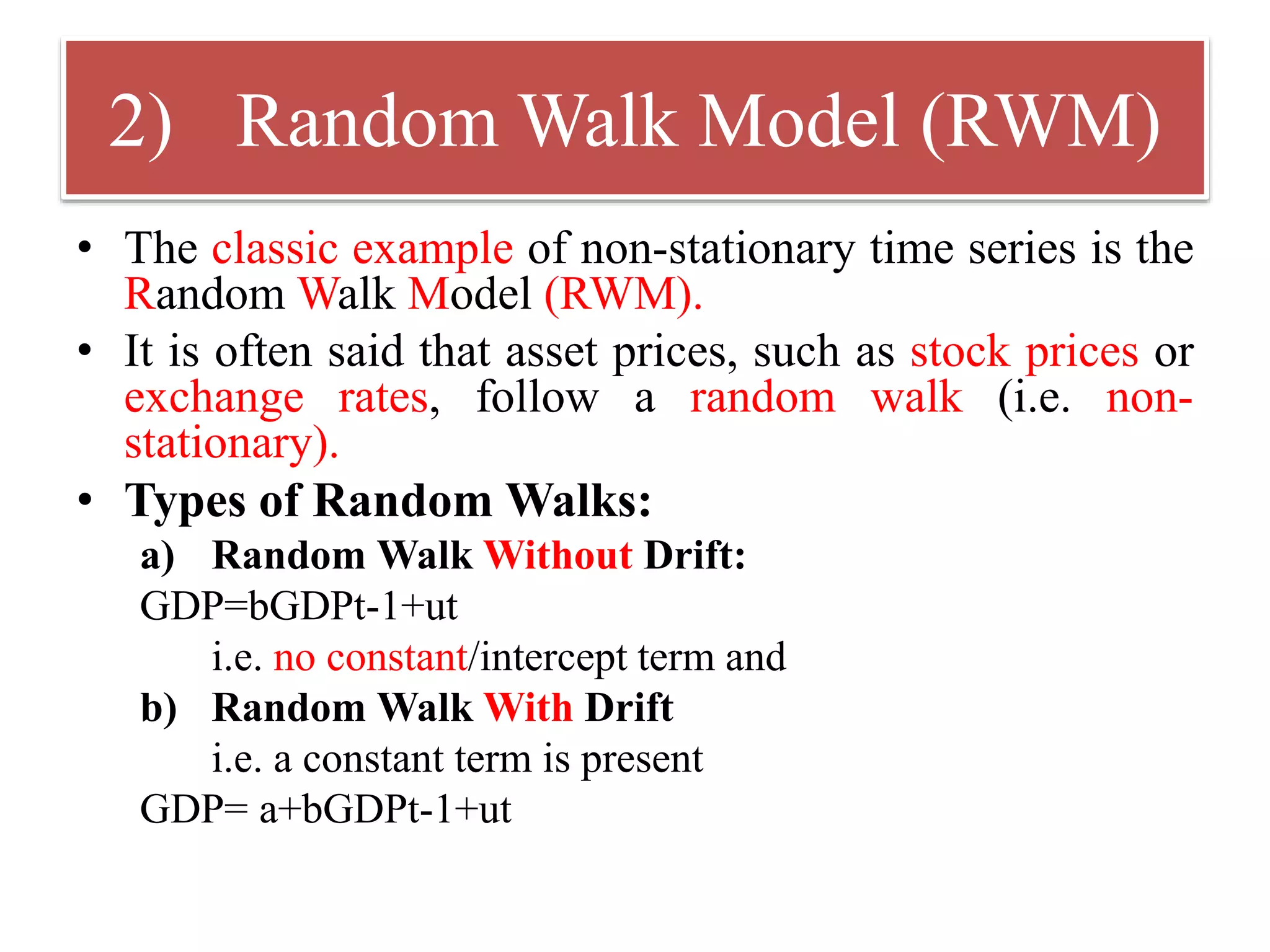

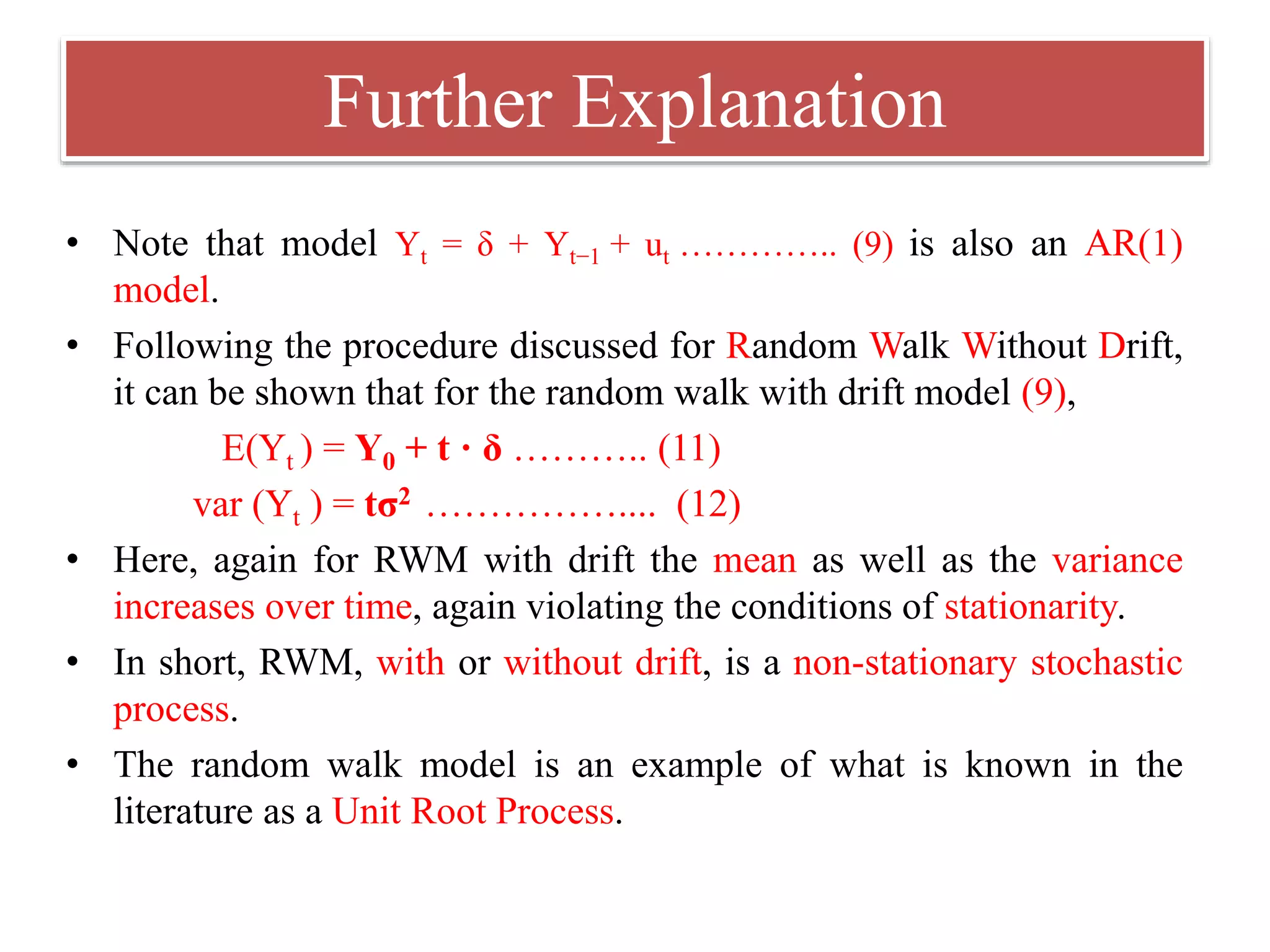

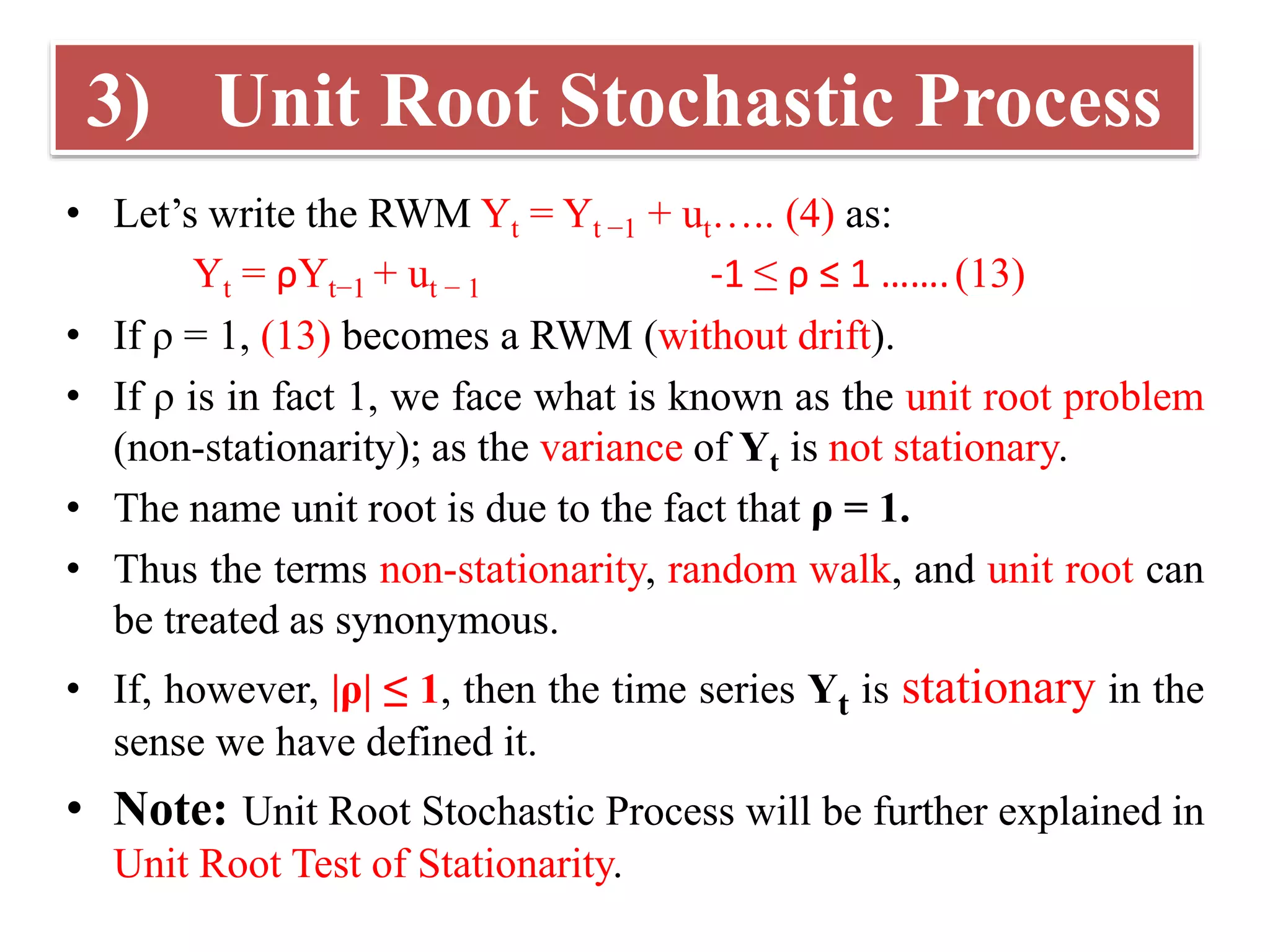

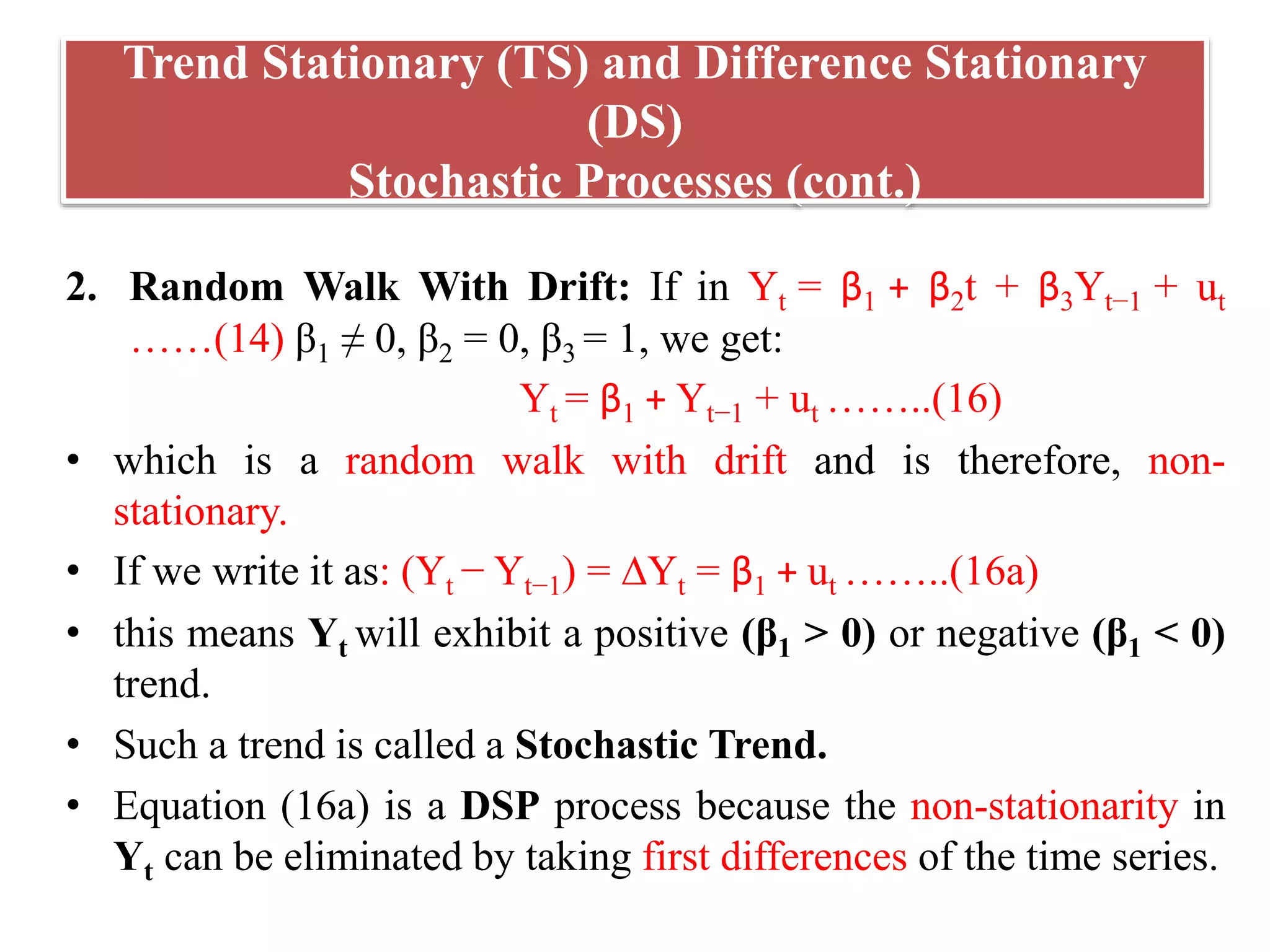

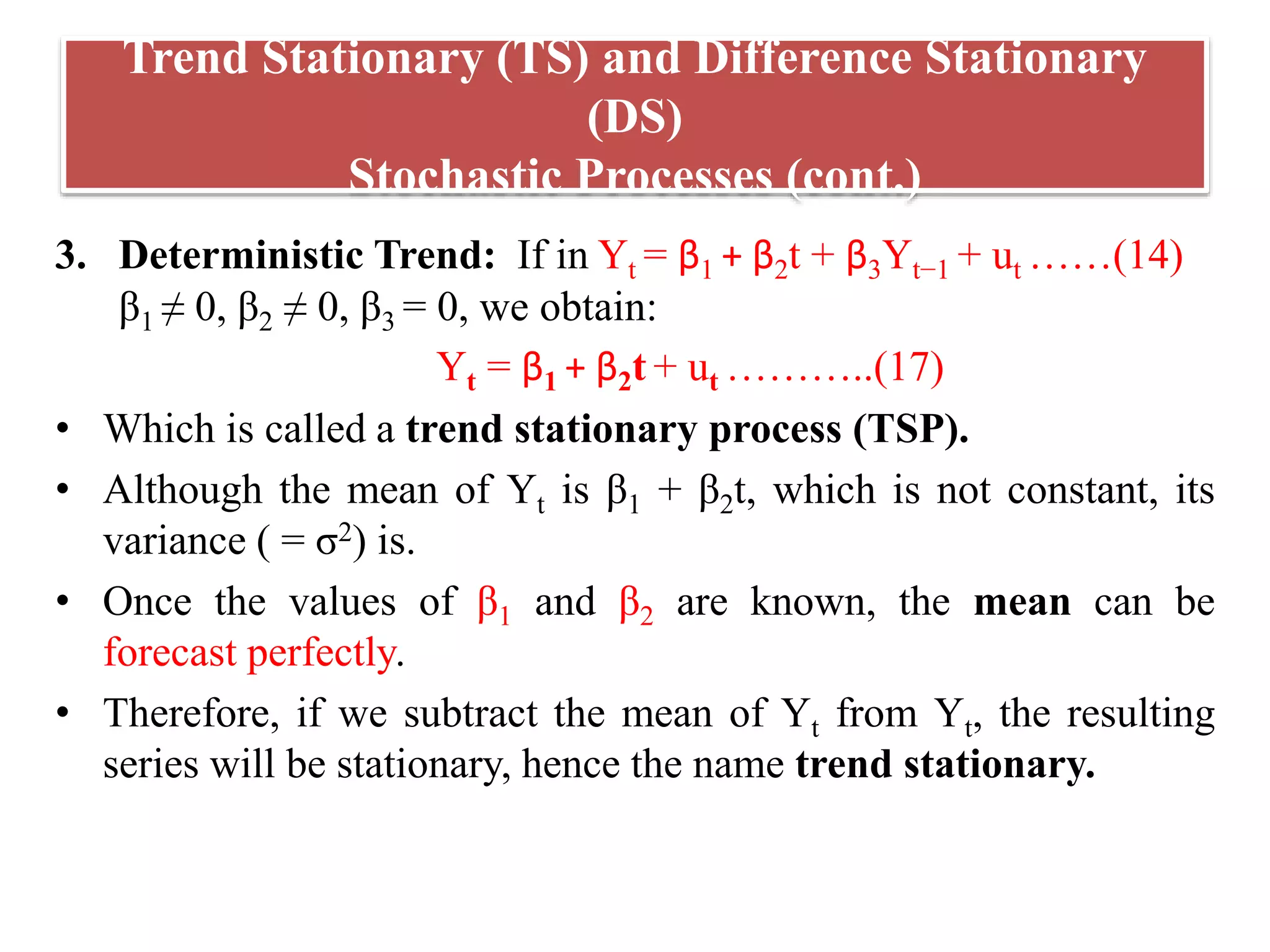

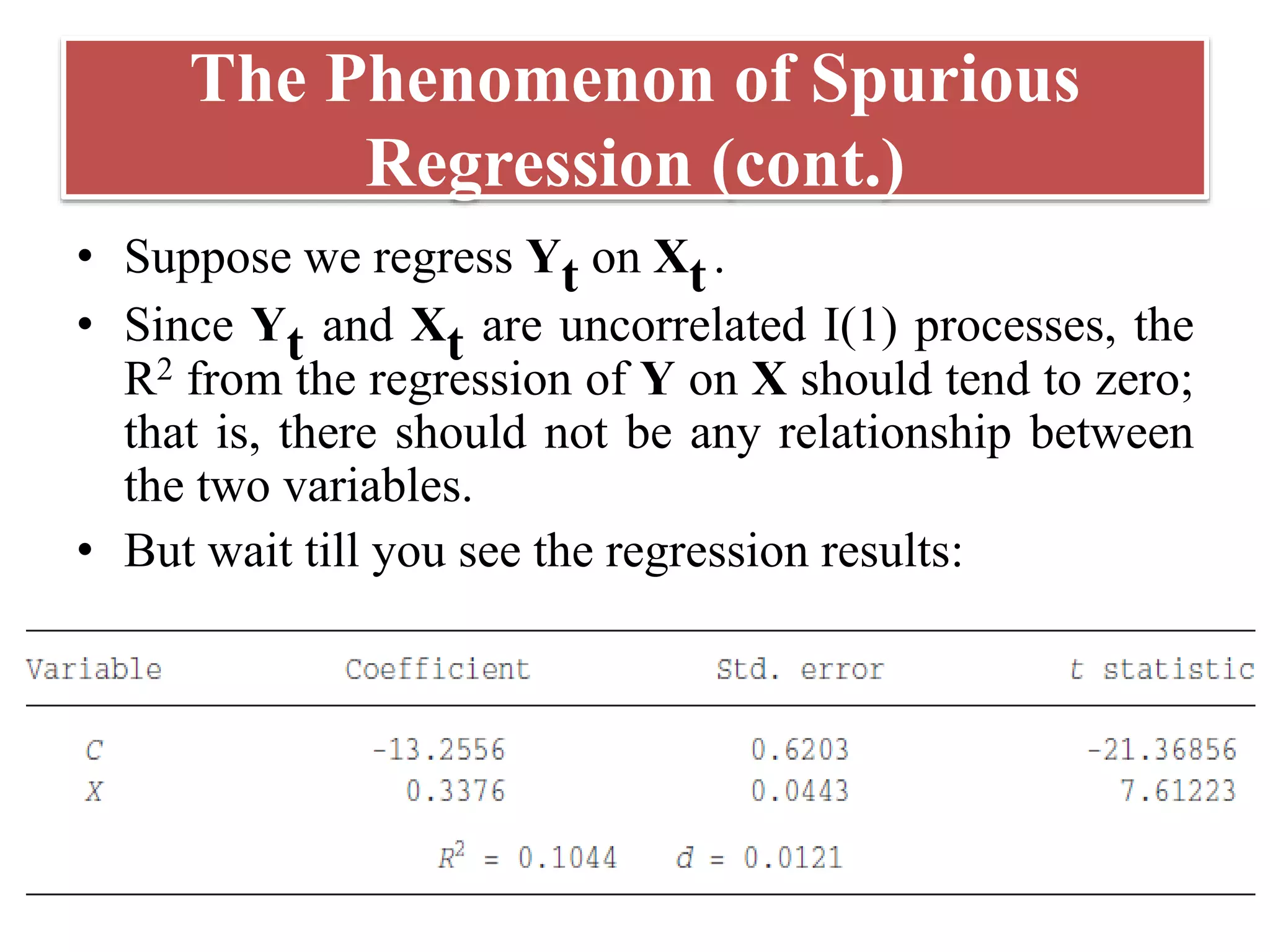

Time series econometrics deals with time series data that poses challenges due to non-stationarity. There are three types of stochastic processes - stationary, purely random, and non-stationary. Random walk models including random walk with and without drift are examples of non-stationary processes. A unit root stochastic process refers to non-stationary time series. Time series can be either trend stationary or difference stationary. Failing to account for non-stationarity can result in spurious regressions with high R-squared but no meaningful relationship between variables.

![(1) Stochastic Processes

• Stationary Stochastic Processes: A stochastic process is

said to be stationary/ weakly /covariance/2nd-order

stationary if:

o Its mean and variance are constant over time, and

o The value of the covariance between the two time periods depends only

on the distance/lag between the two time periods and not the actual time

at which the covariance is computed.

o E.g. let’s Yt be a stochastic process, then;

– Mean: E(Yt ) = µ …………………………………………..

(1)

– Variance: var (Yt ) = E(Yt − µ)2 = σ2 ………………………………..

(2)

– Covariance: γk = E[(Yt − µ)(Yt +k − µ)] ……………..…………(3)

• Where γk, the covariance (or auto-covariance) at lag k,

• If k = 0, we obtain γ0, which is simply the variance of Y (= σ2); if k =

1, γ1 is the covariance between two adjacent values of Y](https://image.slidesharecdn.com/introductiontotimeseries-221102160217-499aaa33/75/Introduction-to-time-series-pptx-5-2048.jpg)

![• We call a stochastic process(time series) purely random/white noise

process if it has zero mean, constant variance σ2, and is serially

uncorrelated i.e. [ut ∼ IIDN(0, σ2)].

• Note: Here onward, in all equations the assumption of “white noise” will be

applicable on ut .

• Yt= a +b1xt+b2xt+et

White Noise Processes](https://image.slidesharecdn.com/introductiontotimeseries-221102160217-499aaa33/75/Introduction-to-time-series-pptx-7-2048.jpg)

![• In each case, the null hypothesis is that δ = 0;

i.e. there is a unit root—the time series is non-

stationary.

• The alternative hypothesis is that δ is less than

zero; i.e. the time series is stationary.

• If the null hypothesis is rejected, it means that Yt

is a stationary time series with zero mean in the

case of (4.2), that Yt is stationary with a nonzero

mean [= β1/(1 − ρ)] in the case of (4.4), and that

Yt is stationary around a deterministic trend in

(4.5).](https://image.slidesharecdn.com/introductiontotimeseries-221102160217-499aaa33/75/Introduction-to-time-series-pptx-33-2048.jpg)