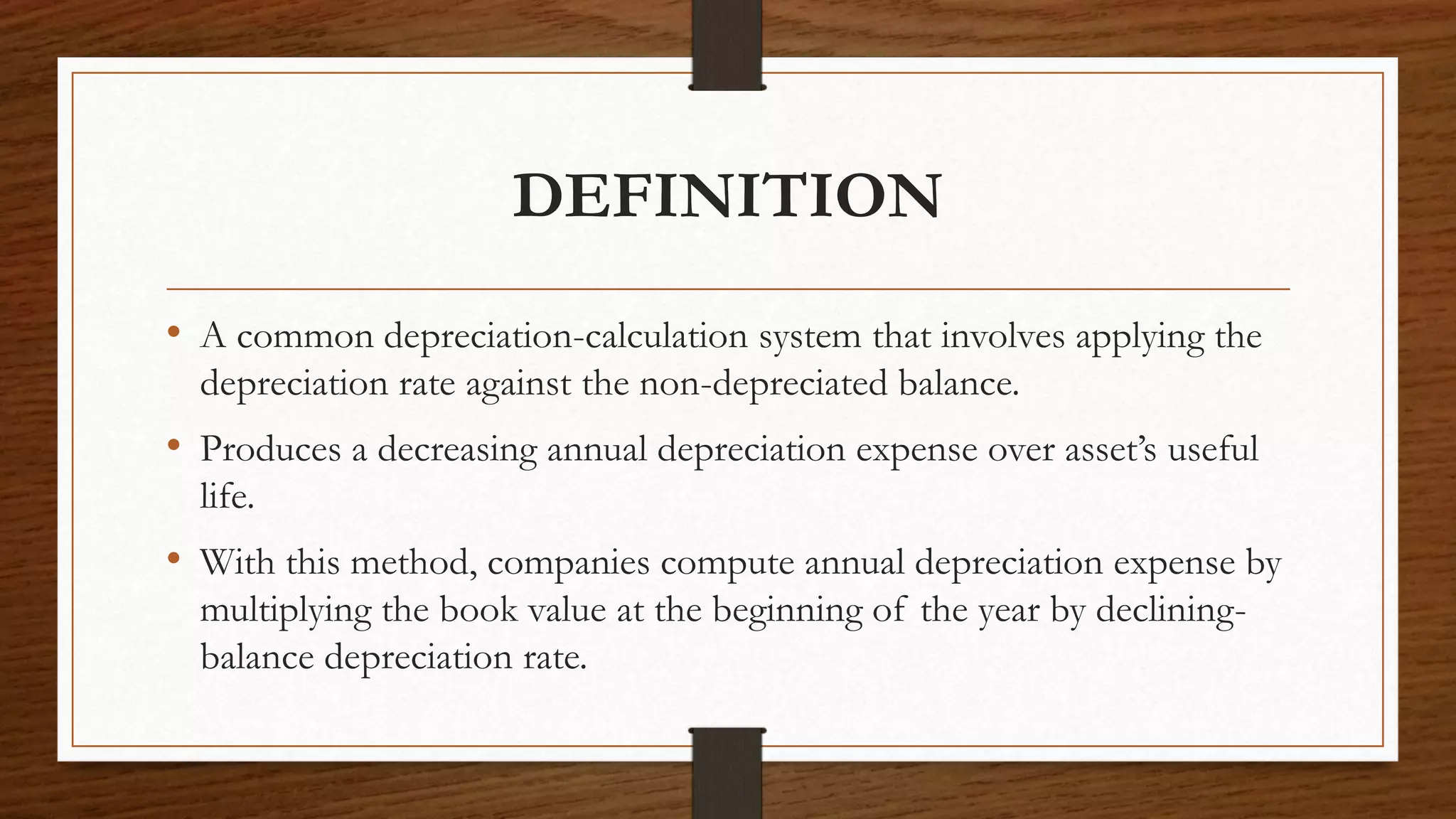

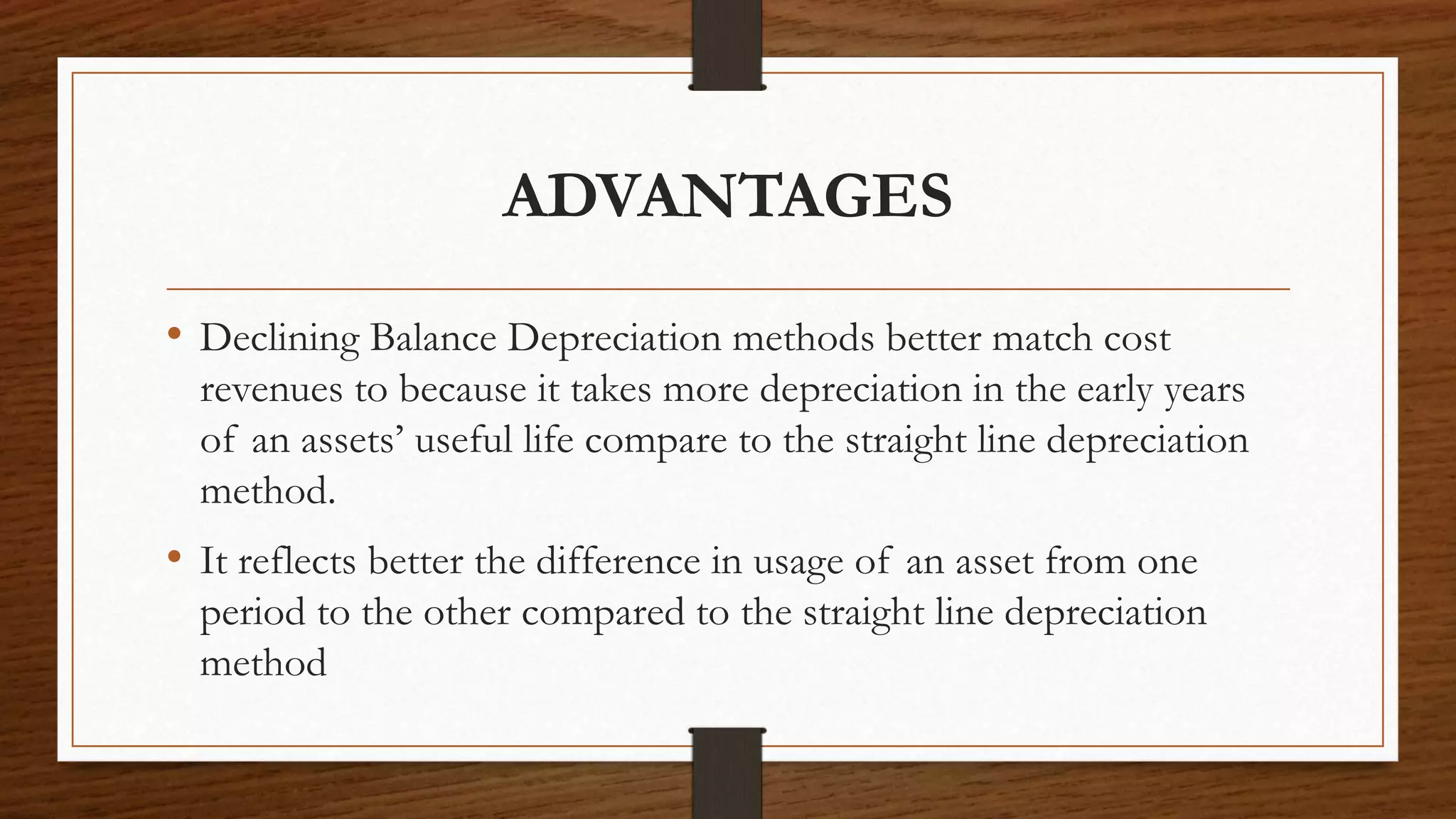

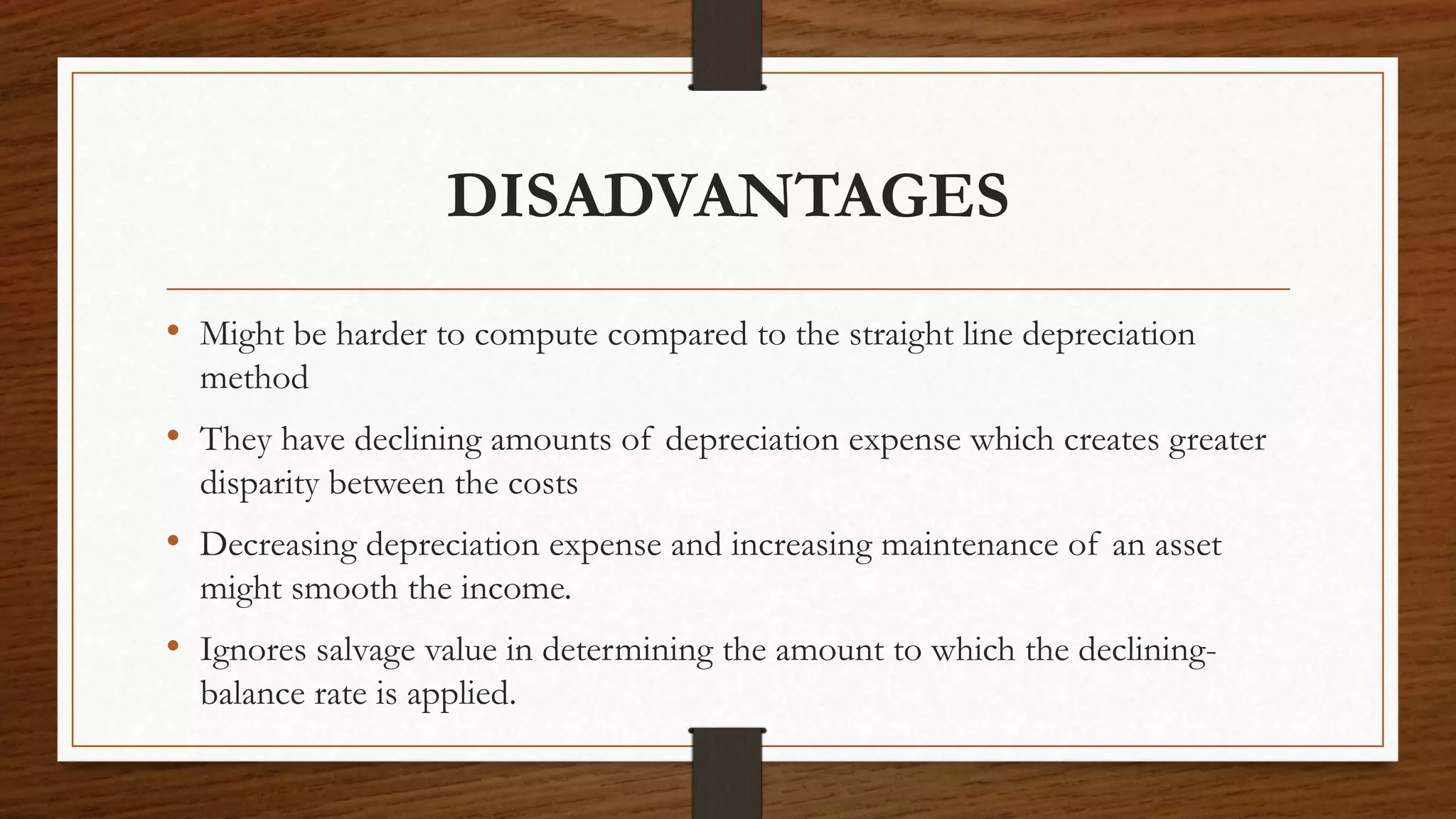

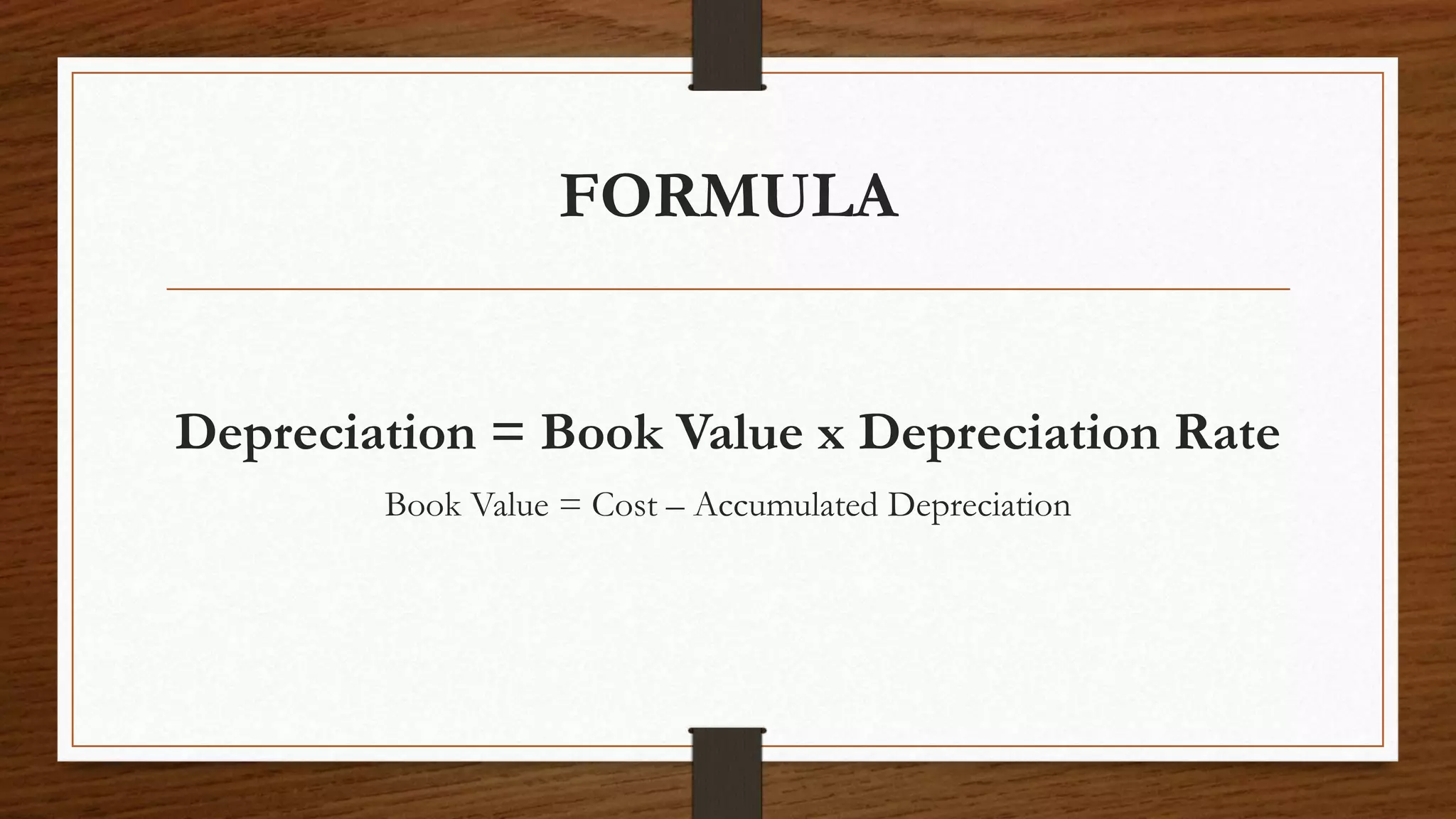

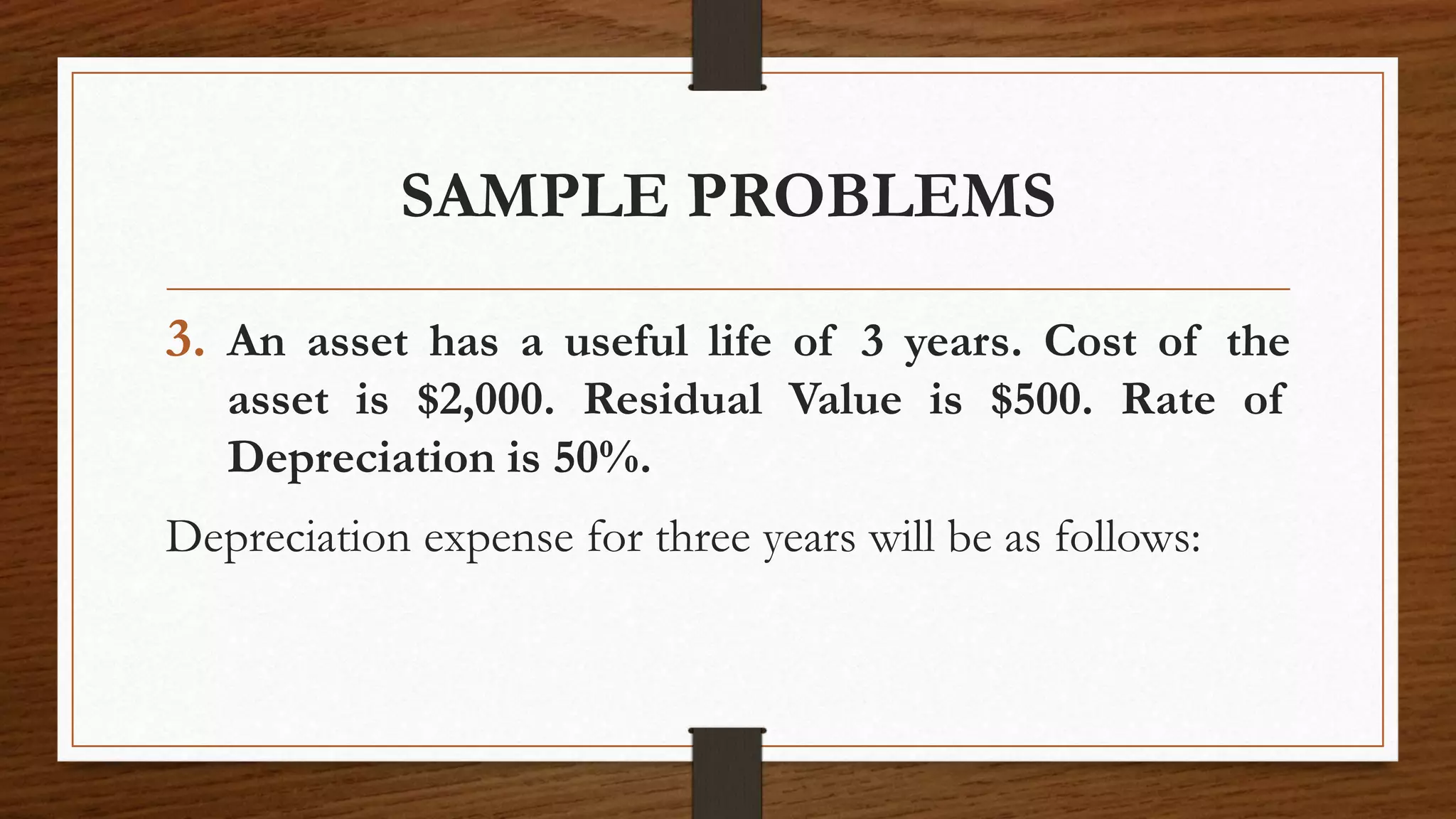

The document discusses the declining balance method of depreciation. It defines declining balance depreciation as applying the depreciation rate against the non-depreciated balance each year, resulting in a decreasing annual depreciation expense over the asset's useful life. The advantages are that it better matches costs to revenues by taking more depreciation in early years. The disadvantages are it may be harder to compute and ignores salvage value. Formulas and examples are provided to demonstrate how to calculate depreciation expense using the declining balance method.