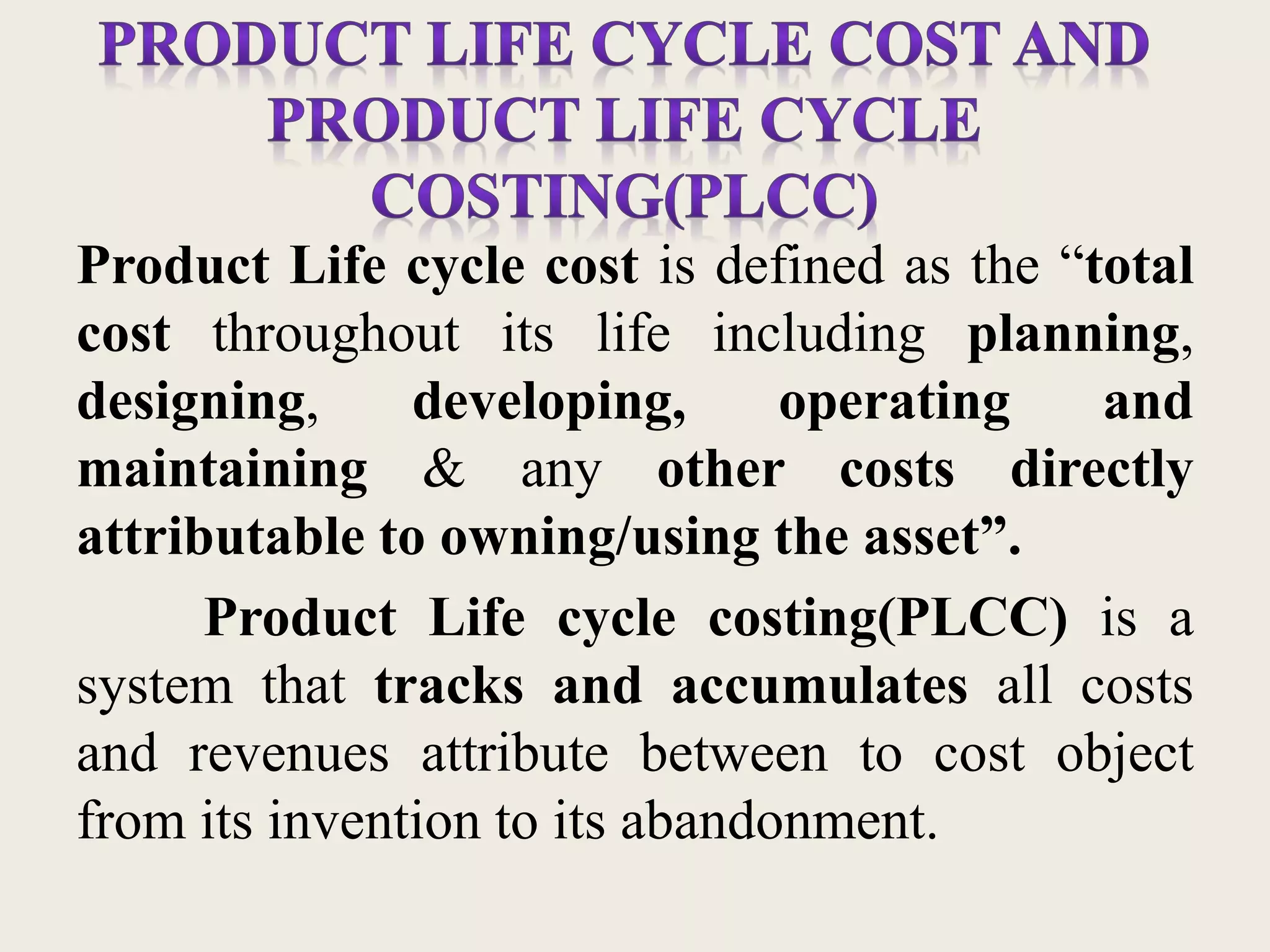

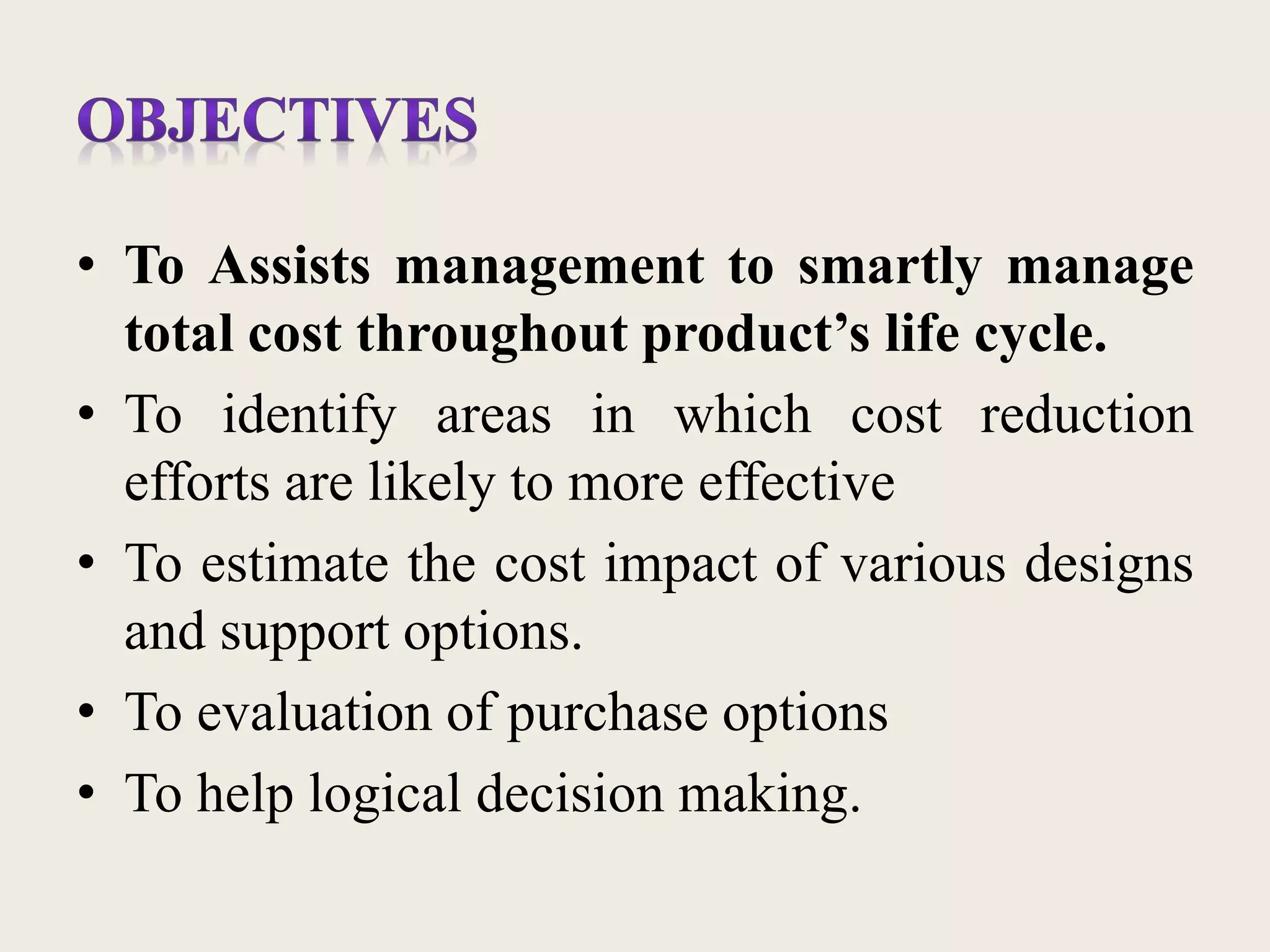

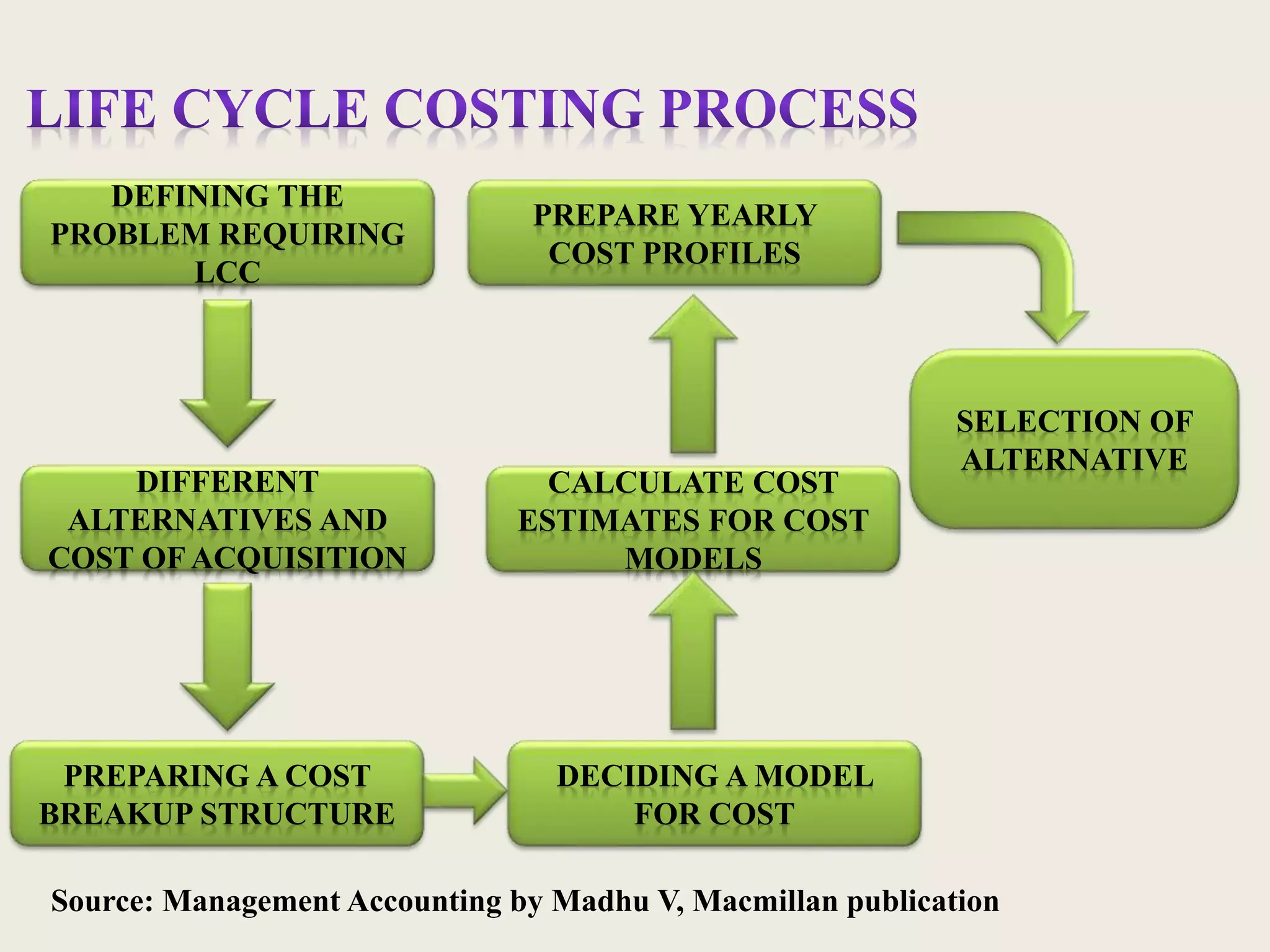

The document discusses product life cycle costing (PLCC). PLCC tracks and accumulates all costs from invention to abandonment of a product. It helps calculate total costs over the product's entire lifecycle. PLCC considers initial costs, operating and maintenance costs, and can identify areas for cost reduction. PLCC was developed in the 1960s and used by defense agencies to improve cost effectiveness. It provides a more accurate assessment of total revenues and costs than traditional accounting methods.