Downloaded 25 times

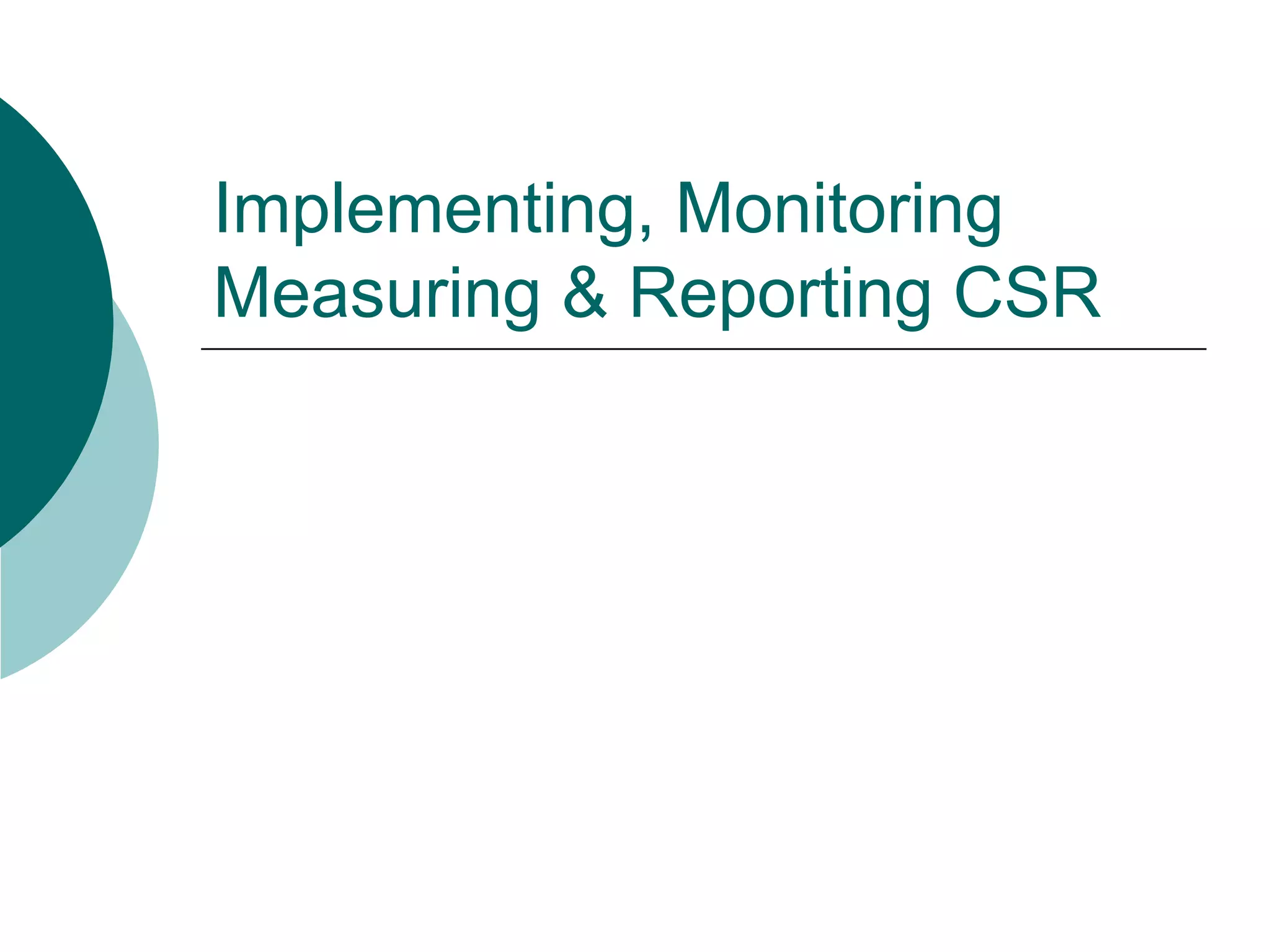

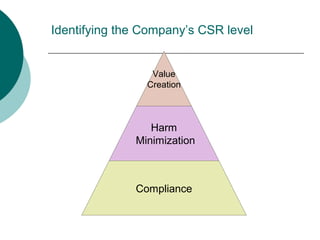

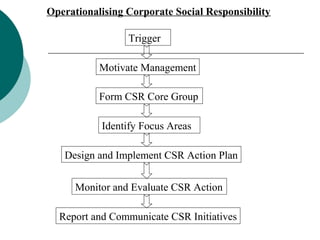

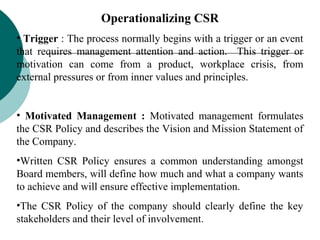

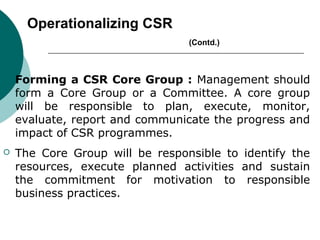

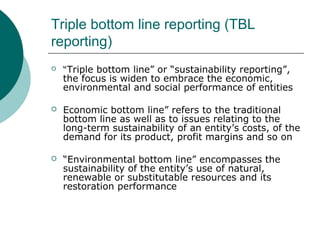

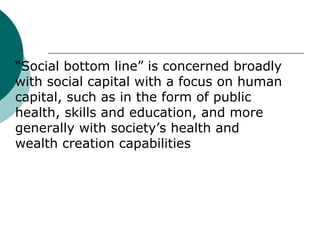

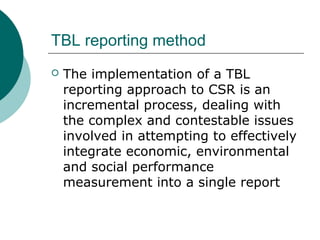

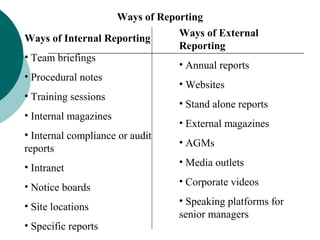

Implementing, monitoring, and reporting CSR requires identifying a company's CSR level, key requirements like commitment and resources, and operational steps. CSR should be operationalized through forming a motivated core group to identify focus areas, design action plans, monitor impacts, and report initiatives. Measuring, monitoring, and reporting CSR ensures accountability, avoids risks, and improves reputation and performance. It involves using tools like ratings, principles, and indices to benchmark performance across areas like workplace, environment, and community initiatives. Reporting provides transparency and drives progress through methods like descriptive, quantitative, full cost, and triple bottom line reporting.