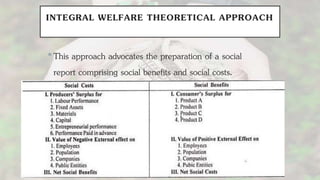

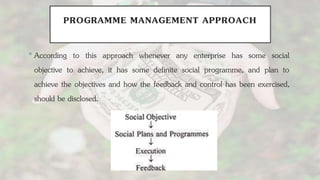

This document discusses socially responsible accounting. It presents socially responsible accounting as integrating non-financial measures into financial reporting to communicate the social and environmental effects of organizations. It aims to help companies address stakeholder accountability and improve social, environmental, and economic performance. There is no standardized model. Approaches to social accounting measurement are discussed, including the classical, descriptive, integral welfare, program management, pictorial, and footnote disclosure approaches. The objectives of social accounting are identified as identifying a firm's net social contribution, determining consistency with social priorities, developing models for social cost/benefit quantification and presentation, and meeting information needs.