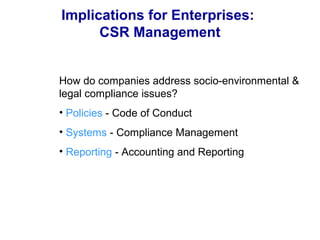

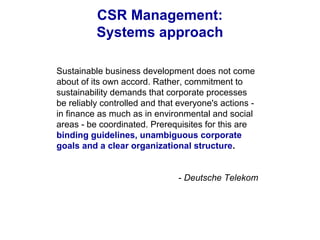

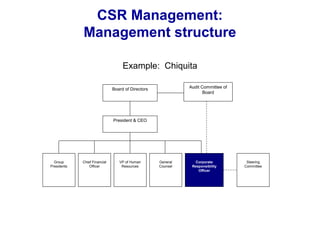

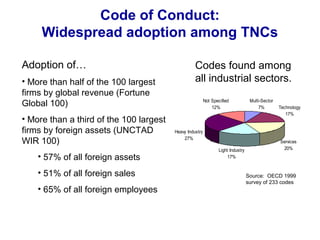

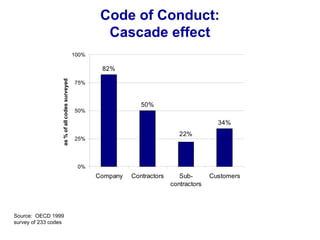

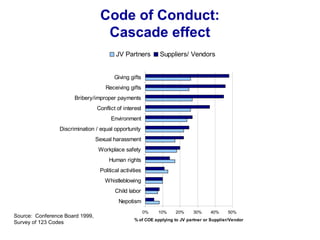

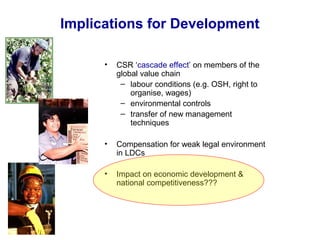

This document discusses concepts and drivers related to corporate social responsibility (CSR). It outlines key CSR concepts like social contract theory and stakeholder theory. It then examines the context of CSR globally and key drivers like NGO activism, responsible investment, litigation, and government initiatives. The document also explores implications of CSR for enterprises, like managing their value chains and sphere of influence, adopting codes of conduct, and implementing compliance and reporting systems. Finally, it discusses implications of CSR for development through its cascade effects on global value chains and members' labor and environmental practices.

![Implications for Enterprises:

TNC as an “organ of society”

“every individual and every

organ of society [should]

promote respect for these

rights and freedoms and to

secure their universal and

effective recognition.” - UN

International Declaration of Human Rights

International

principles apply only

to governments

International

principles apply to

governments and

companies

It would be a strange tort system

that imposed liability on state actors

but not on those who conspired

with them to perpetrate illegal acts

through coercive use of state

power. - 1997 Eastman Kodack Co. v. Kalvin

Trend in international law](https://image.slidesharecdn.com/csvppt2019-190718101812/85/Csv-ppt2019-15-320.jpg)

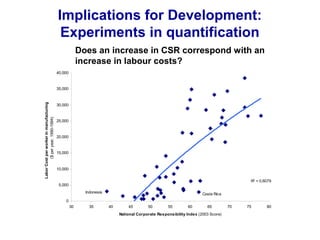

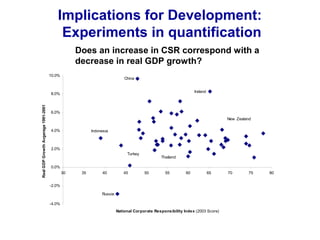

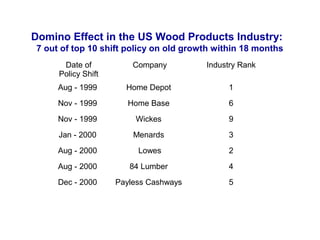

![Implications for Development:

is CSR good for growth?

“…[CSR] is liable to hold back the development of poor

countries through the suppression of employment opportunities

within them.”

David Henderson

“[CSR]’s adoption would reduce competition and economic

freedom, and undermine the market economy.”](https://image.slidesharecdn.com/csvppt2019-190718101812/85/Csv-ppt2019-40-320.jpg)