Download to read offline

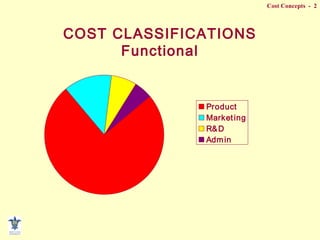

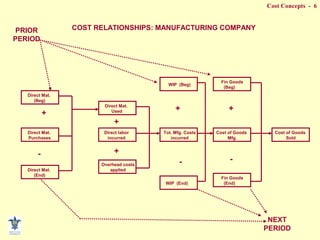

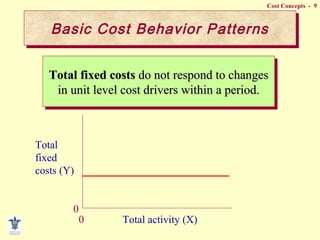

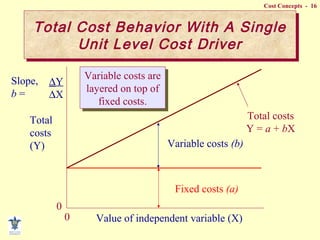

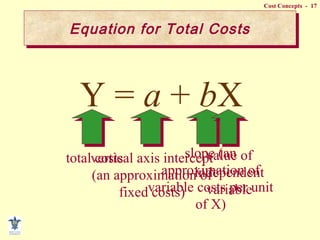

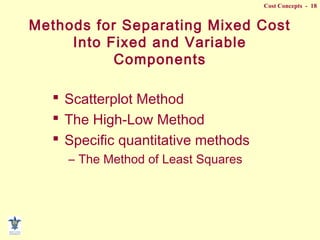

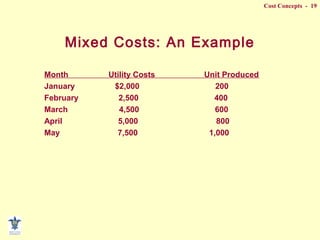

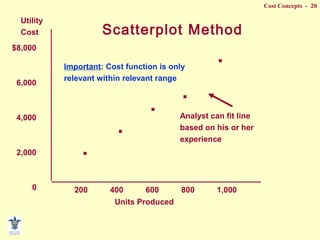

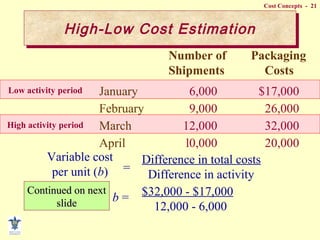

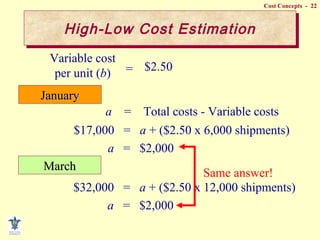

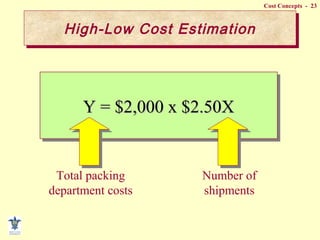

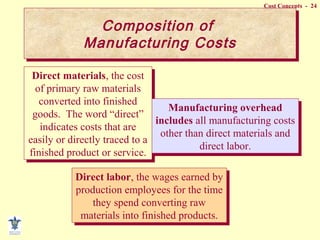

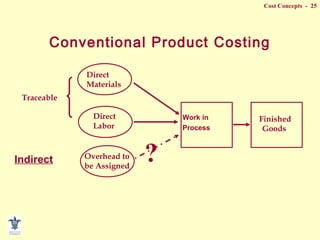

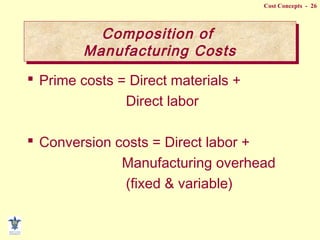

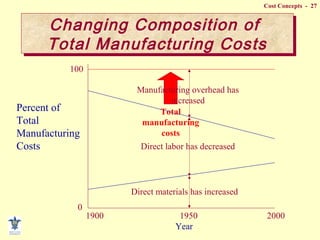

The document discusses various cost concepts and classifications including: - Fixed vs variable vs mixed costs and how they behave differently with changes in activity. - Functional classifications like product, marketing, R&D costs. - Behavioral classifications like committed vs discretionary fixed costs. - Responsibility classifications that assign costs to cost centers like departments A, B, C. - Composition of manufacturing costs including direct materials, direct labor, and manufacturing overhead. - Methods for separating mixed costs into fixed and variable components like scatterplot, high-low, and least squares.

![COMPONENT OF COST BY G.DINESHPIRAN [DP]](https://cdn.slidesharecdn.com/ss_thumbnails/ppceyuvraj-170819104226-thumbnail.jpg?width=640&height=640&fit=bounds)