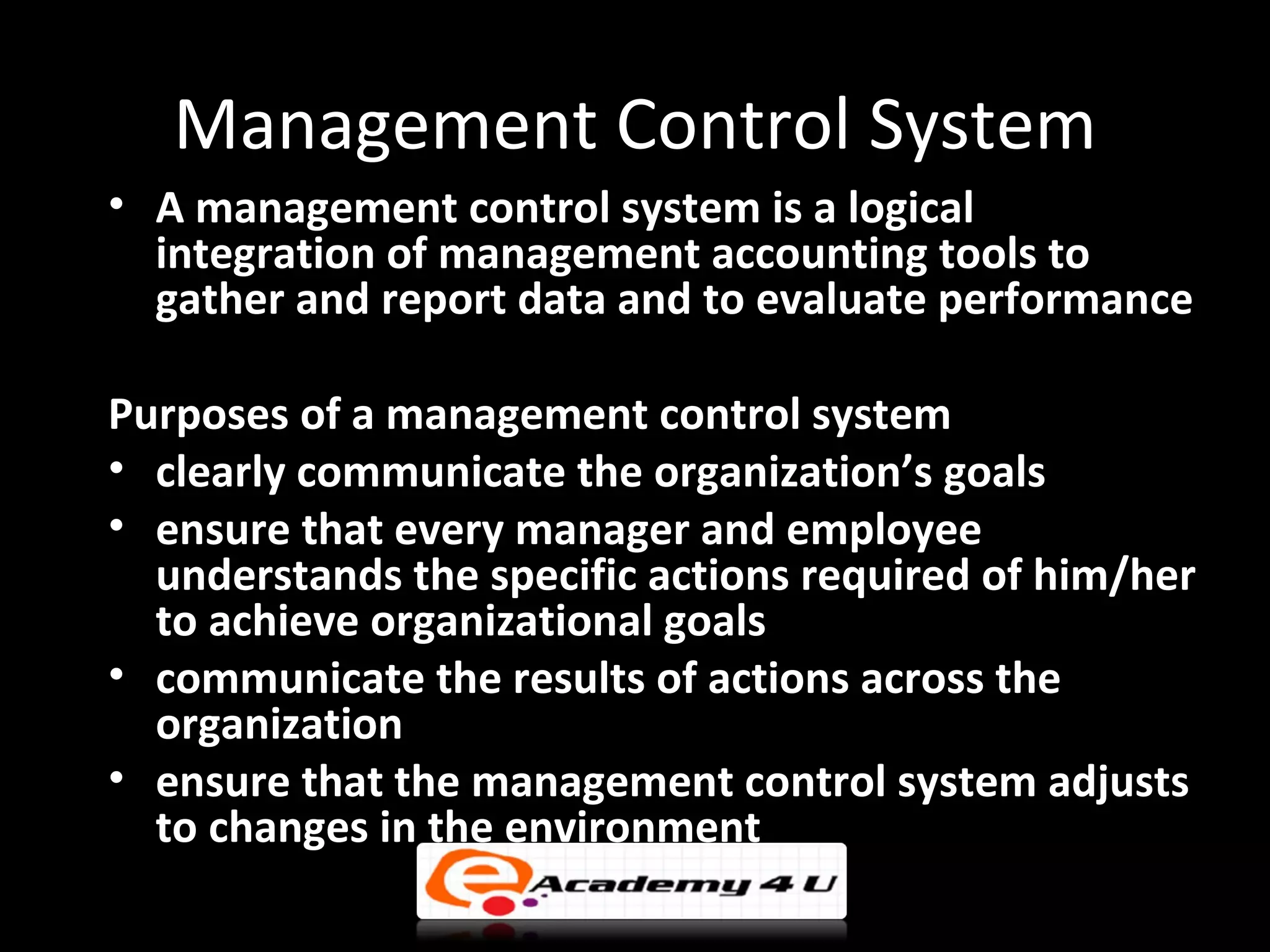

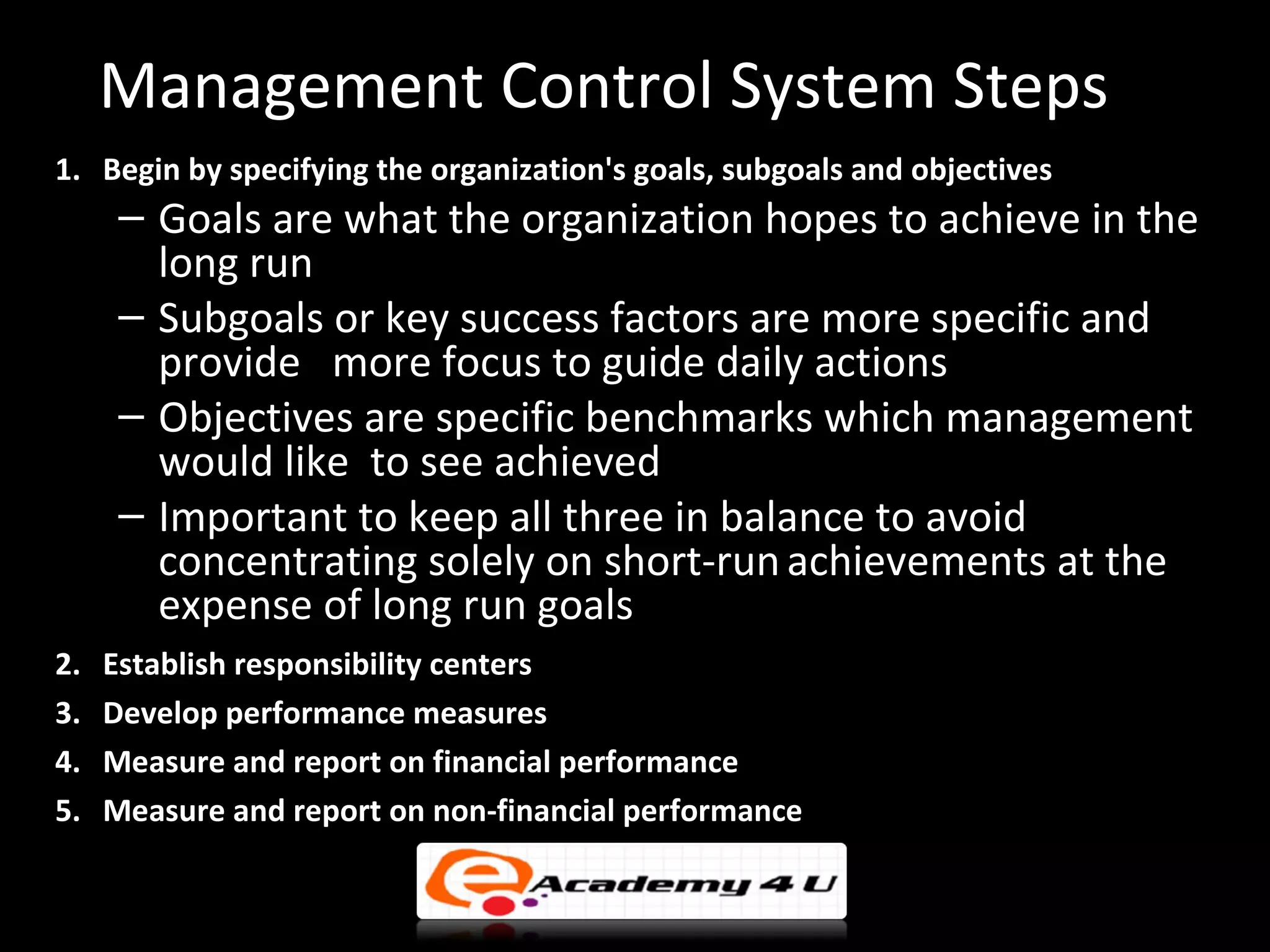

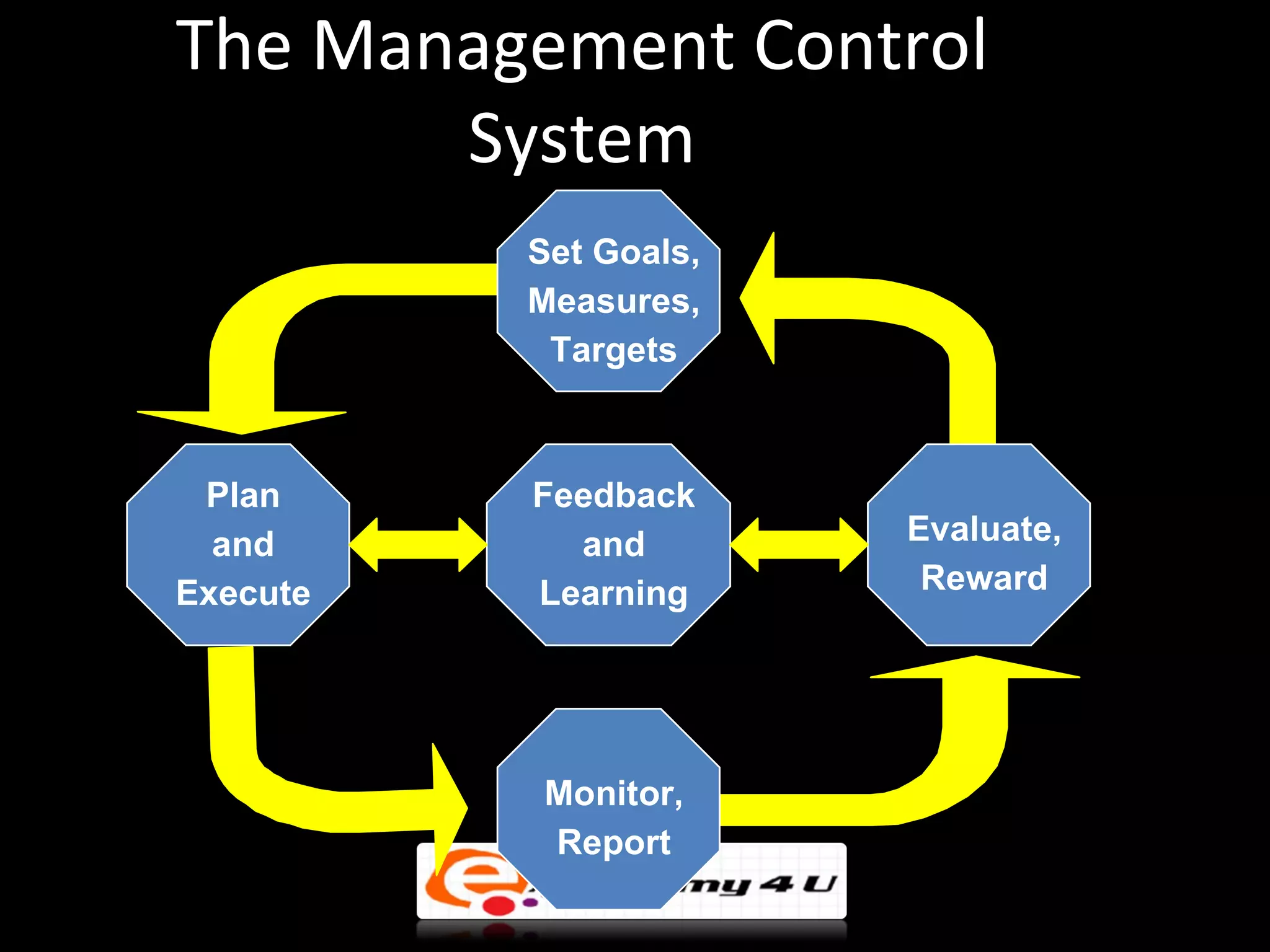

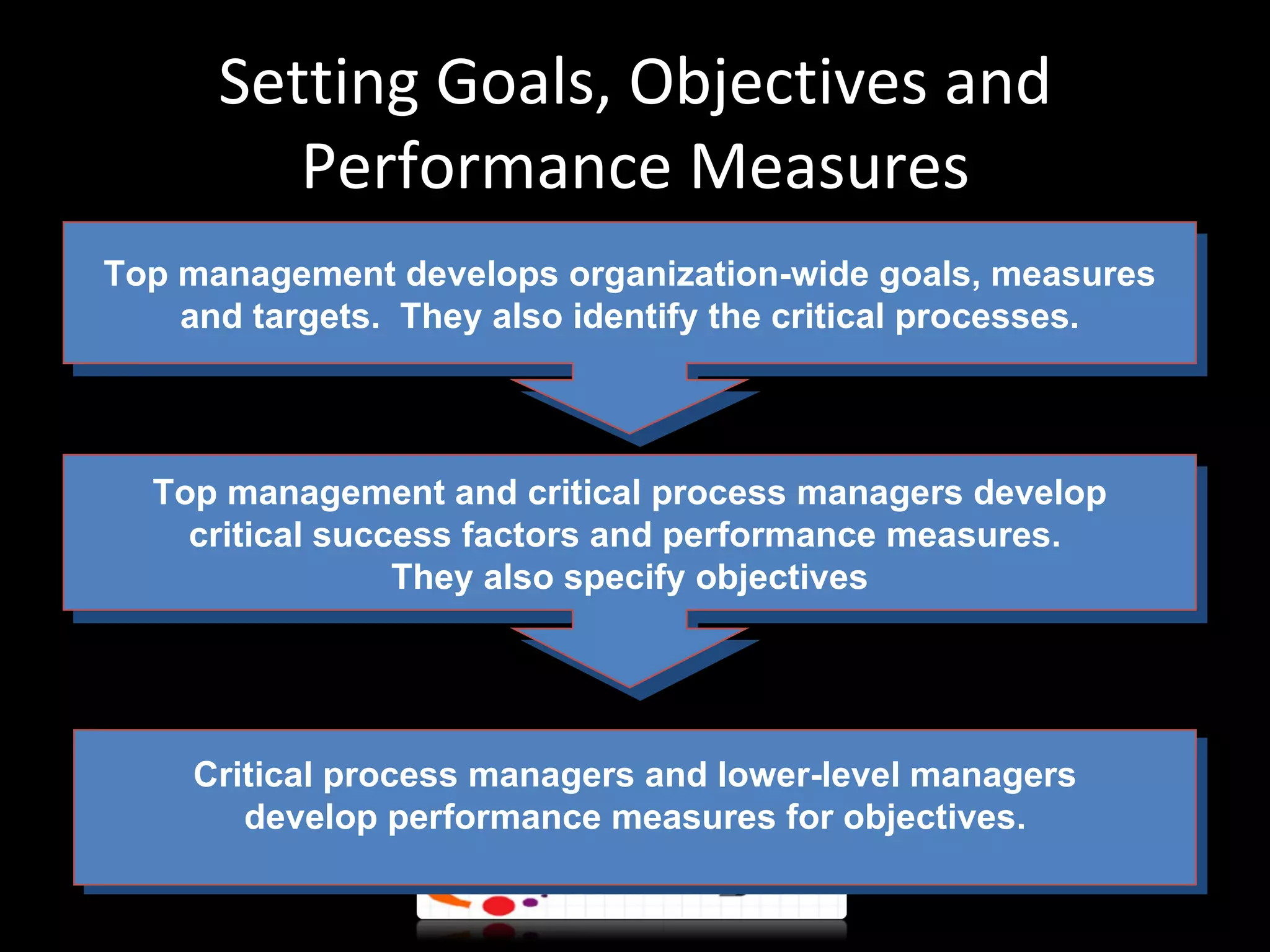

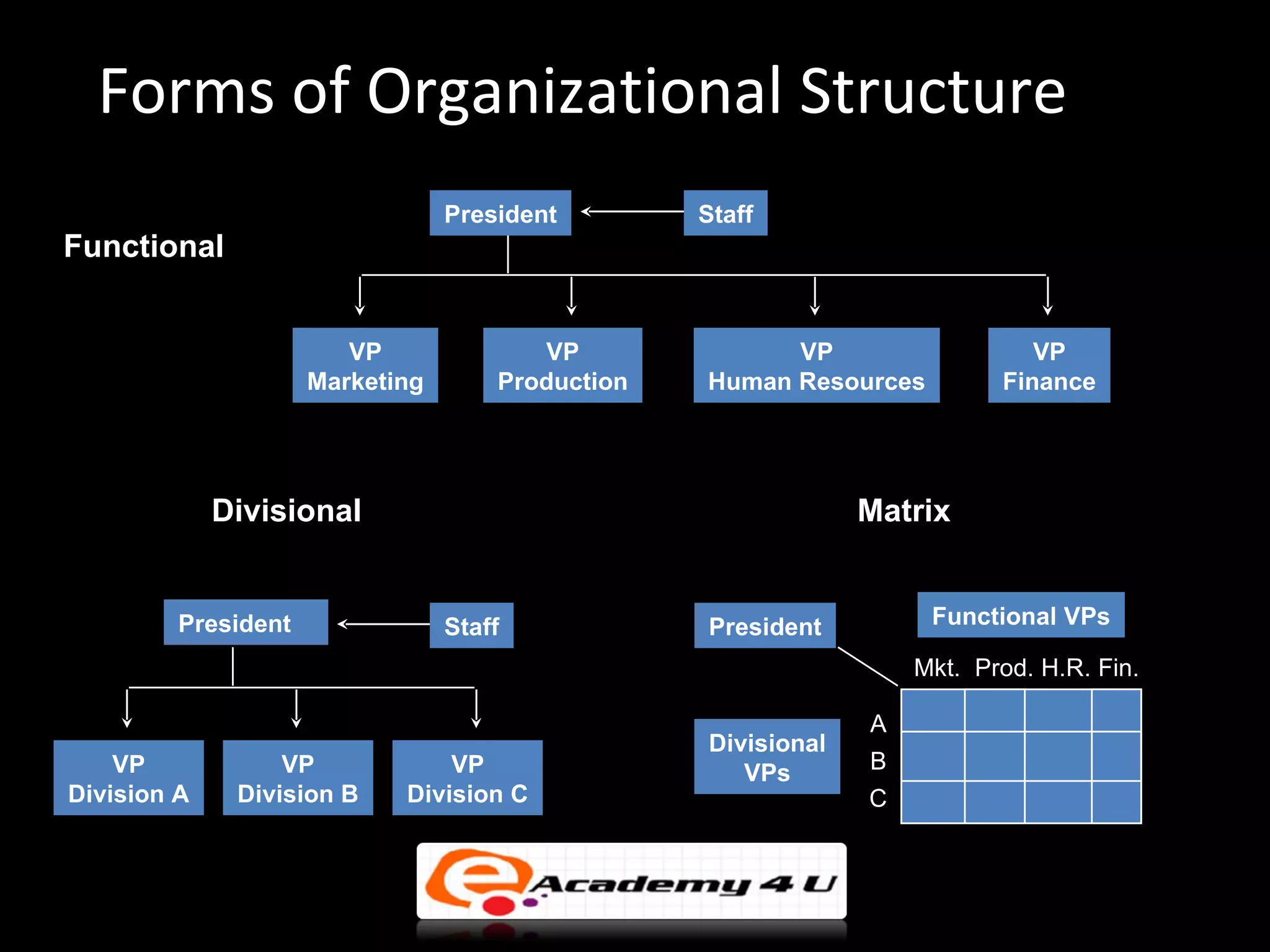

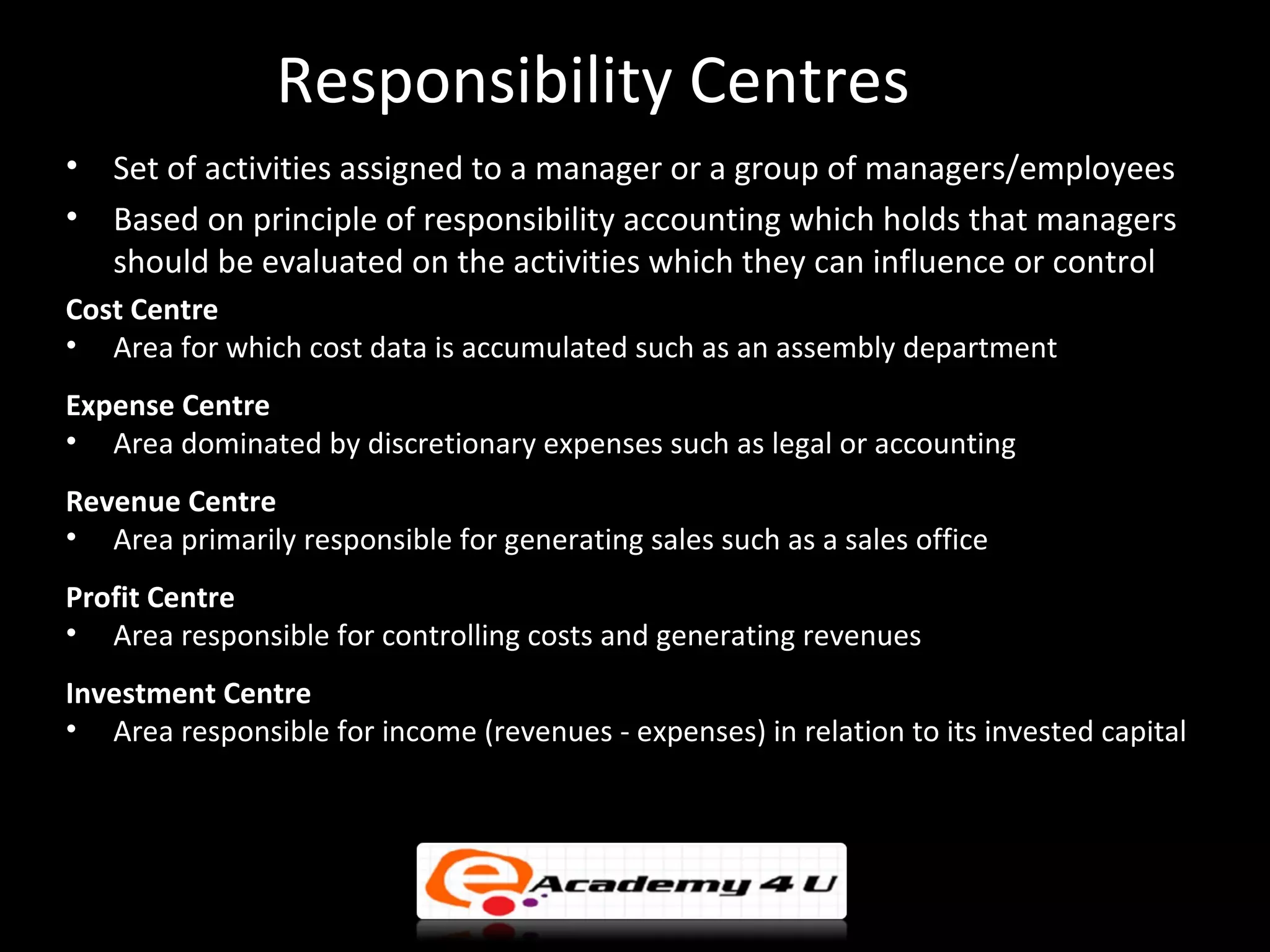

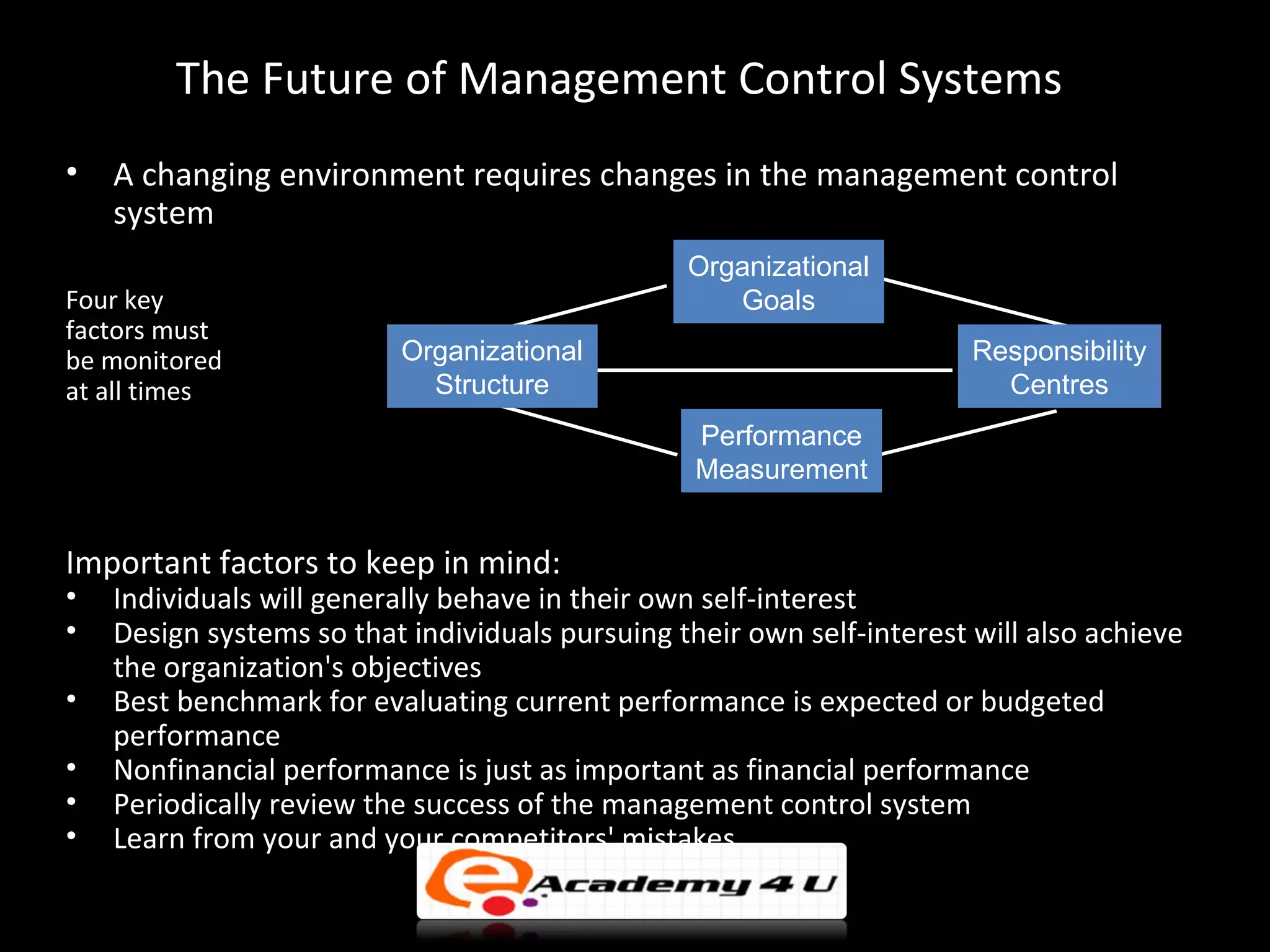

A management control system integrates accounting tools to set goals, measure performance, and evaluate results to ensure managers and employees work to achieve organizational objectives; it establishes responsibility centers, develops financial and non-financial performance measures, and provides feedback to adjust to changes. The document outlines the key components of an effective management control system, including specifying goals and objectives, measuring controllable costs and uncontrollable costs, using both financial and non-financial metrics, and periodically reviewing the system.