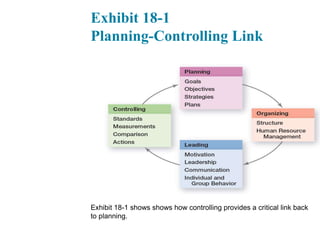

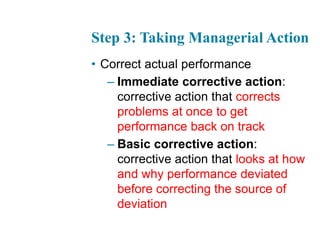

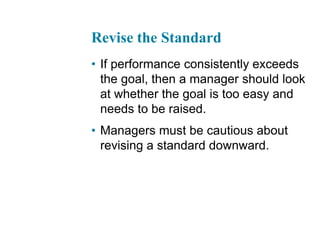

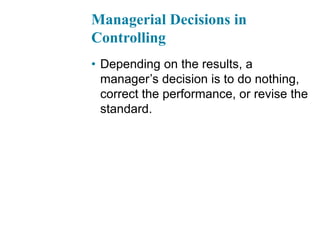

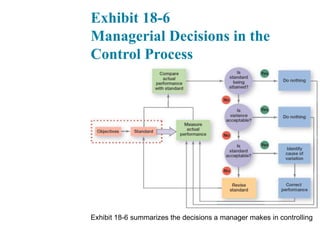

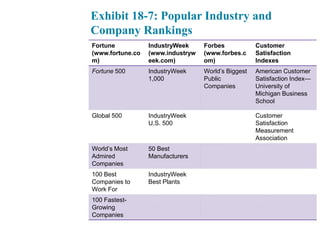

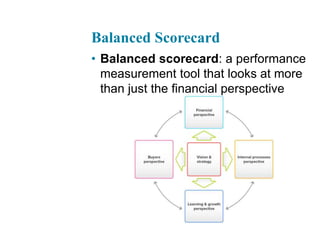

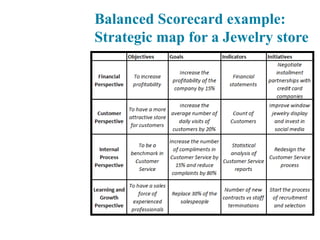

Controlling is the management function of monitoring, comparing, and correcting work performance. It is important for ensuring goals are met, providing feedback, and protecting the organization. The control process involves three steps - measuring actual performance, comparing it to standards, and taking action to correct deviations. Organizational and employee performance can be measured through productivity, effectiveness, and industry/company rankings. Tools for measuring organizational performance include financial controls, information controls, balanced scorecards, and benchmarking of best practices. Contemporary control issues include cross-cultural differences, workplace privacy, and adjusting controls for global operations.