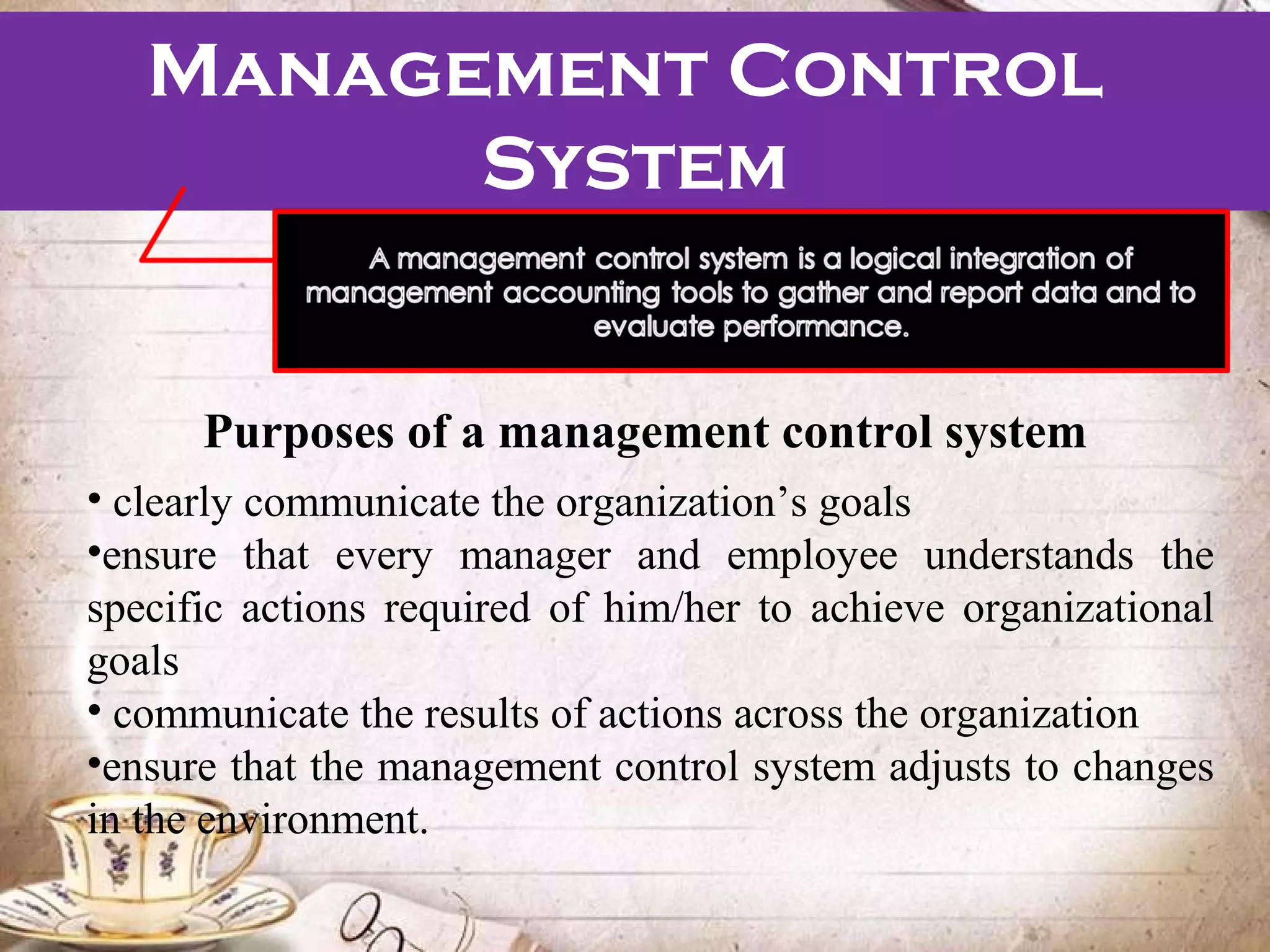

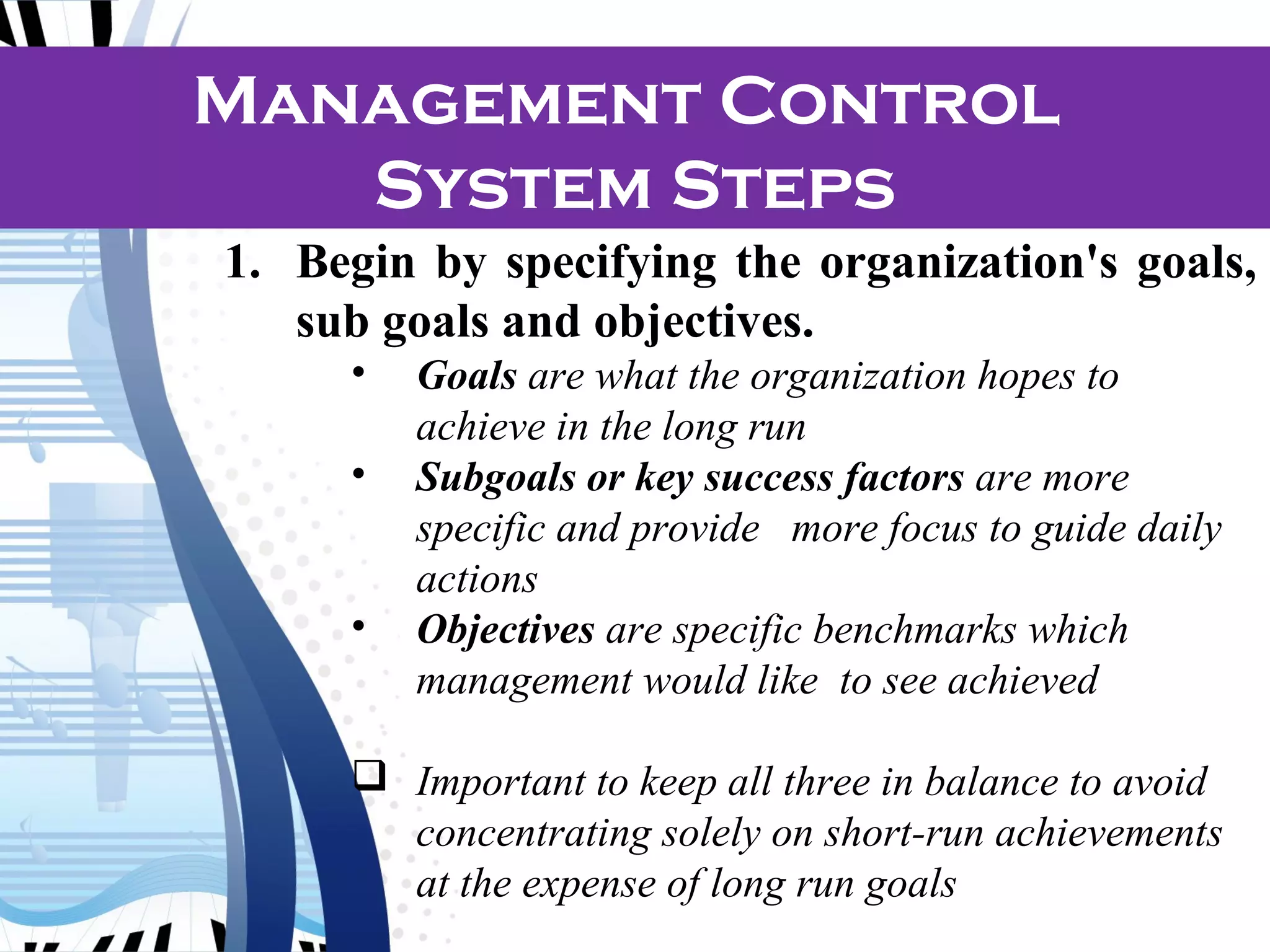

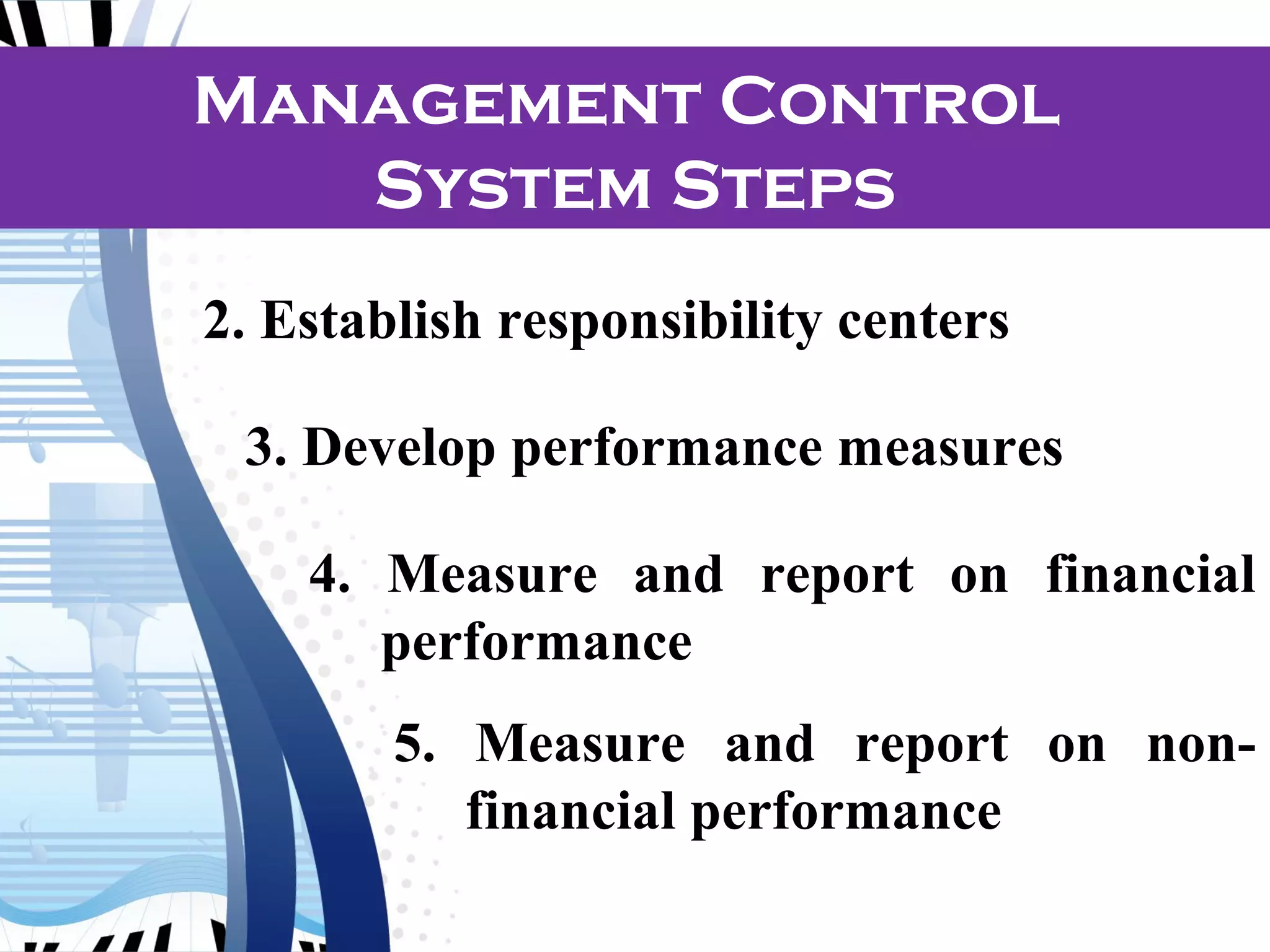

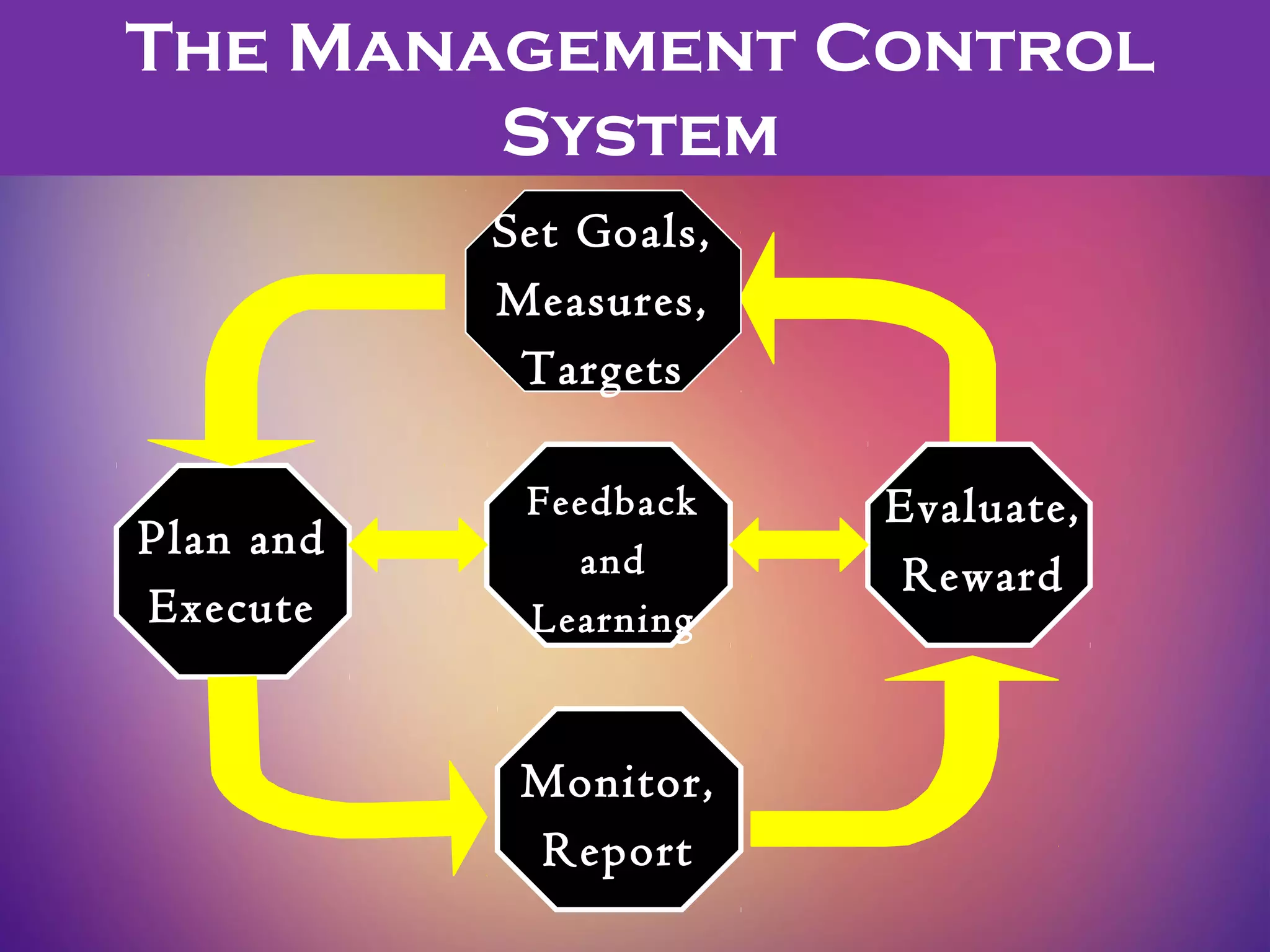

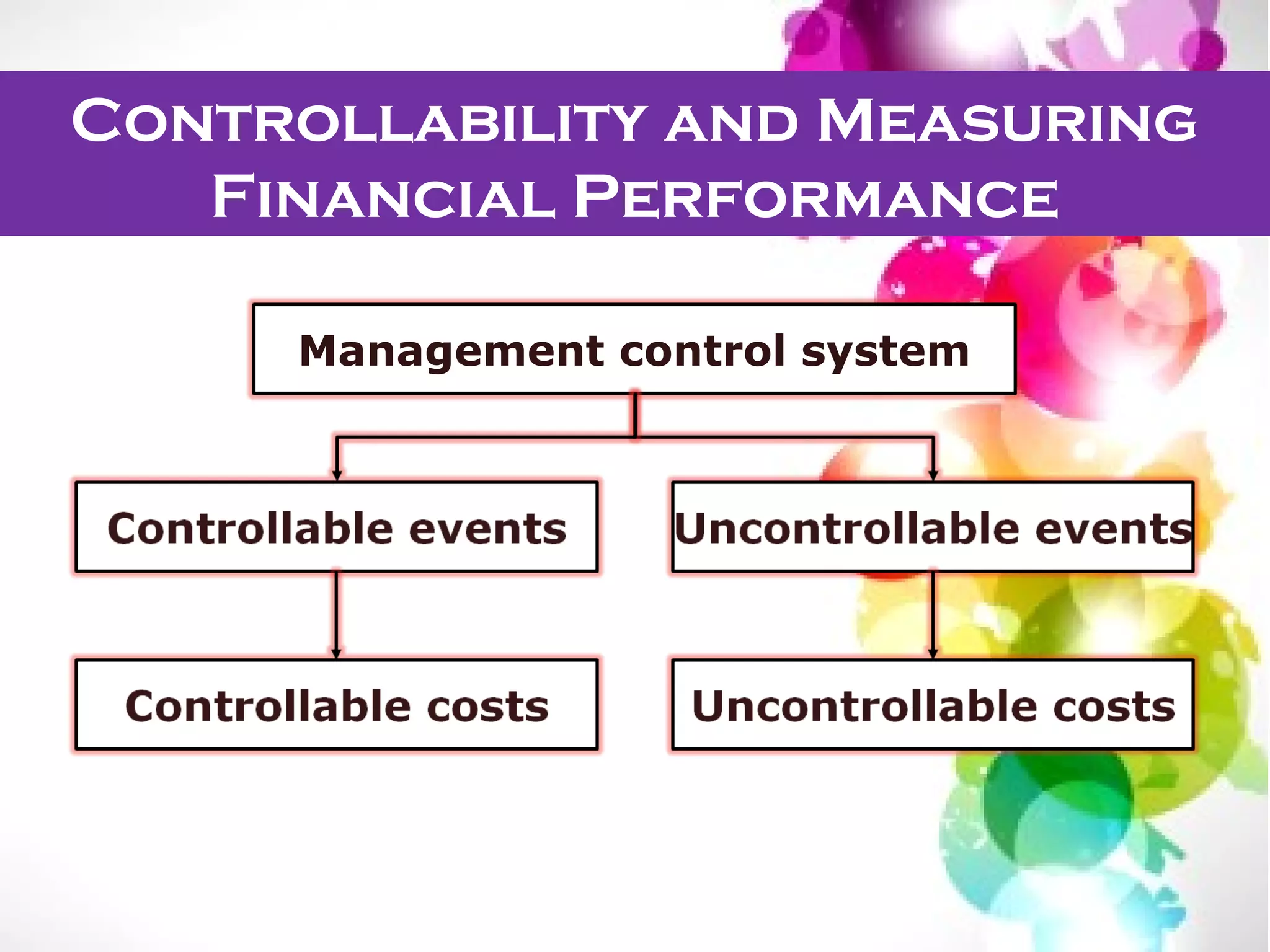

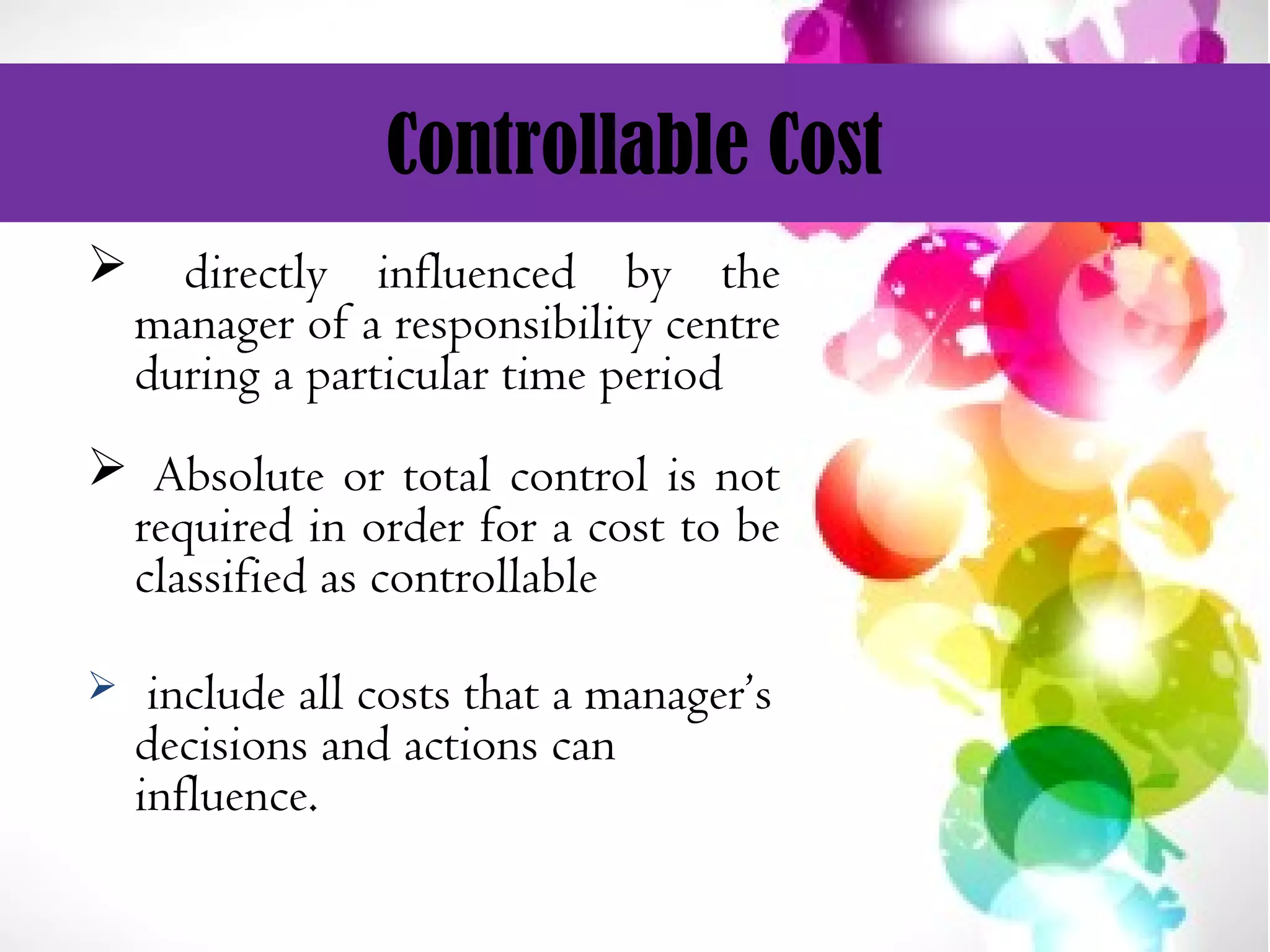

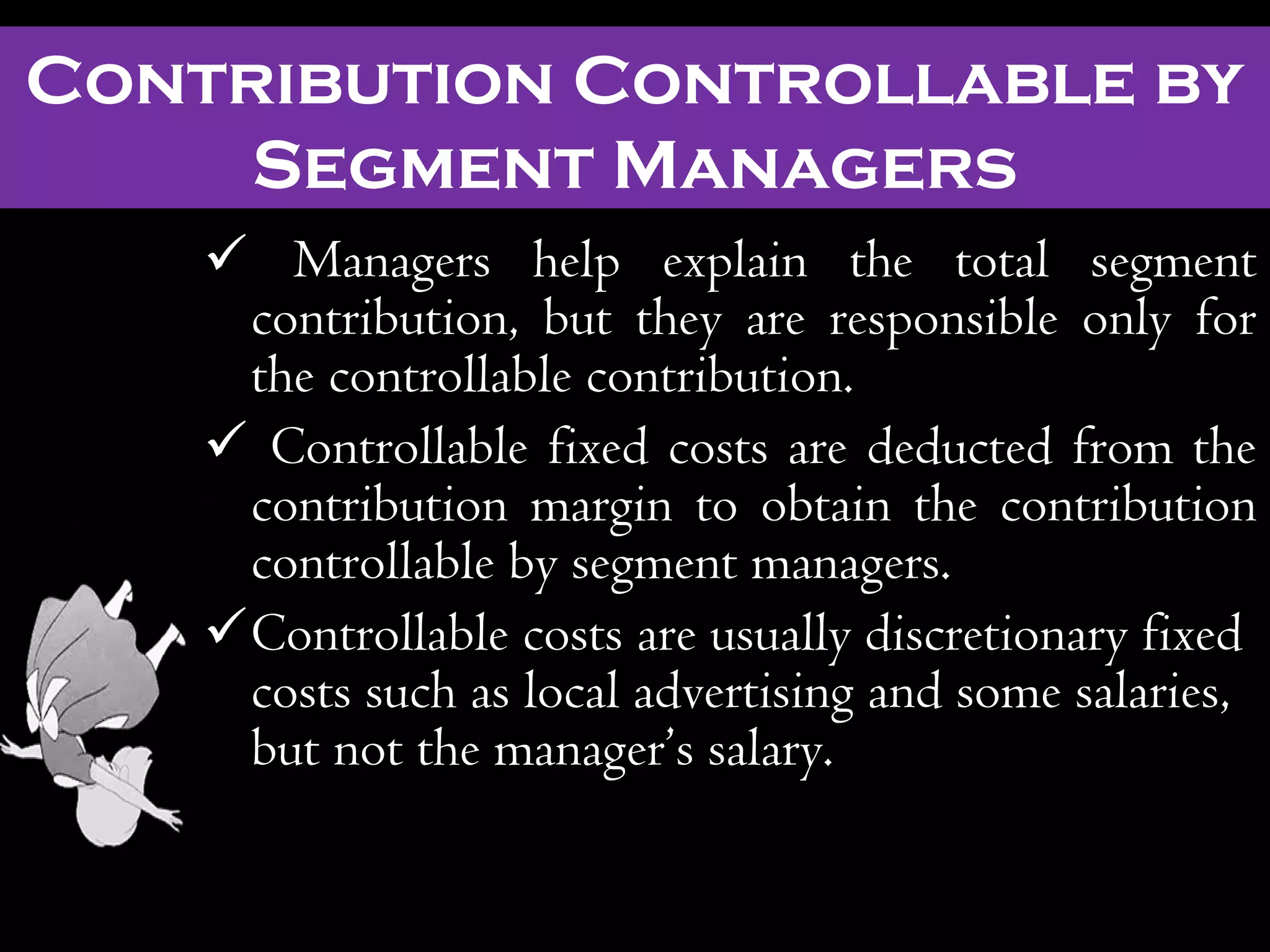

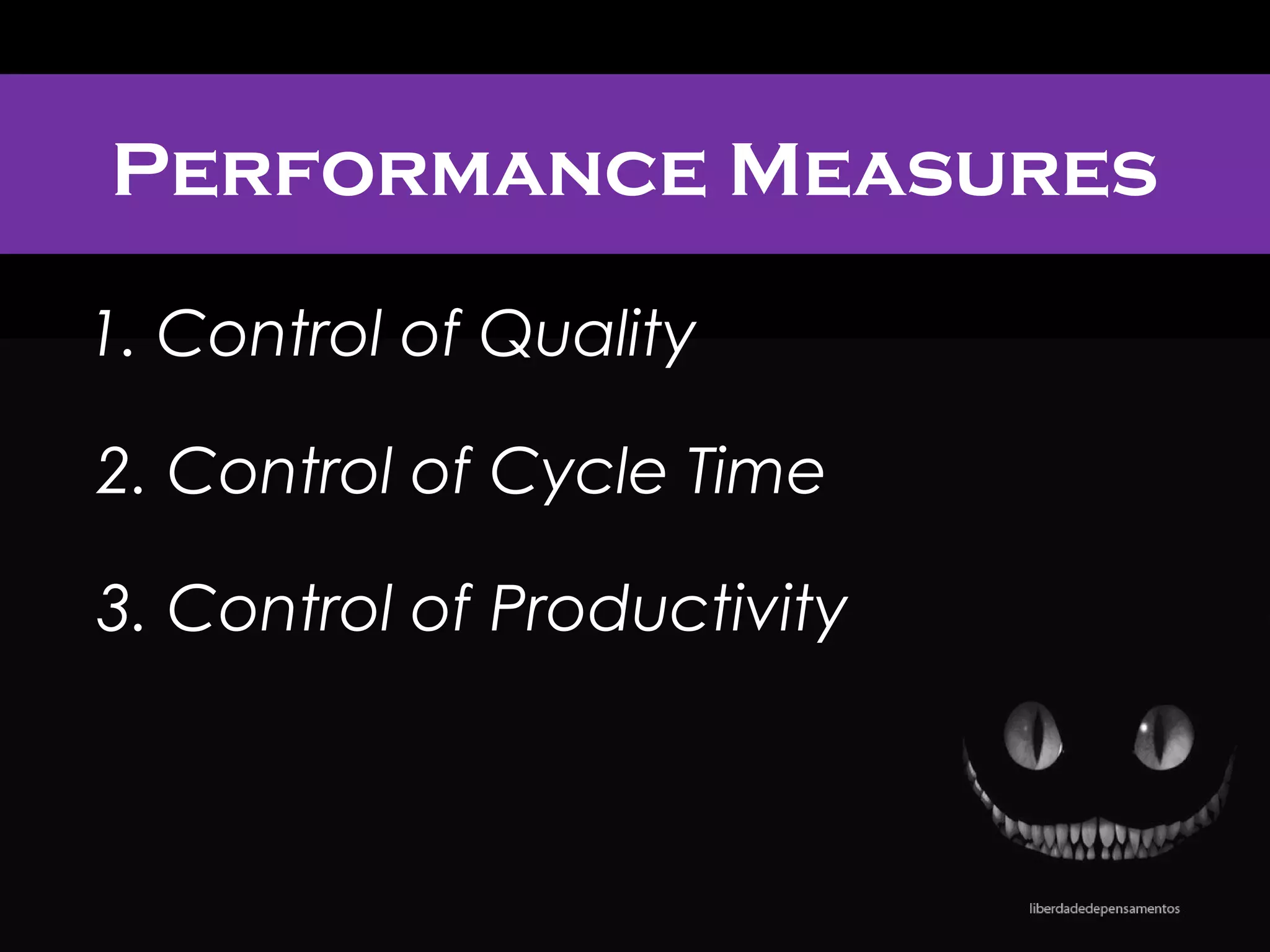

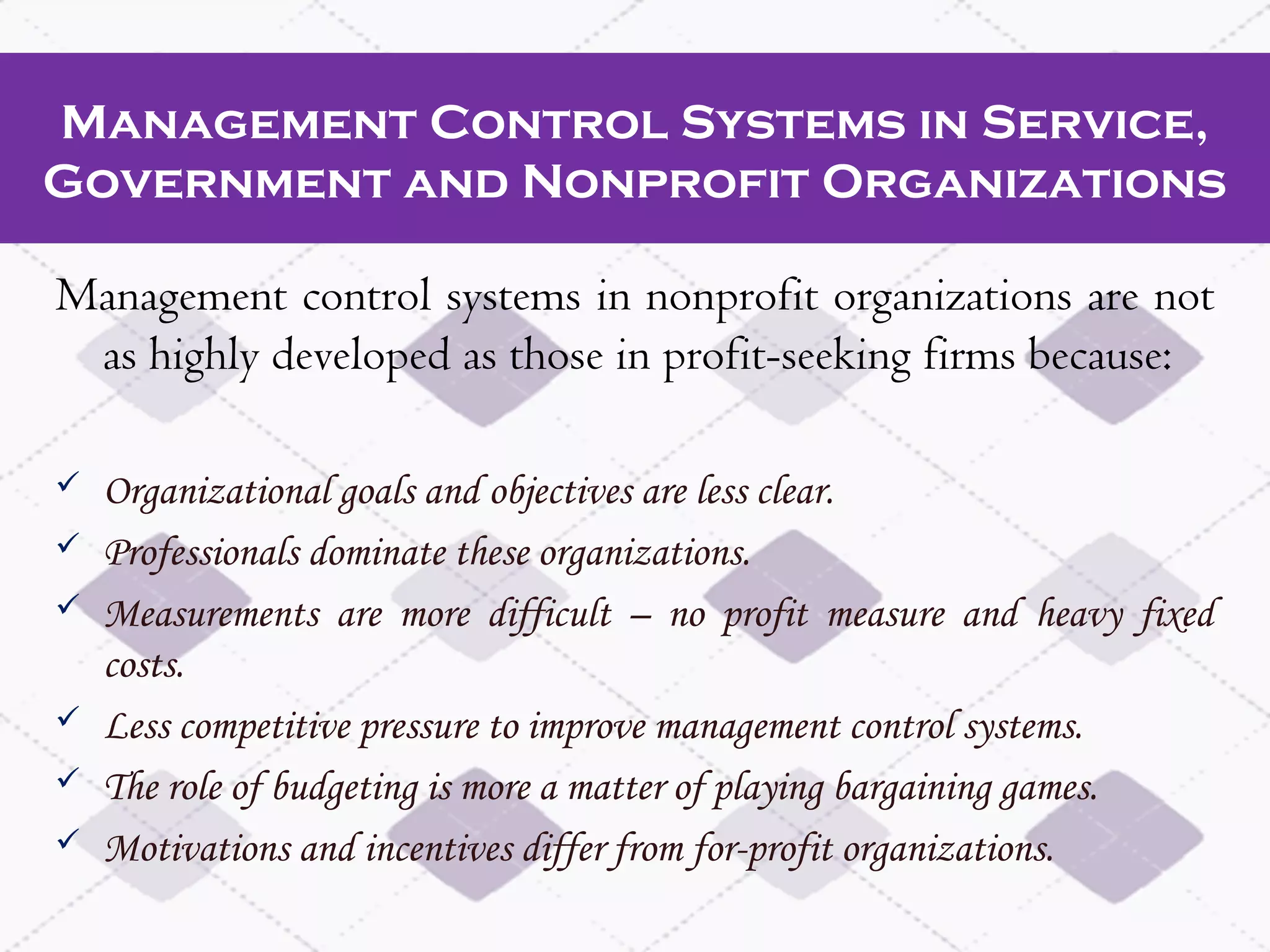

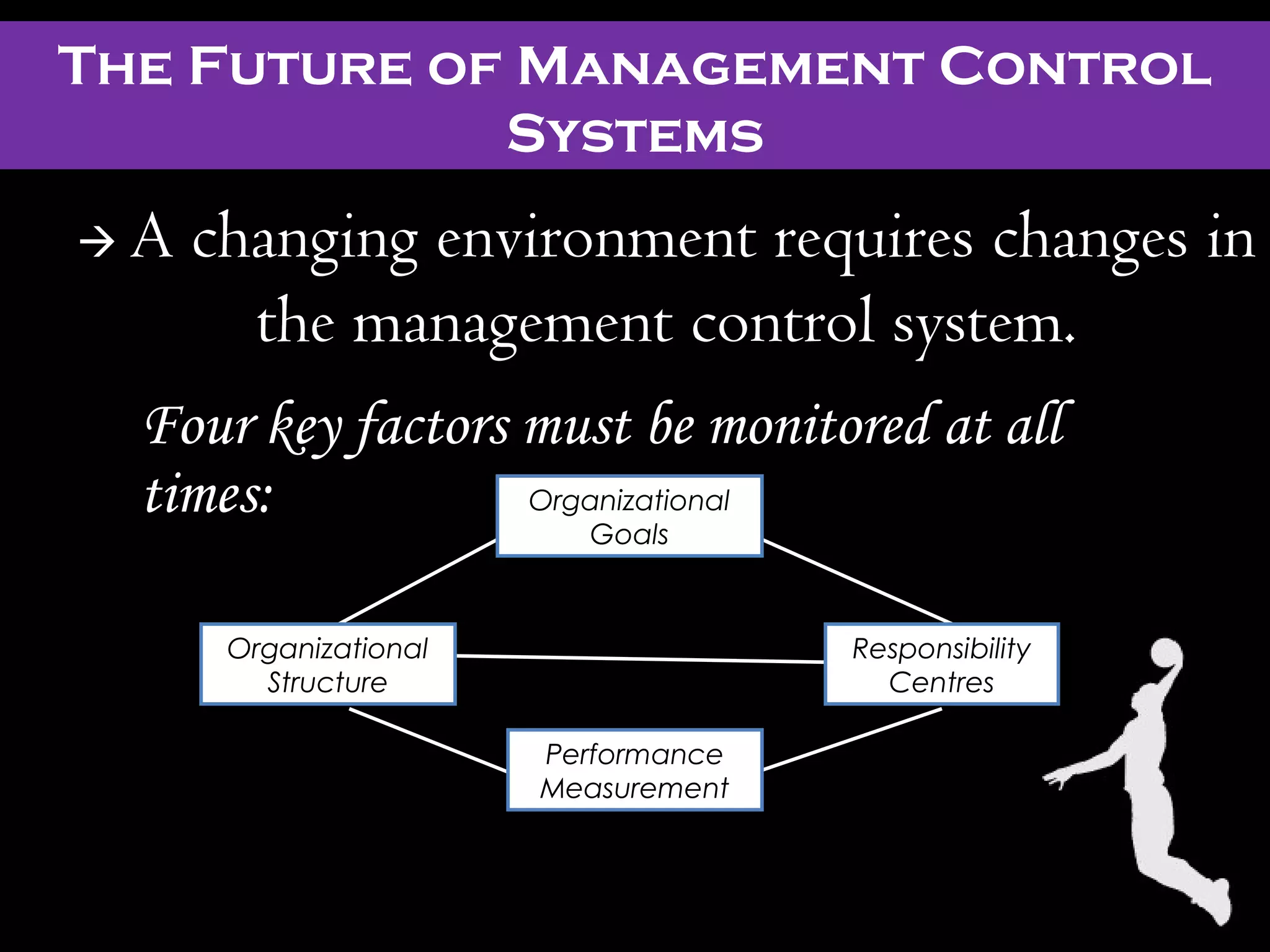

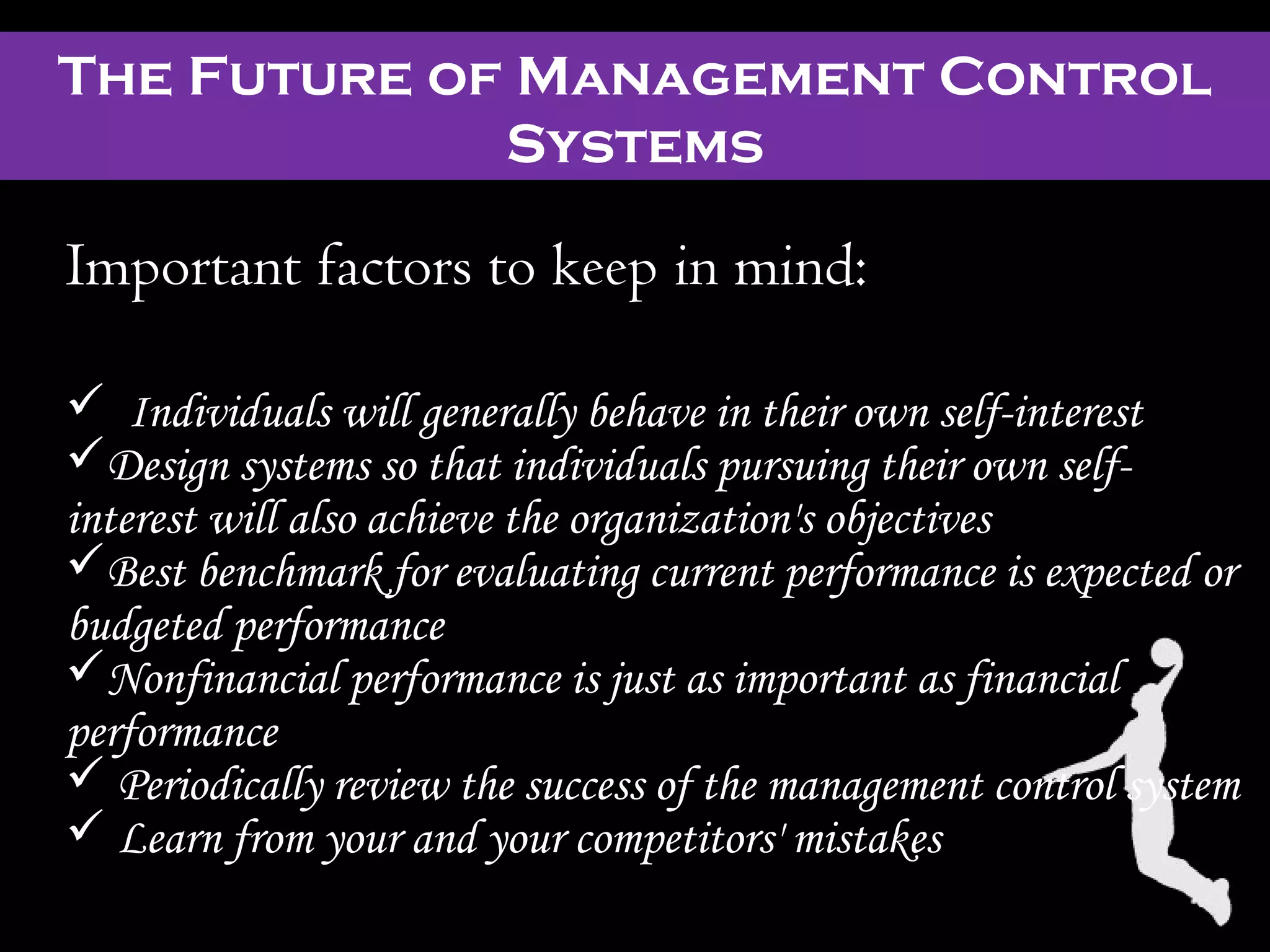

Management control systems have several key purposes: clearly communicating organizational goals; ensuring managers understand required actions; communicating results; and adjusting to environmental changes. They involve specifying goals/objectives; establishing responsibility centers; developing financial and non-financial performance measures; monitoring/reporting performance; and evaluating/rewarding. Performance is measured through quality, cycle time, and productivity controls. The future of management control systems requires adapting the organizational structure, goals, responsibility centers, and performance measurements to a changing environment.