Downloaded 2,400 times

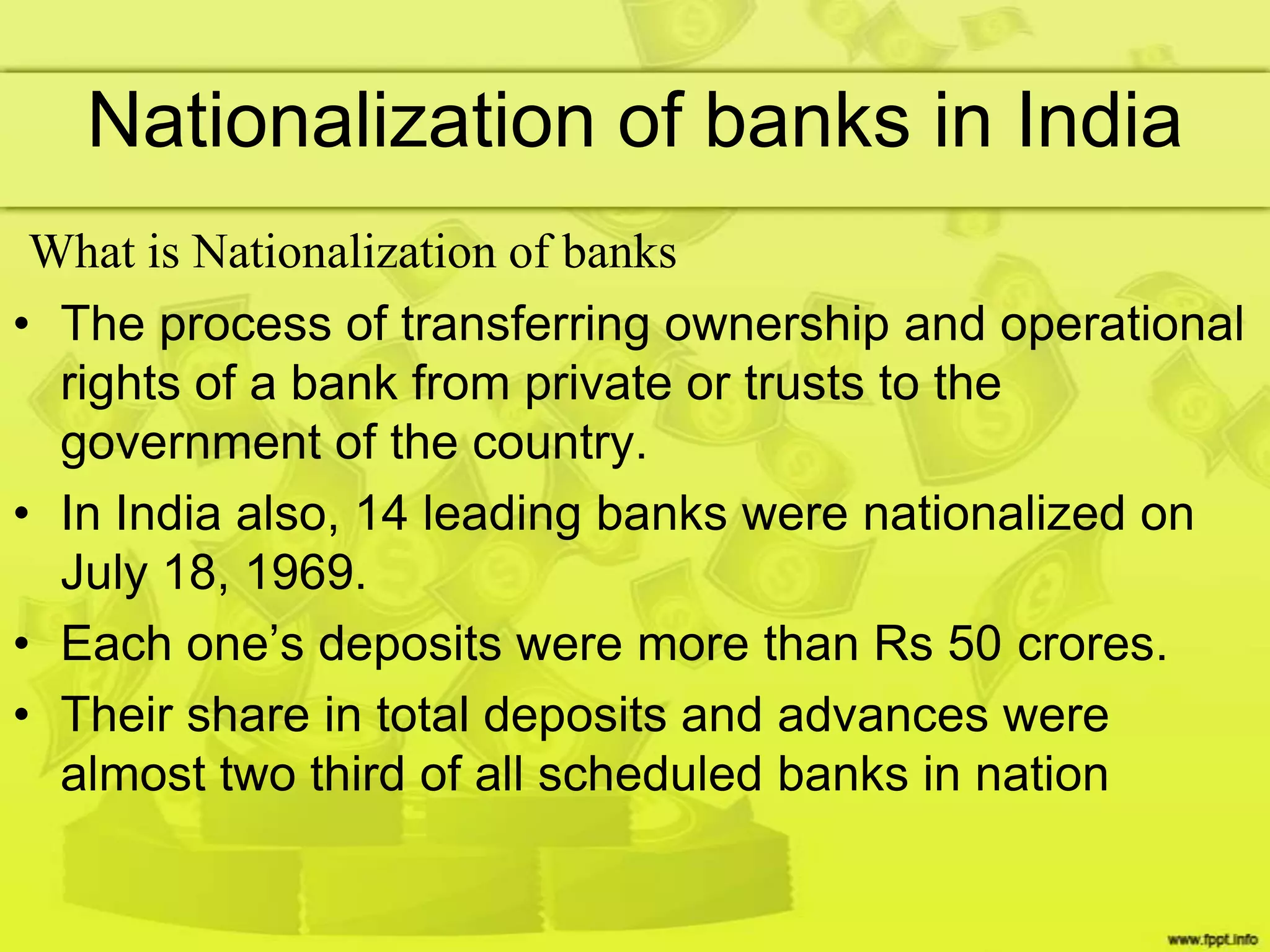

Commercial banks in India accept deposits and provide loans and other financial services. The key functions of commercial banks are accepting deposits, advancing loans, discounting bills of exchange, and providing agency and general services. In 1969 and 1980, the Indian government nationalized several large commercial banks to increase access to credit in rural and underserved areas and promote equitable development. The objectives of nationalization were to reduce economic concentration, mobilize resources nationwide, and fulfill the credit needs of small businesses and farmers.