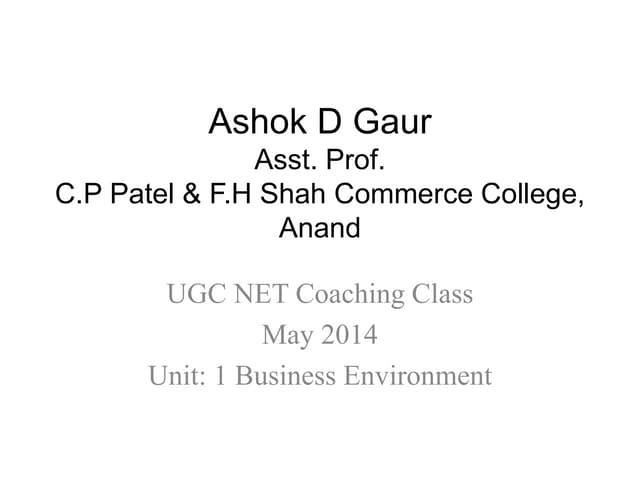

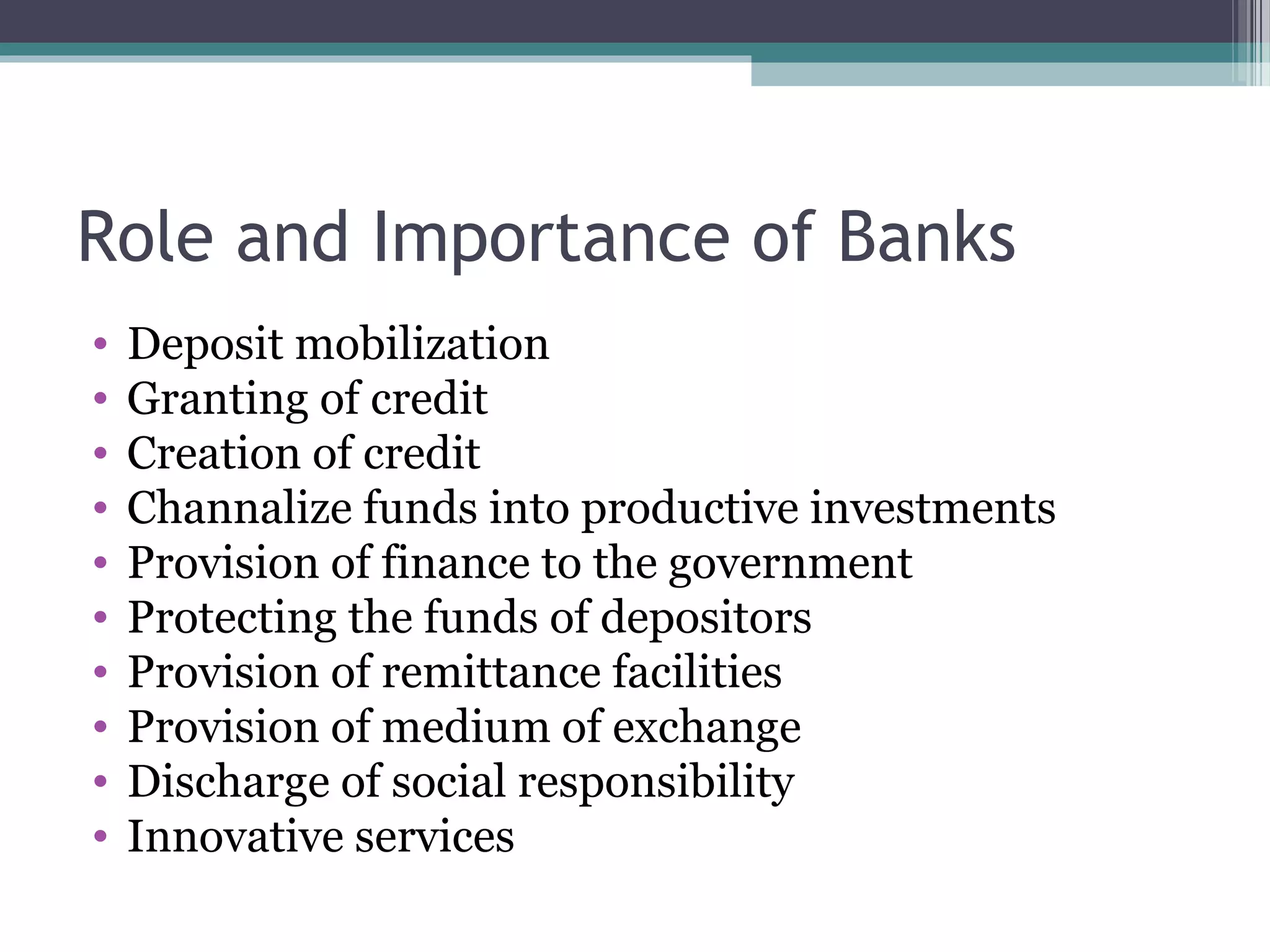

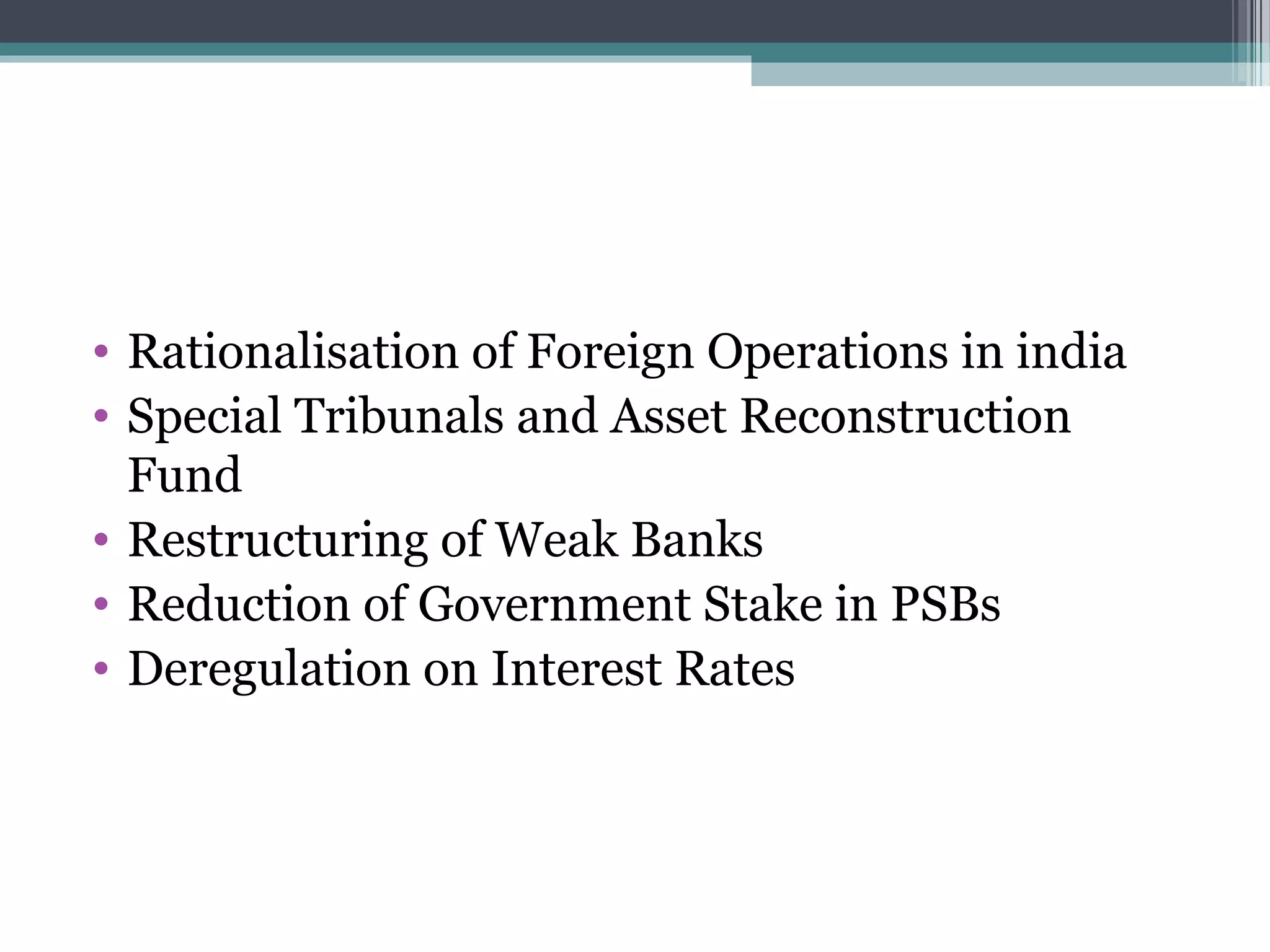

![Acts relating to banks

• Banking [Regulation] Act, 1949

• Deposit Insurance Corporation Act, 1961

• Industrial Development Bank of India Act, 19

• Export-Import Bank of India Act, 1981

• Industrial Reconstruction Bank of India Act, 1984

• National Housing Bank Act, 1987

• Regional Rural Banks Act, 1976

• Reserve Bank of India Act, 1934

• Small Industries Development Bank of India Act,

1989

• State Bank of India Act, 1955](https://image.slidesharecdn.com/bankingandfinancialinstitutions-120930112918-phpapp02/75/Banking-and-Financial-Institutions-as-per-UGC-NET-syllabus-10-2048.jpg)

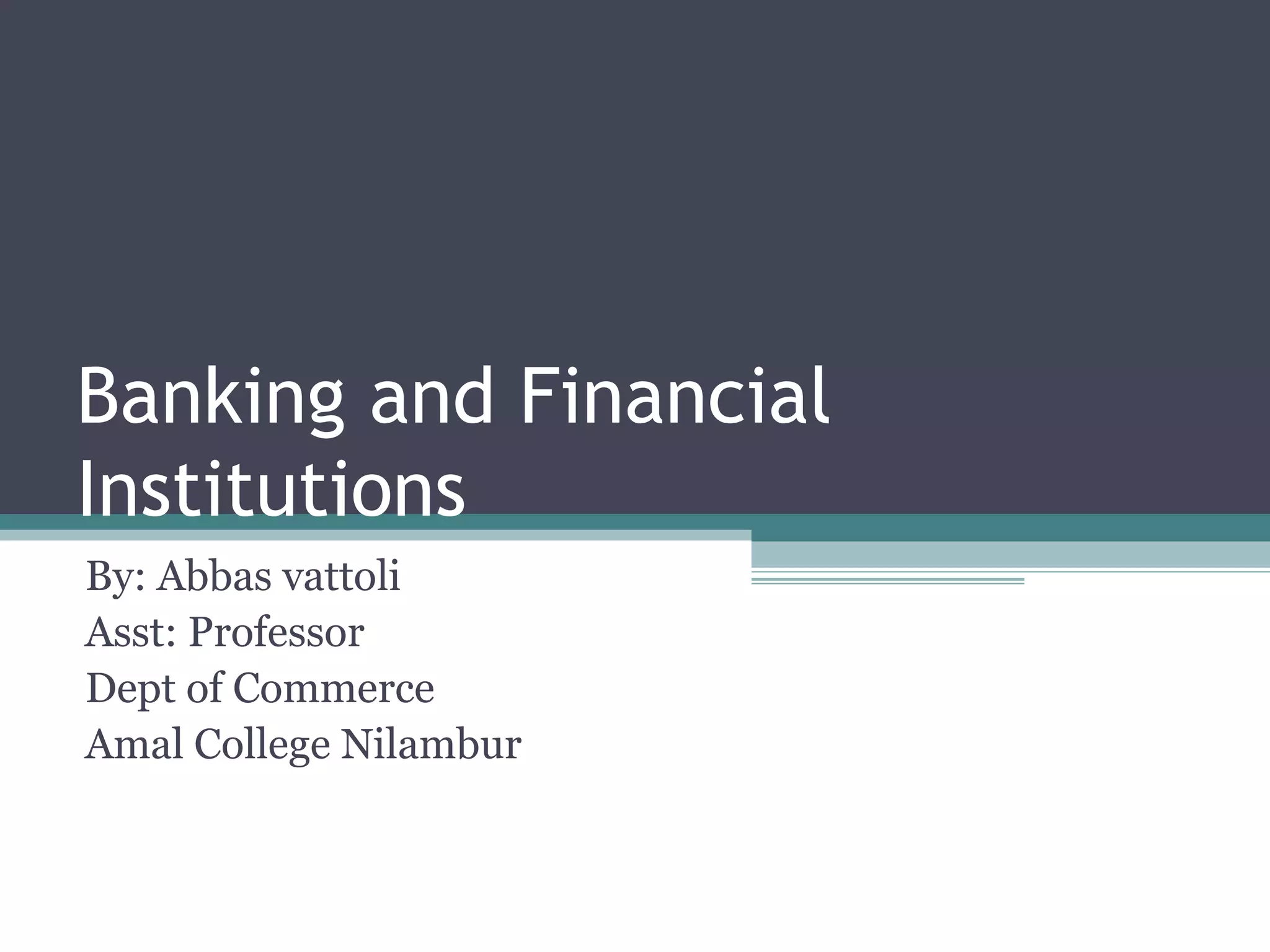

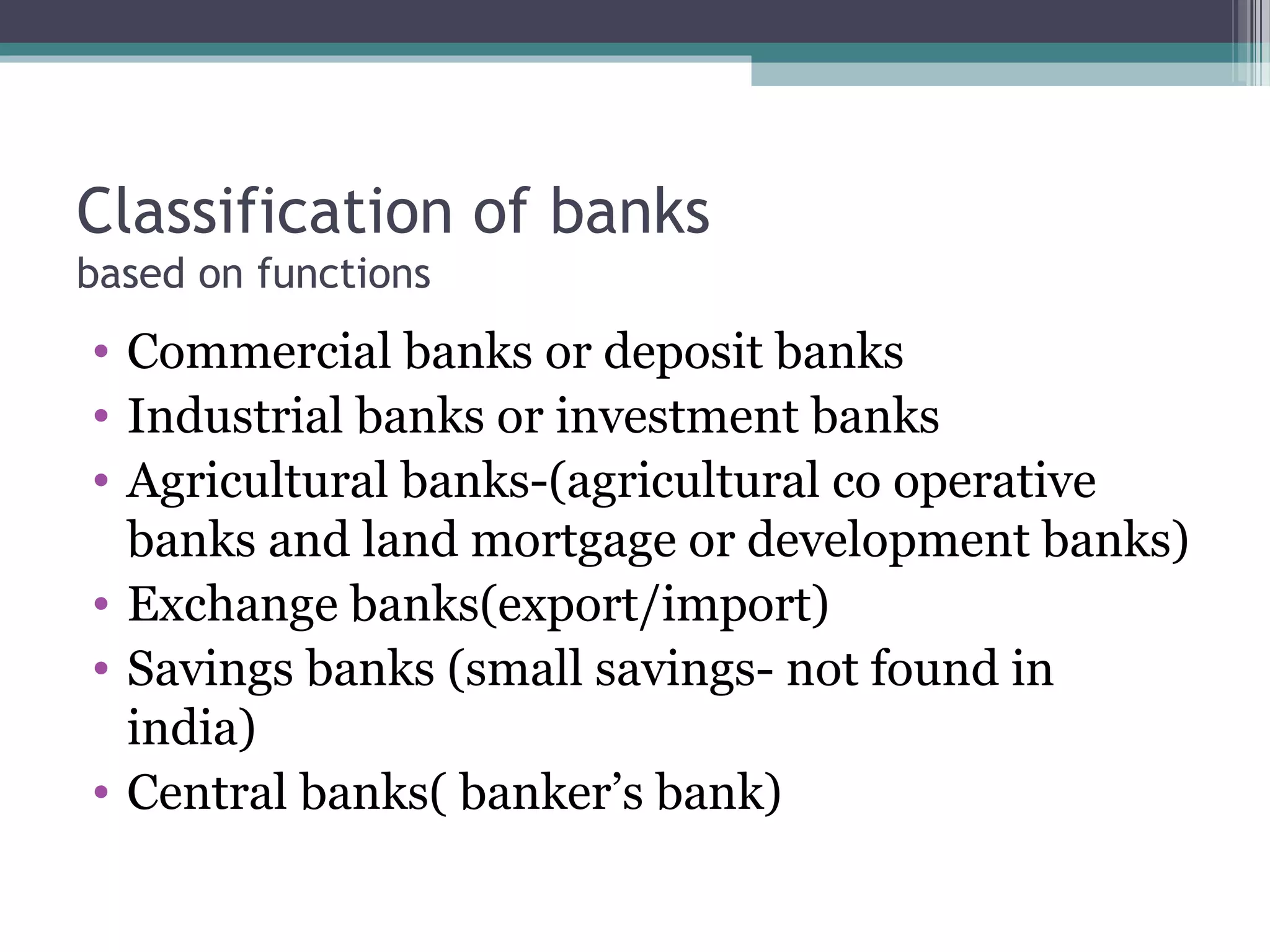

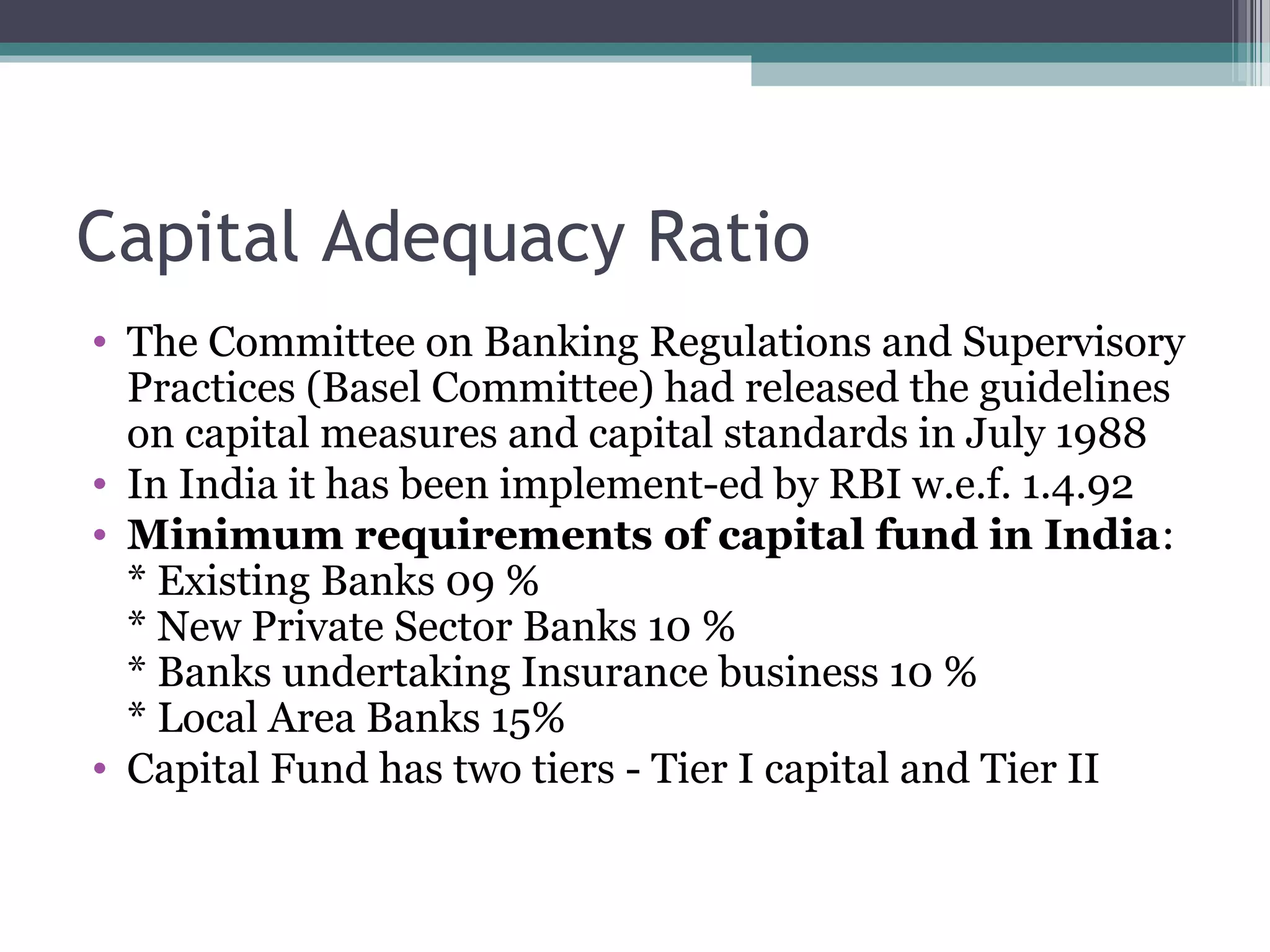

![NABARD’s Initiatives

• SHG Bank linkage programme started as a pilot project

in 1992 with 500 SHGs

• Farmers Clubs

• Rural Infrastructure Development Fund (RIDF)

• Watershed Development 1999-2000

• Rural Innovation Fund in association with Swiss Agency

for Development and Cooperation (SDC)

• agreements for co-financing with 14 commercial banks

2006-07

• Kisan Credit Card

• NABARD Consultancy Services (Nabcons)

• NABARD Financial Services Limited, [NABFINS]](https://image.slidesharecdn.com/bankingandfinancialinstitutions-120930112918-phpapp02/75/Banking-and-Financial-Institutions-as-per-UGC-NET-syllabus-51-2048.jpg)

The document provides an extensive overview of banking and financial institutions, outlining key definitions, historical evolution, functions, and regulations in India. It discusses the roles of different types of banks, including commercial and central banks, and covers banking operations such as credit control, managing non-performing assets (NPA), and the impact of banking reforms. Additionally, it highlights the significance of technological advancements like e-banking and the role of institutions like NABARD in promoting rural development.