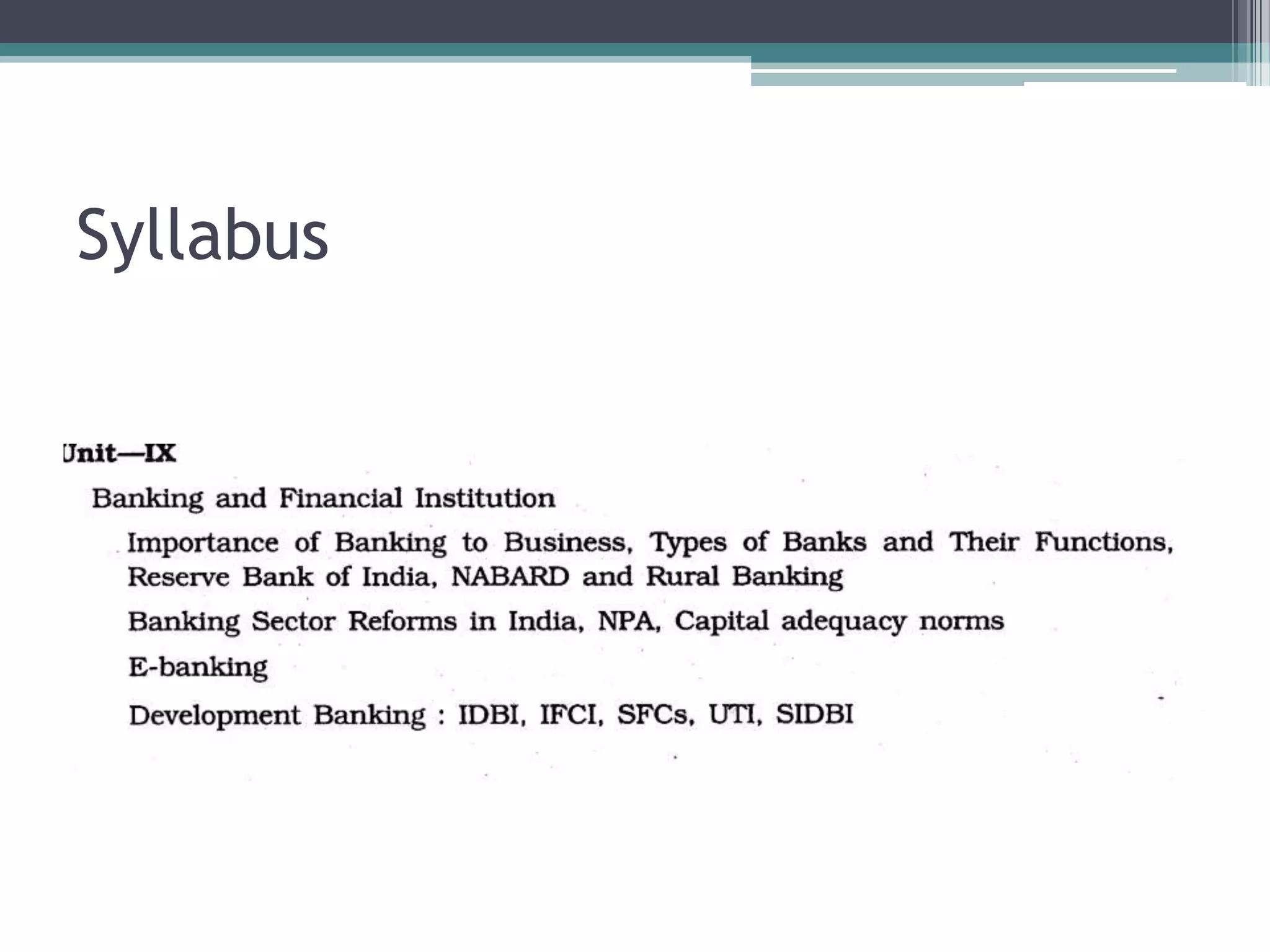

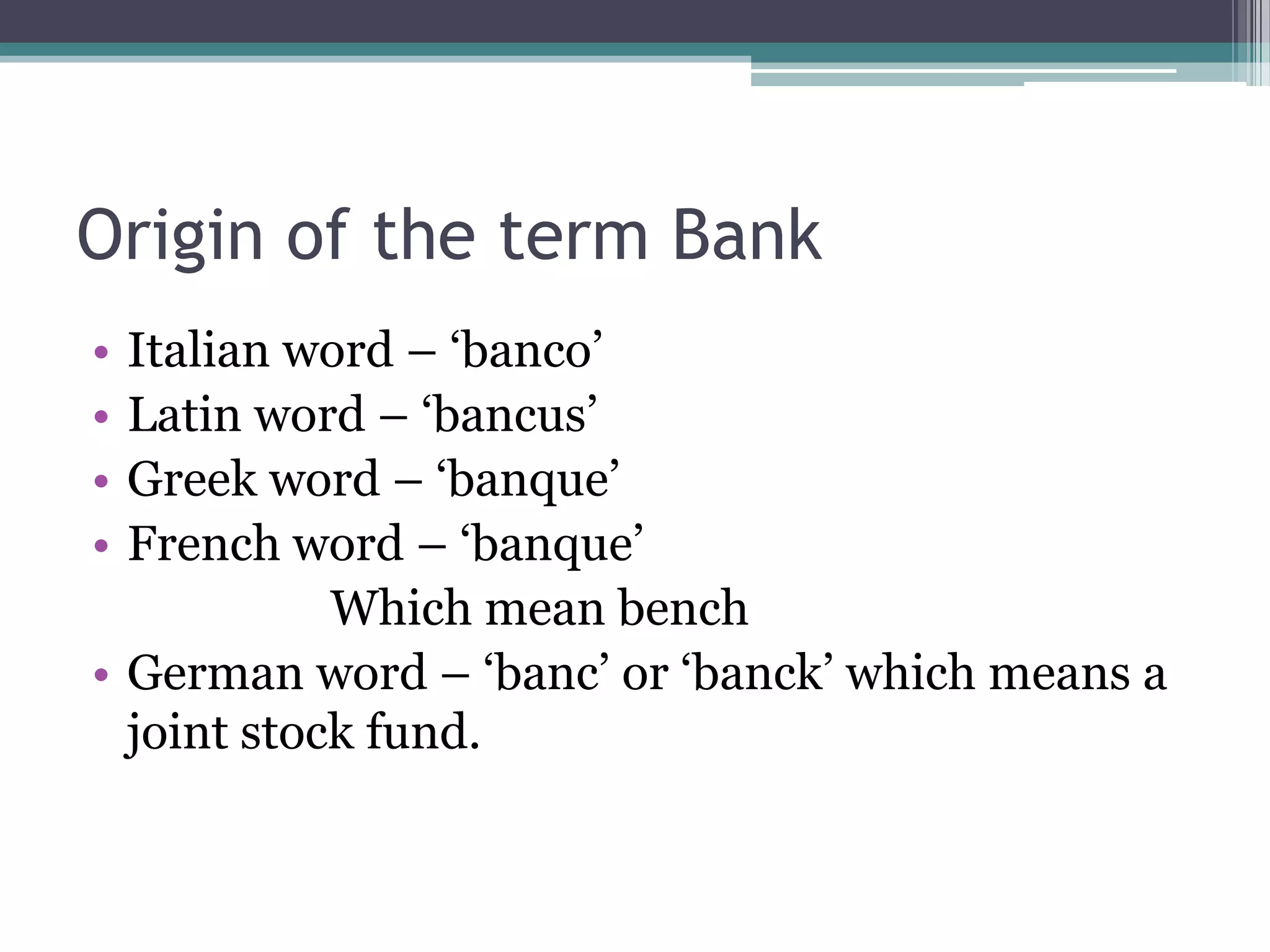

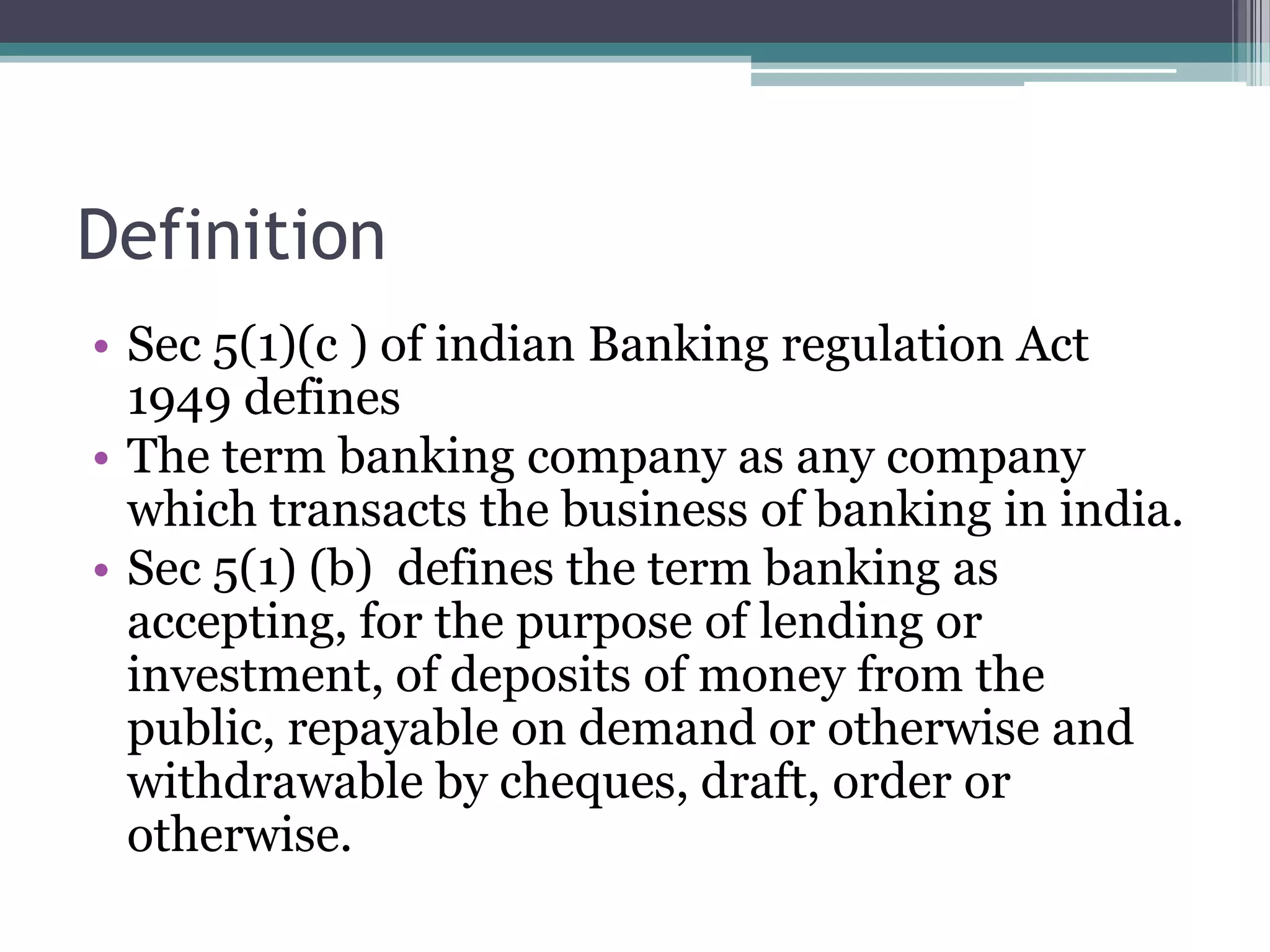

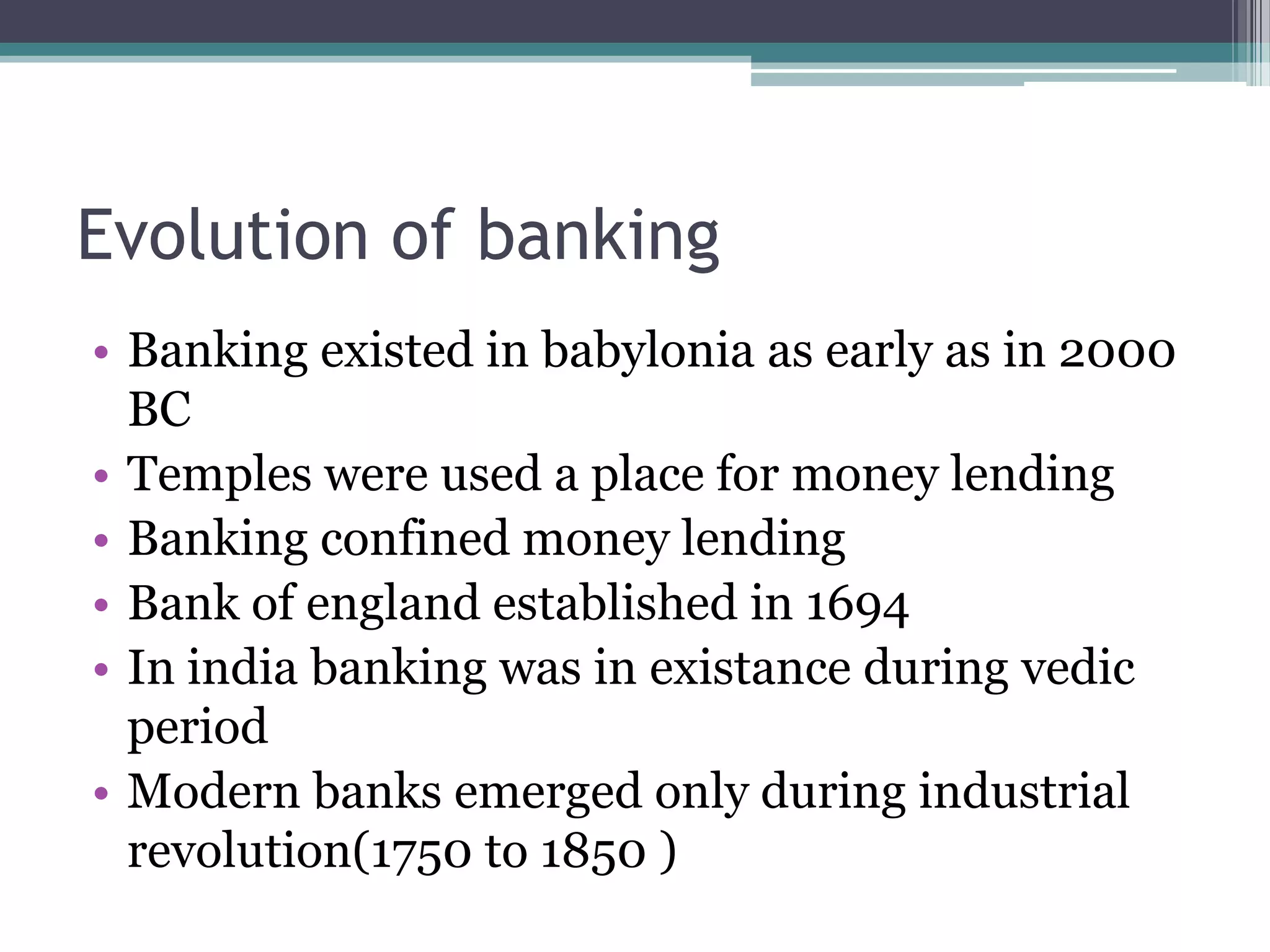

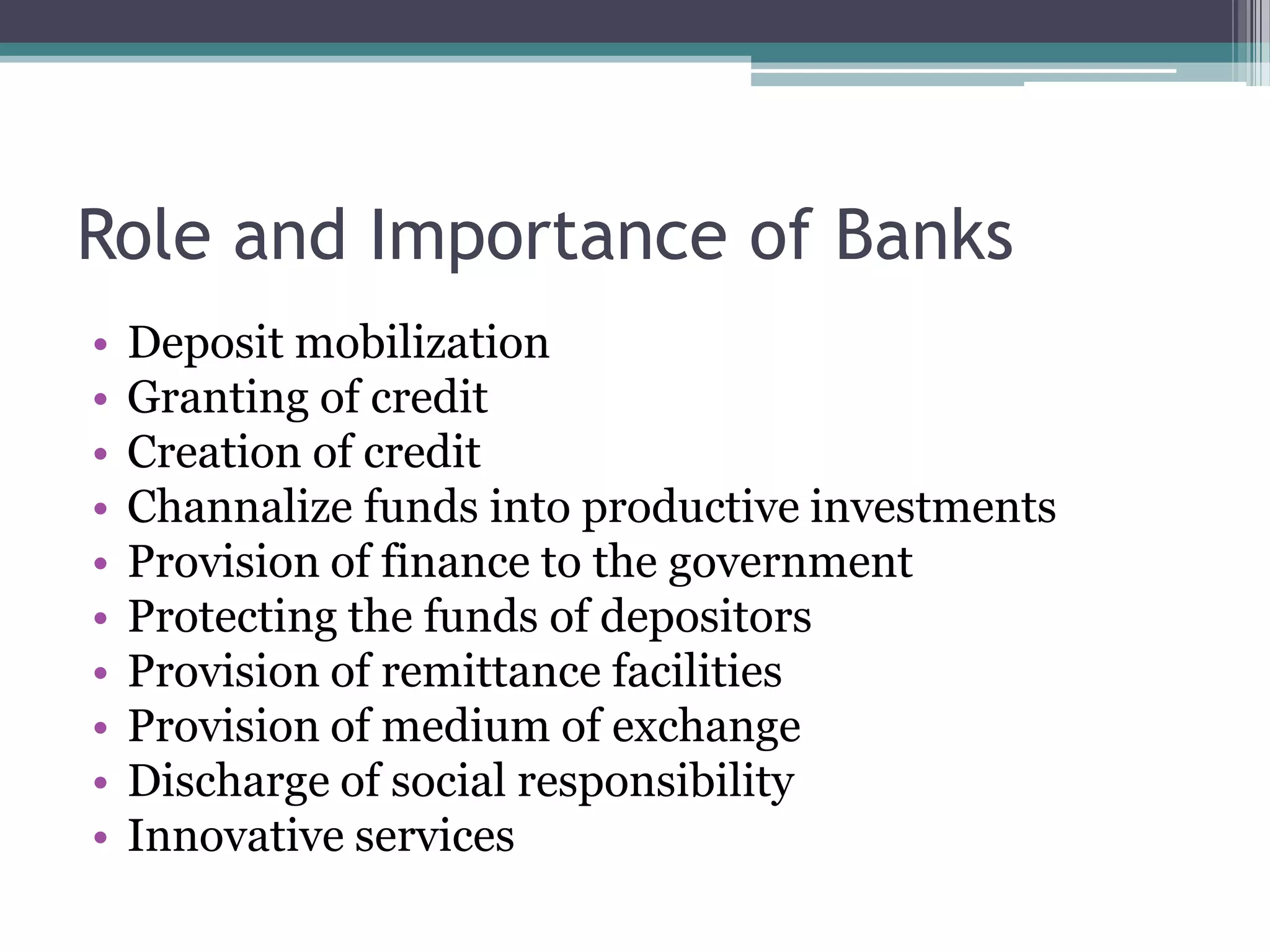

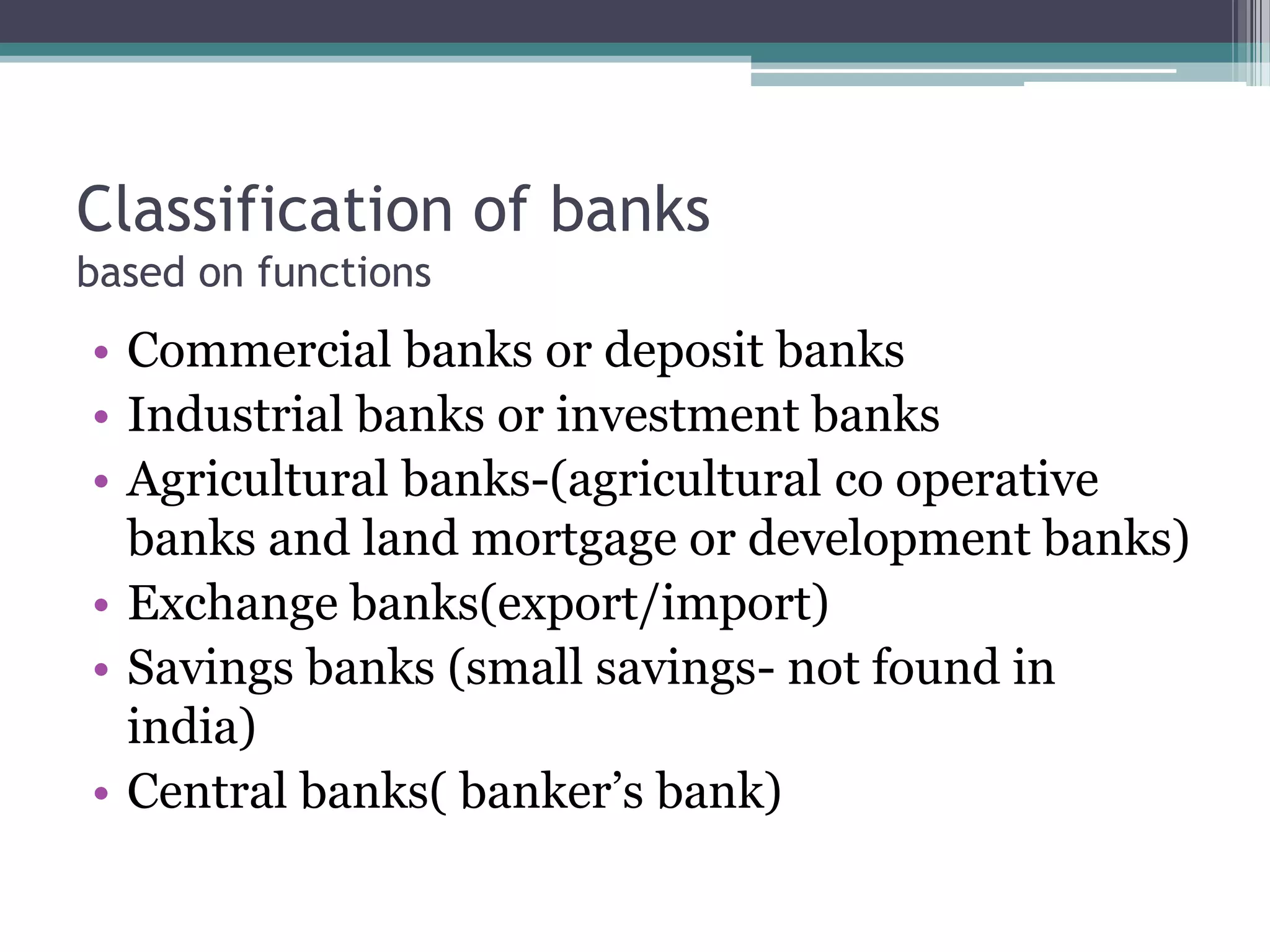

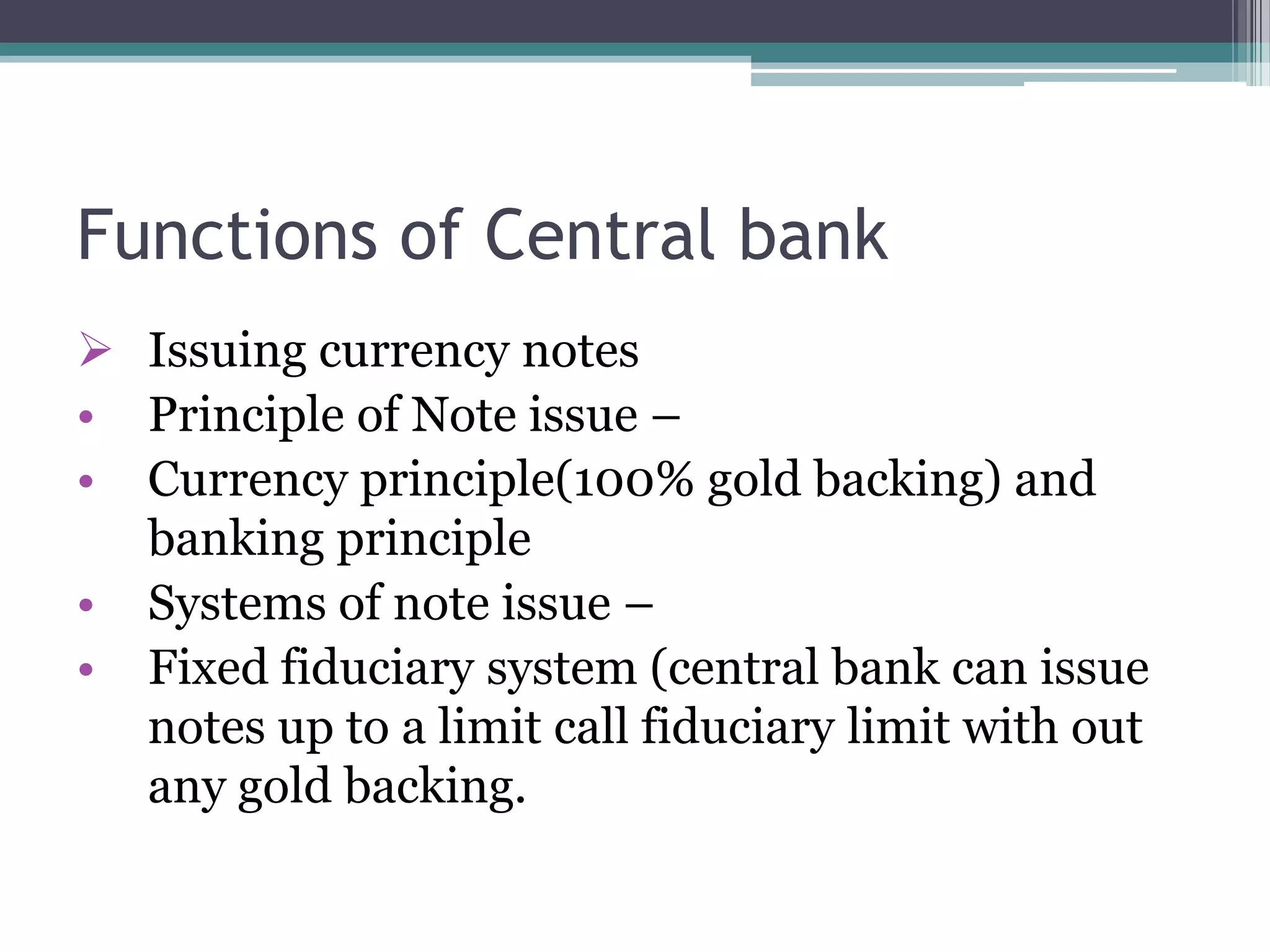

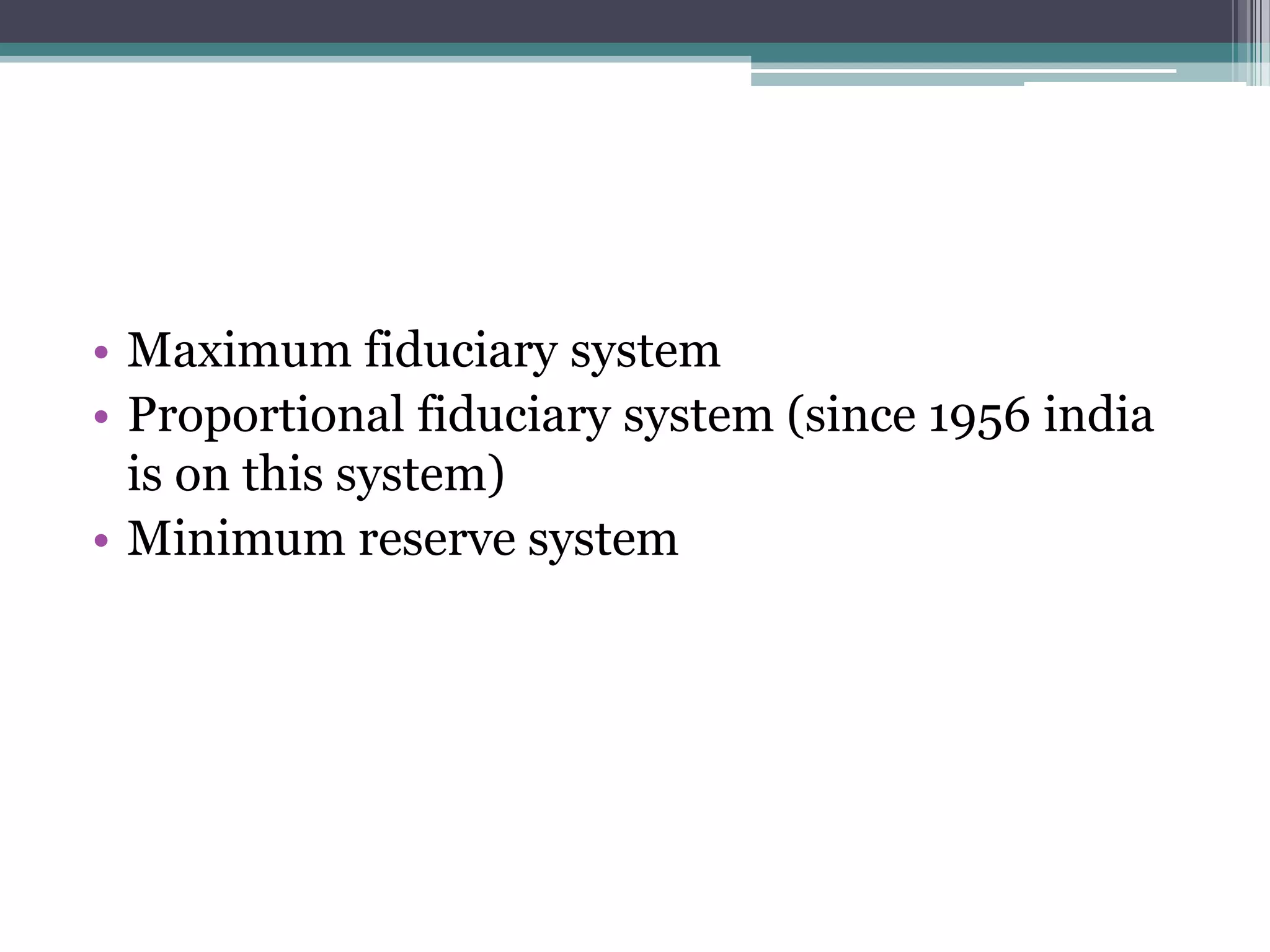

The document provides an overview of banking and financial institutions. It defines banking as accepting deposits from the public that are repayable on demand. Commercial banks engage in deposit taking and lending activities. Central banks act as bankers to commercial banks and engage in credit control to regulate money supply. Non-performing assets are loans that are overdue for over 90 days, impacting bank profitability. The Indian banking system has evolved from money lenders to include public and private sector banks.