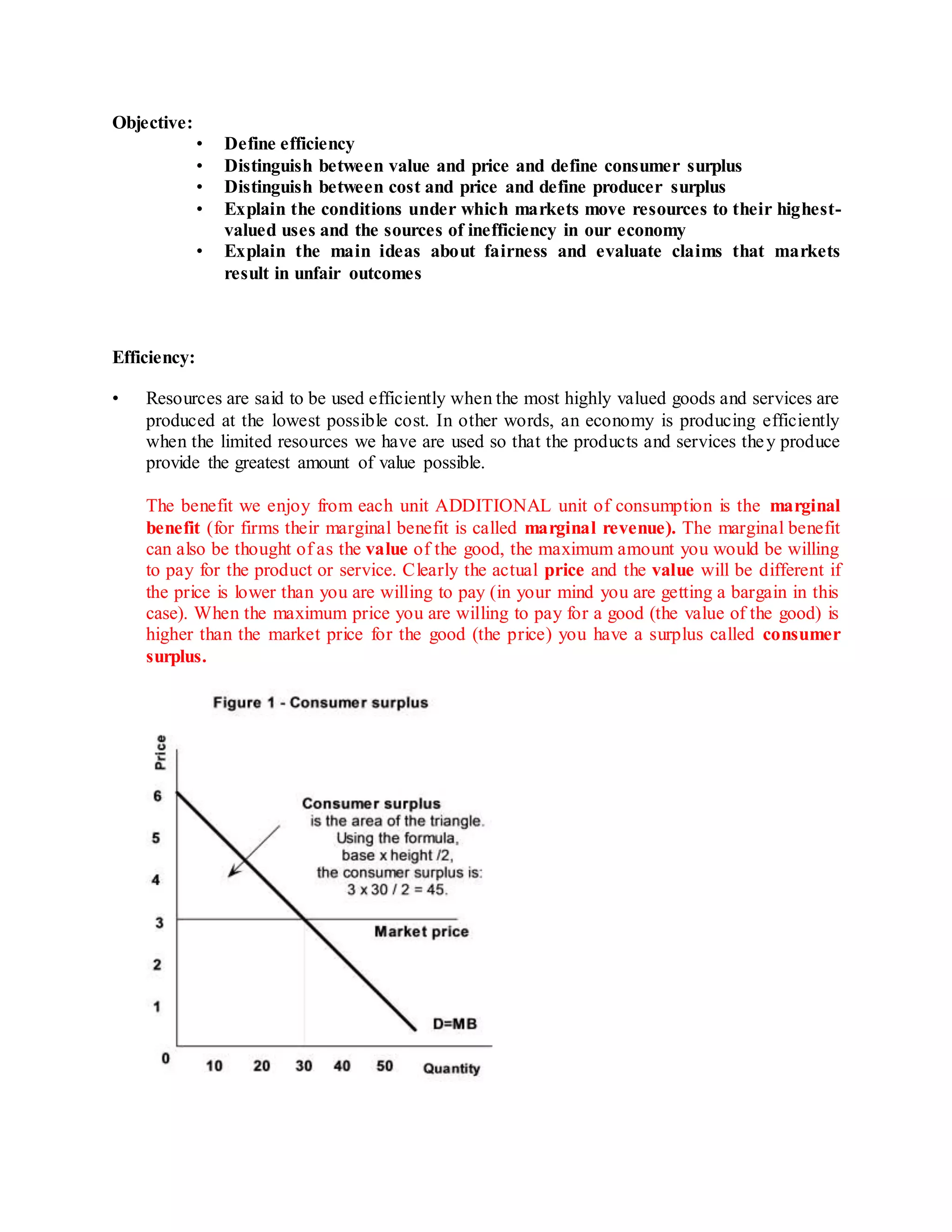

The document defines efficiency as producing goods and services at the lowest possible cost to provide the greatest value. Markets are efficient when marginal cost equals marginal benefit. When price is lower than value, consumers enjoy surplus, and when price exceeds costs, producers earn surplus. However, markets can be inefficient due to price controls, taxes/subsidies, monopoly, public goods, and externalities, resulting in deadweight loss to society.

![[Instrument] low level measurements handbook (keytley)](https://cdn.slidesharecdn.com/ss_thumbnails/instrumentlowlevelmeasurementshandbookkeytley-150105090213-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)