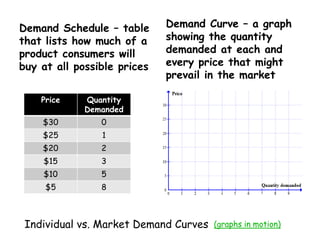

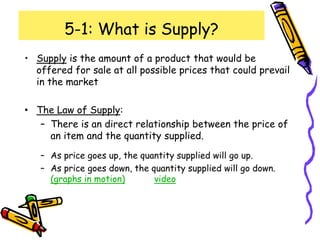

1) The document discusses microeconomic concepts of supply and demand, including the law of demand which states that as price increases, quantity demanded decreases, and vice versa.

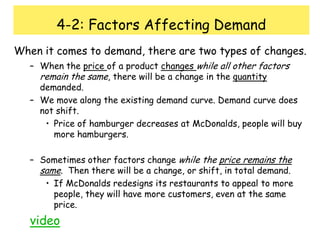

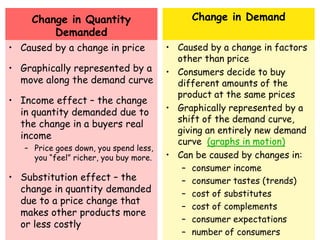

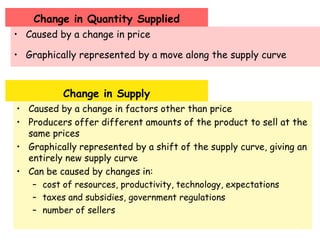

2) It examines factors that can cause changes in demand and supply, such as income, tastes, prices of substitutes/complements, and expectations.

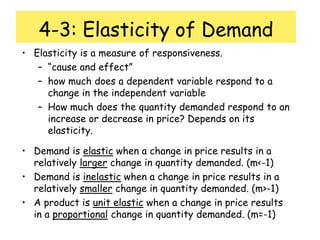

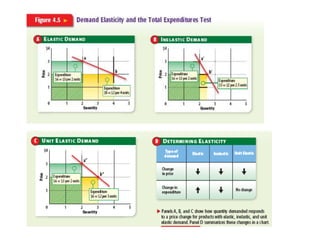

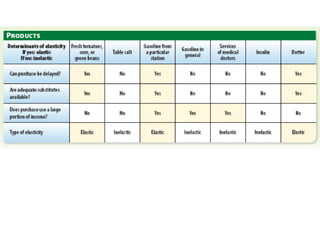

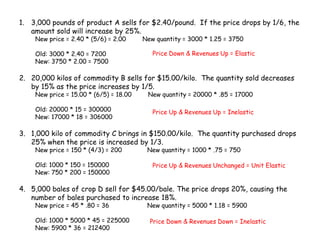

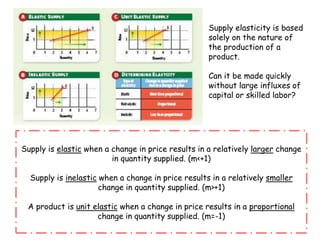

3) The concept of elasticity is introduced, measuring the responsiveness of quantity to price changes, and examples are provided to illustrate elastic versus inelastic demand.

![Lesson 7--supply[1]](https://cdn.slidesharecdn.com/ss_thumbnails/lesson-7-supply1-130409201835-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)