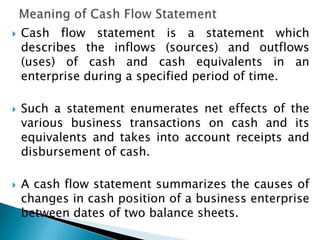

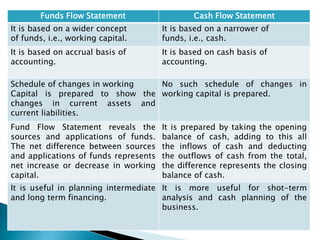

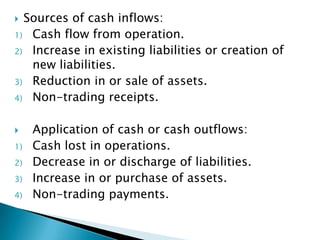

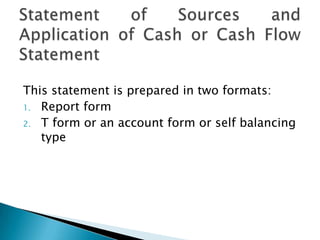

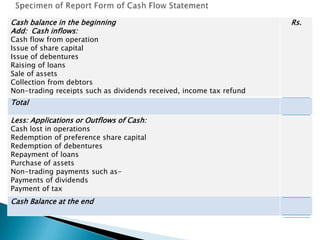

The cash flow statement describes sources and uses of cash over a period of time. It is based on cash accounting rather than accrual accounting. The statement summarizes changes in a business's cash position between two balance sheet dates by detailing cash inflows and outflows. Common sources include cash from operations, borrowing, and asset sales, while uses include cash lost in operations, loan repayments, asset purchases, and dividend payments. The statement is prepared in either report or T-account format.