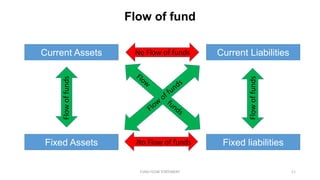

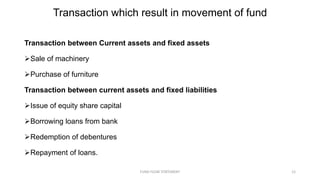

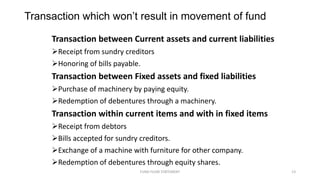

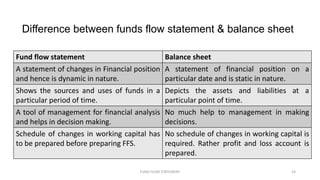

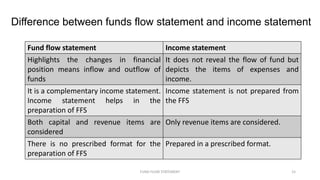

The document discusses the fundamentals of a funds flow statement. It defines a funds flow statement as a statement that shows changes in assets, liabilities, and owners' equity over a period of time. It explains the difference between narrow and broad concepts of funds, with the broad concept referring to working capital. The document also distinguishes between inflows and outflows of funds, and provides examples of transactions that do and do not result in the movement of funds. Finally, it compares funds flow statements to balance sheets and income statements.