The document discusses cash flow statements, which show the movement of cash between periods. It has three main sections:

1. It explains what cash flow statements are, their purpose of showing cash inflows and outflows from operating, investing and financing activities, and their advantages like ascertaining liquidity.

2. It covers the classification of cash flows into operating, investing and financing activities and provides examples of cash flows for each category.

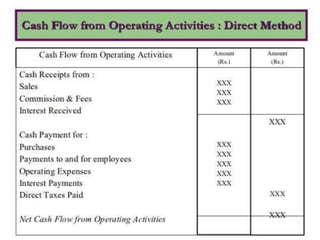

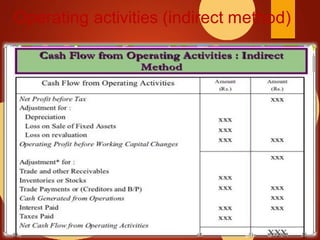

3. It describes the direct and indirect methods for showing cash flows from operating activities, noting non-cash items and other classifications are excluded under the direct method.