Download to read offline

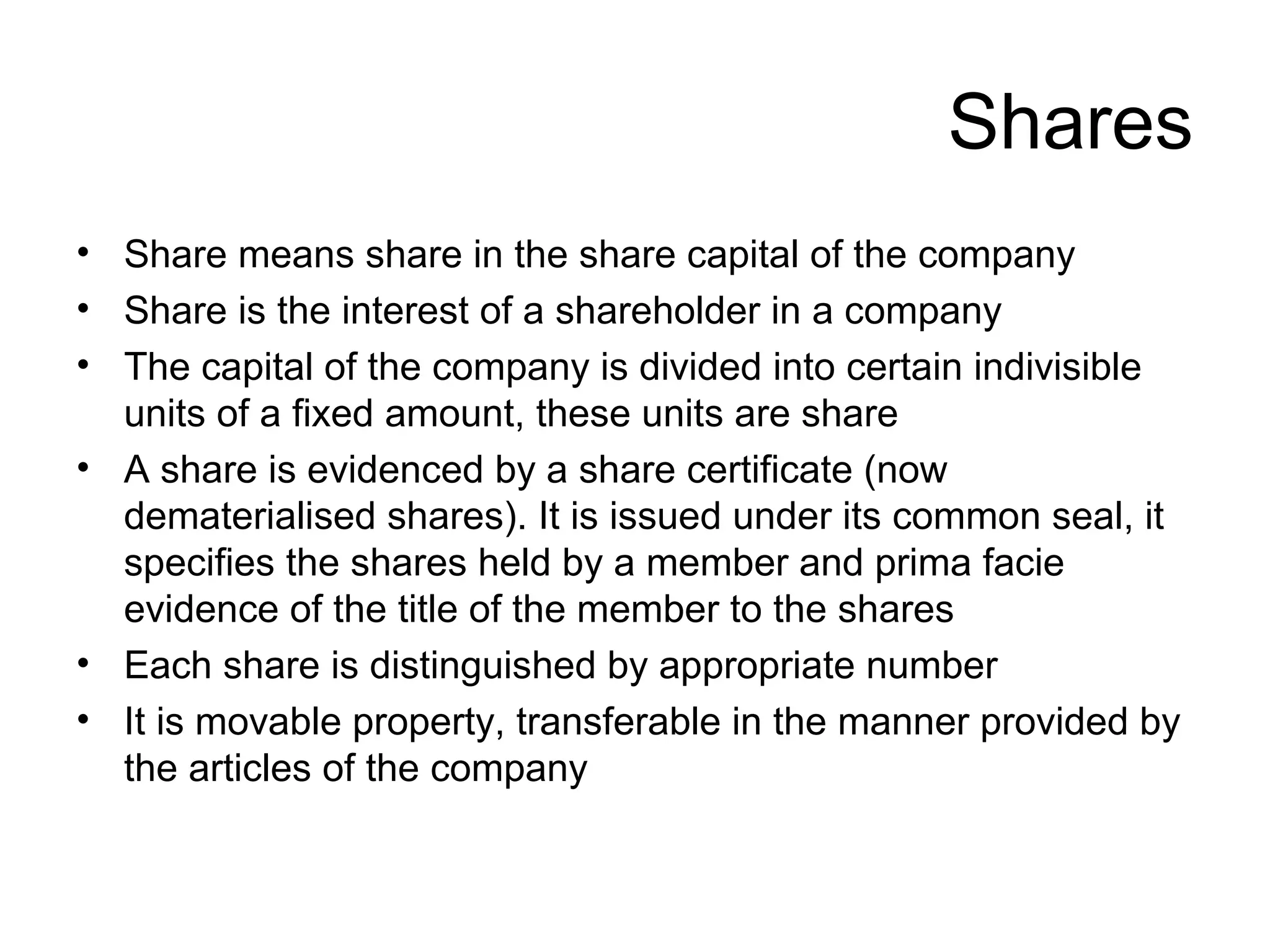

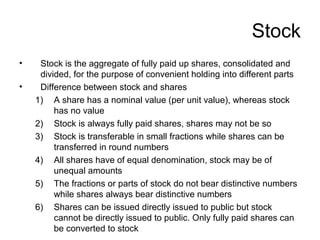

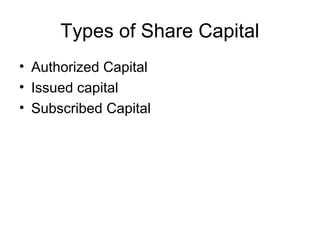

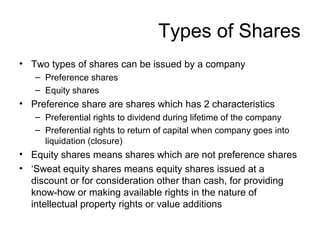

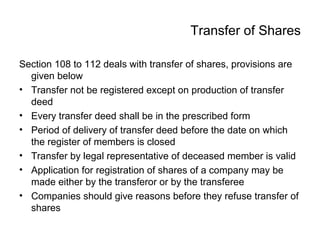

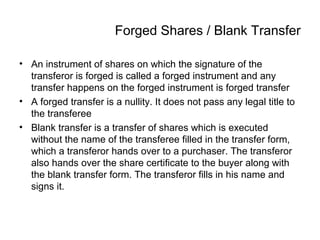

The document defines key terms related to shares and share capital in companies. It discusses what shares and stock are, the different types of share capital and shares, and provisions around application and allotment and transfer of shares. Specifically, it outlines the differences between shares and stock, types of preference and equity shares, minimum subscription requirements for allotment of shares, and requirements around forged and blank share transfers.

![Distribution channel &_physical_distribution.pptx [repaired]](https://cdn.slidesharecdn.com/ss_thumbnails/distributionchannelphysicaldistribution-150108150528-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)