Downloaded 32 times

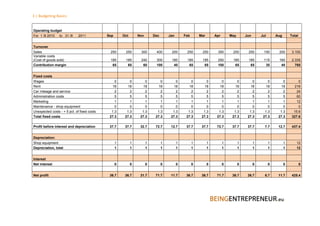

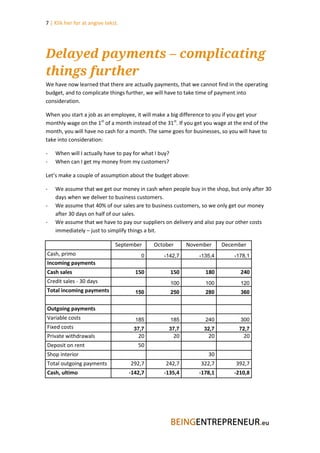

The document discusses cashflow budgets for startups. It provides an example of transforming an operating budget into a cashflow budget by transferring revenue and cost items to show monthly cash inflows and outflows. However, the cashflow budget must also account for additional payments like withdrawals, deposits, and large purchases not captured in the operating budget. Delayed customer payments and supplier payment terms further complicate the cashflow projections. The cashflow budget is necessary to determine if and when additional financing may be required beyond initial startup funding.