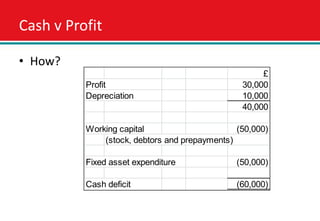

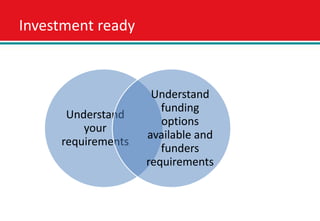

This document discusses the differences between profit and cash flow for businesses and the importance of adequate funding. It notes that while profit shows what is earned, cash flow shows actual payments and receipts, and there can be a gap between the two. The document advises businesses to understand their funding requirements through forecasts and look to match these with appropriate funding sources like debt, equity or grants. It also discusses being "investment ready" by having a strong business case and being compliant with legal requirements in order to attract financing.