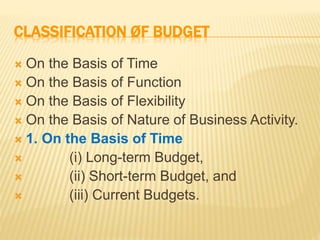

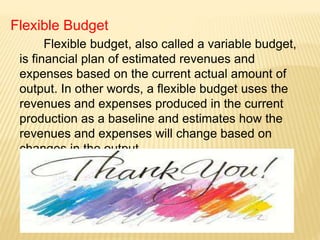

This document provides an overview of budgets and budgeting. It defines a budget as a financial plan for a defined period, often one year, that estimates revenues, expenses, assets, liabilities and cash flows. It then discusses the importance of budgeting and different ways to classify budgets, such as by time period, function, flexibility, and business activity. Specific budgets discussed include the master budget, cash budget, sales budget, purchases budget, materials budget, and flexible budget.