Learning Objectives:

At theend of this lesson, you should be able to:

1. Discuss budgeting;

2. Identify the benefits of budgeting; and

3. Explain the budgeting process

4.

The Concept ofBudgeting

● Budgeting is the process or act of preparing a

financial budget.

● Budget refers to a plan which is expressed in

quantitative monetary value (Philippine peso).

In other words, a budget is the final output of

the whole budgeting process.

5.

Benefits of Budgeting

Thebenefits that may be derived from

budgeting are as follows:

1. Planning is facilitated.

2. Financial coordination is established.

3. Resources are properly allocated.

4. Morale of employees improved.

5. Control mechanism is enhanced.

6.

Perspective of theBudgeting Process

In preparing a budget, the following questions

are addressed:

1. Who are involved in the budget

preparation?

2. What period is covered by the budget?

3. What type of budget is prepared?

7.

Persons Involved inthe Budget

Preparation

● Businesses create a budget committee to oversee the

preparation and administration of the budget. The budget

committee is represented by different functional areas of the

business.

● The four functional areas of the business (e.g.,

marketing, finance, production, and administration or

human resources) are involved in the preparation of the

budget.

8.

Period Covered bythe Budget

In terms of time element, the budget can either be:

a. Short-term budget – anchored on the targets and activities for

one-year operation

b. Medium-term or intermediate budget – sets budgetary

requirements of the busines for the next three or five years of

operations; anchored on the broad programs of each functional area

c. Long-term or strategic budget – the financial expression of the

vision-mission of the business; defines financial direction of the

business for the next five or ten years.

9.

Types of Budgetor Budgeting

a. Fixed budget – a budget based only on one level

of production capacity.

b. Flexible budget – a budget prepared showing the

projected cost at different levels of production

capacity.

c. Continuous rolling budget – a one-year budget

continuously prepared every month by adding

another month once the current month has passed.

10.

d. Cash budget– a budget that reflects the expected cash receipts from

cash sales, collections of accounts and notes receivable, sale of other

assets, proceeds of borrowings, and the expected cash disbursement

on payments of operating expenses, interest, taxes, and loans. The

cash budget should reflect the projected cash balance at the end of

every period covered.

e. Sales budget – a budget that reflects the expected number of units to

be sold based on forecast made from the performance of previous

years and other marketing variables.

f. Production budget – a budget that shows the cost of producing the

product. The cost of production includes direct materials, direct labor,

and factory overhead.

11.

g. Operating budget– a budget that reflects the sales

and production budgets.

h. Financial budget – a budget that usually includes

the cash budget and budgeted balance sheet.

i. Capital budget – a long-range budget that

incorporates the major expenditures for plant and

machineries.

j. Master budget – the overall budget of the business.

12.

Procedure in Budgeting

Thesteps in preparing the master budget are as

follows:

1. Prepare the sales budget

● The most important financial statement account in

forecasting is sales because almost all other

accounts in the financial statements are affected by

sales:

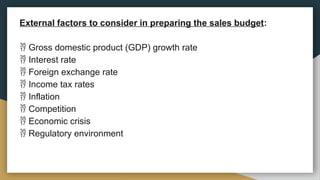

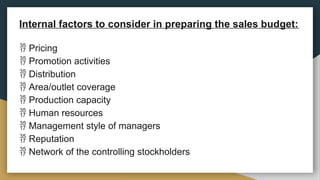

Internal factors toconsider in preparing the sales budget:

Pricing

Promotion activities

Distribution

Area/outlet coverage

Production capacity

Human resources

Management style of managers

Reputation

Network of the controlling stockholders

15.

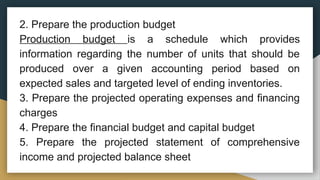

2. Prepare theproduction budget

Production budget is a schedule which provides

information regarding the number of units that should be

produced over a given accounting period based on

expected sales and targeted level of ending inventories.

3. Prepare the projected operating expenses and financing

charges

4. Prepare the financial budget and capital budget

5. Prepare the projected statement of comprehensive

income and projected balance sheet

16.

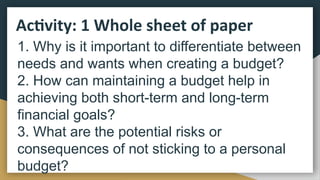

Activity: 1 Wholesheet of paper

1. Why is it important to differentiate between

needs and wants when creating a budget?

2. How can maintaining a budget help in

achieving both short-term and long-term

financial goals?

3. What are the potential risks or

consequences of not sticking to a personal

budget?