expected

learning

outcomes

After studying Chapter10,

you should be able to:

1. Understand the relationship between financial

planning and control.

3. Enumerate the types of budgets.

2. Know the nature, purposes and limitations of

the budget.

4. Understand and apply the steps in developing a

master budget.

3.

Financial planning involvesmaking projections of sales, income, and

assets based on alternative production and marketing strategies and

then deciding how to meet the forecasted financial requirements. In

the financial planning process, managers should also evaluate plans

and identify changes in operations that would improve results.

Financial control moves on to the implementation phase dealing

with the feedback and adjustment process that is required (a) to

ensure that plans are followed and, (b) to modify existing plans in

response to changes in the operating environment. The process

begins with the specification of the corporate goals, after which

management lays out a series of forecasts and budgets for every

significant area of the firm's activities, as shown in Figure 10-1.

FINANCIAL PLANNING AND CONTROL PROCESS

5.

FINANCIAL FORECASTING

AND BUDGETING

Financialforecasting starts with projecting sales revenues and

production costs. A budget outlines expected expenses for activities

and identifies funding sources. The production budget analyzes

investments in materials, labor, and facilities to meet forecasted sales.

This includes sub-budgets like the materials budget, personnel budget,

and facilities budget. The marketing team also prepares selling and

advertising budgets. Budgets are typically set monthly, comparing

actual results to projections and adjusting if needed.

During planning, these budgets are combined to create a cash budget,

anticipating cash flow needs. If increased sales forecast a cash shortage,

management arranges funding cost-effectively. After forecasting,

projected financial statements are developed and compared to actual

results, helping identify deviations, fix issues, and refine future projections.

Overall, this process helps management avoid cash shortages and boost

profitability.

6.

Budgeting is theact of preparing a budget.

A budget is a financial plan of the resources needed to carry

out tasks and meet financial goals. It is also a quantitative

expression of the goals the organizations wishes to achieve

and the cost of attaining these goals. The use of budgets to

control a firm's activities is known as budgetary control.

BUDGETING

Identify Income Calculate Expenses Set Priorities

7.

THE PURPOSE OFTHE BUDGET

A budget is a description in quantitative - usually monetary - terms of a desired future

result. The process of preparing the budget requires management at all levels to focus

on the future of the business entity. The benefits that may be realized from a budgeting

program are

1. Defining broad objectives and goals and formulating strategies to achieve such objectives;

2. Coordinating the activities of the organization by integrating the plans of the various parts thereby

pulling every one in the same direction;

3. Allocating resources to those parts of the organization where they can be used most effectively;

4. Communicating management's approved plans throughout the organization;

5. Uncovering and preparing for potential bottleneck in the operations before they occur;

6. Motivating managers to achieve the desired results, and

7. Setting a standard or benchmark for evaluating actual performance.

8.

ADVANTAGES AND LIMITATIONSOF BUDGETS

The advantages of budgeting include:

1. It forces planning and exposes situations in which plans of subcomponents are inadequate to

attain the total organization's objectives.

2. It allows a reiterative process to bring the goals of the organization and the subcomponents into

agreement.

3. It provides a means of communicating organization goals down through the organization and

sub-unit operational limitations up though the organization.

4. It provides a basis for financial planning, sub-unit coordination, resource acquisition, inventory

policy, scheduling and output distribution.

5. It provides a basis by which activity can be monitored, with actual results being compared to the

planned results.

9.

ADVANTAGES AND LIMITATIONSOF BUDGETS

The limitations of budgeting are:

1. Budgets tend to oversimplify the real situation and fail to allow for variations in external factors.

They do not reflect qualitative variables.

2. It is difficult to prepare a detailed budget for an organization that has never existed or for a new

division, product, or department of an existing firm.

3. There may be lack of higher and lower management commitment because of lack of

understanding of the fundamentals of budget preparation and utilization.

4. The budget is only a representation of future plans or a means to the goal of profitable activity and

not an end in itself. It may interfere with the supervisor's style of leadership and can therefore stifle

initiative.

5. Budget reports usually emphasize results, not reasons.

10.

TYPES OF BUDGETS

Thetypes of budgets or the major composition of

the master budget are:

1. The Operating Budget

2. The Financial Budget

3. The Capital Investment Budget

11.

A. Operating Budget

1.Budgeted Income Statement

a. Sales budget

b. Production budget

- Materials cost budget

- Direct labor cost budget

- Factory overhead budget

- Inventory levels

2. Cost of Sales budget

3. Selling and Administrative expenses budget

4. Financial expense budget

B. Financial Budget

1. Budgeted Statement of Financial Position

2. Cash budget

3. Budgeted Statement of Sources and Uses of Funds

C. Capital Investment Budget

The following is a simplified subclassification of the above-

mentioned types of budget for a manufacturing firm:

TYPES OF BUDGETS

12.

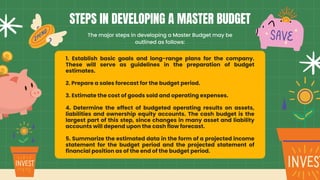

1. Establish basicgoals and long-range plans for the company.

These will serve as guidelines in the preparation of budget

estimates.

2. Prepare a sales forecast for the budget period.

3. Estimate the cost of goods sold and operating expenses.

4. Determine the effect of budgeted operating results on assets,

liabilities and ownership equity accounts. The cash budget is the

largest part of this step, since changes in many asset and liability

accounts will depend upon the cash flow forecast.

5. Summarize the estimated data in the form of a projected income

statement for the budget period and the projected statement of

financial position as of the end of the budget period.

The major steps in developing a Master Budget may be

outlined as follows:

STEPS IN DEVELOPING A MASTER BUDGET

14.

The sales budgetoutlines what products will be sold, in

what quantities, and at what prices. It serves as the

foundation for all other short-term budgets, triggering a

chain reaction in budget planning. It provides revenue

predictions, helps estimate cash receipts, and informs

budgets for production costs and selling & administrative

expenses. As the keystone of budgeting, its accuracy

directly impacts the entire financial plan.

SALES BUDGET

15.

The sales forecastis made after consideration of the

following factors.

1. Past sales volume

2. General economic and industry conditions

3. Relationship of sales to economic indicators

4. Relative product profitability

5. Market research studies and competition

6. Pricing, advertising and other promotion policies

7. Production capacity

8. Quality of sales force

9. Seasonal variations

10. Long-term sales trends for various products

17.

After the salesbudget has been set, a decision can be made

on the level of production that will be needed for the period to

support sales and the production budget can be set as well.

The production budget becomes a key factor in the

determination of other budgets, including the direct materials

budget, the direct labor budget and the manufacturing

overhead budget. These budgets in turn are needed to assist in

formulating a cash budget.

PRODUCTION BUDGET

18.

Using the datafrom the previously prepared sales

budget as well as the inventory summary information,

the following production budget is developed.

19.

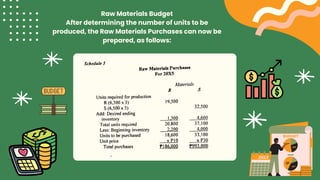

Raw Materials Budget

Afterdetermining the number of units to be

produced, the Raw Materials Purchases can now be

prepared, as follows:

20.

Direct Labor Budget

Thepreliminary data show that the budgeted direct labor cost per

unit produced is P146. This must have been arrived at after

considering such factors as skills level of the workers, labor rate per

hour, time requirement, conditions of union contracts, etc.

21.

Overhead Costs Budget

Studyof past records will show how the cost reacts to

changes in volume or in relation to other factors. Some

overhead items may be projected on the basis of about labor

hours or on materials costs or on machine hours.

24.

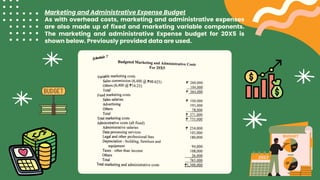

Marketing and AdministrativeExpense Budget

As with overhead costs, marketing and administrative expenses

are also made up of fixed and marketing variable components.

The marketing and administrative Expense budget for 20X5 is

shown below. Previously provided data are used.

25.

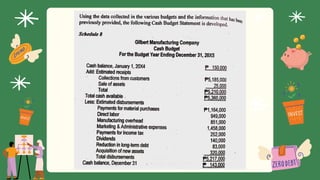

CASH BUDGET

CASH RECEIPTS

Normally,the bulk of a firm's cash receipts come from

customers. The possibility of cash from other sources

(such as additional investments, sales of assets,

borrowings) should likewise be considered when cash

receipts are being budgeted.

Cash Disbursements

Data converted from individual budgets previously illustrated

supply the basic information for the cash disbursements budget.

However, various adjustments and additions will have to be

made when preparing the budget for prepayments, accruals as

well extraneous items (such as the purchase of new equipment,

dividend payment) that do not show up in any of the individual

budgets already Prepared. If the financial policy of the company

requires that a minimum cash balance be maintained at all

times, the cash budget must be altered to accommodate bank

loans and their repayment.

27.

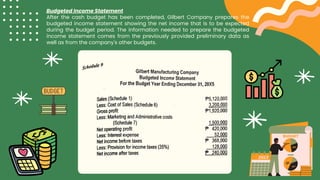

Budgeted Income Statement

Afterthe cash budget has been completed, Gilbert Company prepares the

budgeted income statement showing the net income that is to be expected

during the budget period. The information needed to prepare the budgeted

income statement comes from the previously provided preliminary data as

well as from the company's other budgets.

28.

Budgeted Statement ofFinancial Position

The budgeted statement of financial position is developed by beginning with

the current statement of financial position and adjusting it for the data

contained in the other budgets. Gilbert Company's budgeted statement of

financial position is presented below: