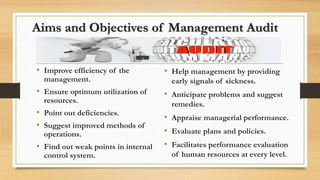

This document provides an overview of management audits. It defines a management audit as a systematic examination and appraisal of management's overall performance. The aims are to improve efficiency, ensure optimal resource use, identify deficiencies, and suggest improvements. Key differences from a cost audit are that management audits evaluate objectives/actions, require knowledge of management/production, and have no statutory obligations. The process involves identifying objectives, evaluating performance against objectives, and providing suggestions. The scope includes evaluating management efficiency, reviewing policy implementation, appraising performance, and recommending improvement areas. Advantages include aiding decisions and utilizing resources effectively. Disadvantages are the high cost for large organizations only. Operational aspects examined include objectives, production, sales,

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)