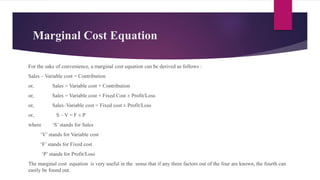

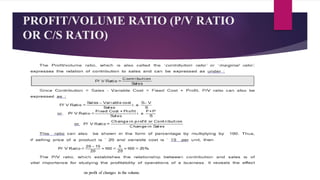

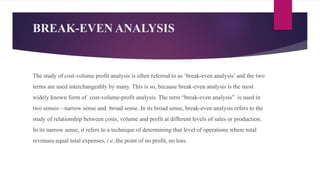

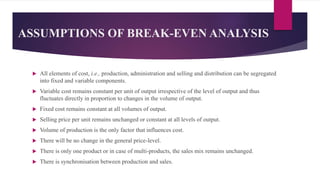

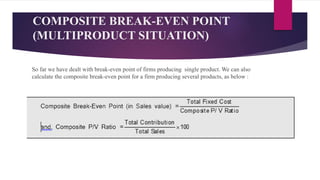

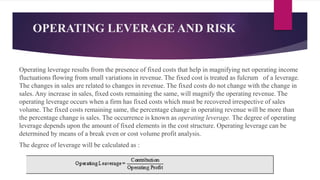

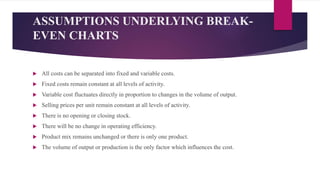

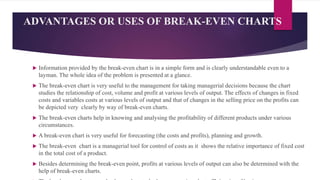

This document provides an overview of cost-volume-profit (CVP) analysis and break-even analysis. It defines CVP analysis as a technique for studying the relationship between cost, volume, and profit. The objectives of CVP analysis include determining the break-even point and maintaining a desired level of profit. Key assumptions of CVP analysis include segregating costs into fixed and variable components and constant selling prices. Techniques covered include contribution margin, the marginal cost equation, and profit-volume ratio. Break-even analysis determines the sales volume where total revenue equals total costs, representing no profit or loss. Formulas and assumptions for calculating the break-even point are also presented.