Download as PDF, PPTX

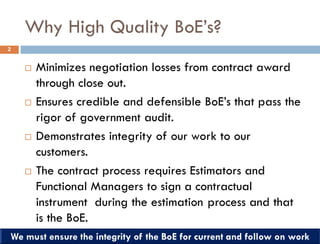

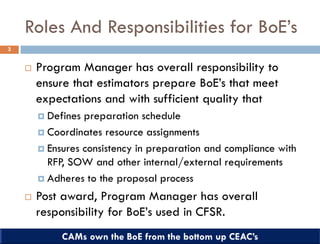

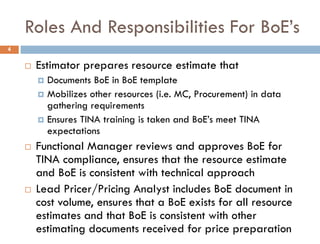

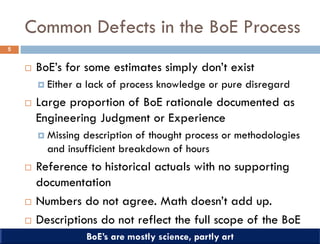

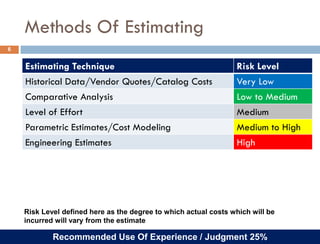

The document outlines the importance of high-quality Basis of Estimates (BOE) in minimizing negotiation losses, ensuring compliance, and demonstrating integrity in contract processes. It details the roles and responsibilities of key stakeholders in the BOE preparation, highlights common defects, and provides checklists for ensuring BOE completeness and accuracy. Additionally, it establishes criteria for auditing BOEs to maintain quality and support during customer submissions.