Downloaded 65 times

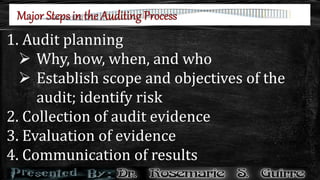

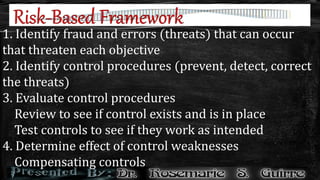

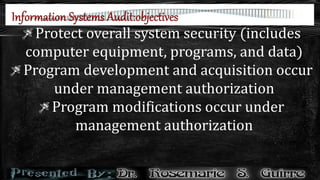

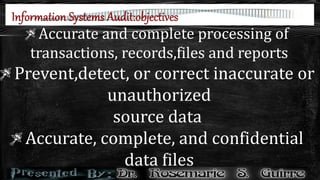

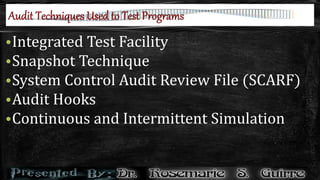

The document outlines the process of auditing an organization's information technology infrastructure, emphasizing the steps of audit planning, evidence collection, evaluation, and communication of results. It highlights the importance of identifying threats, implementing control procedures, and evaluating their effectiveness to protect system security. Additionally, it discusses various methods and tools used in audits, including automated software for operational audits that assess effectiveness and efficiency.