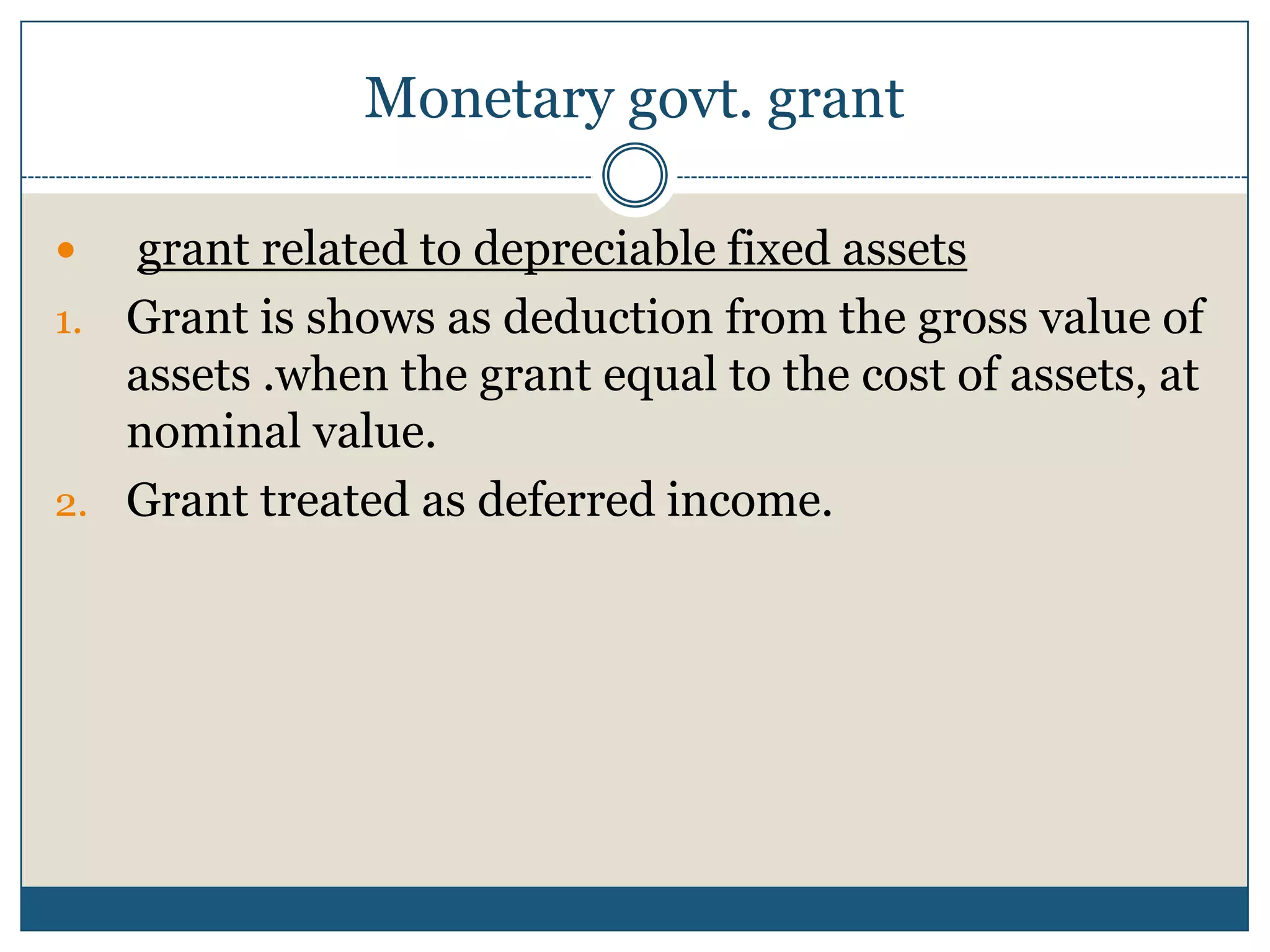

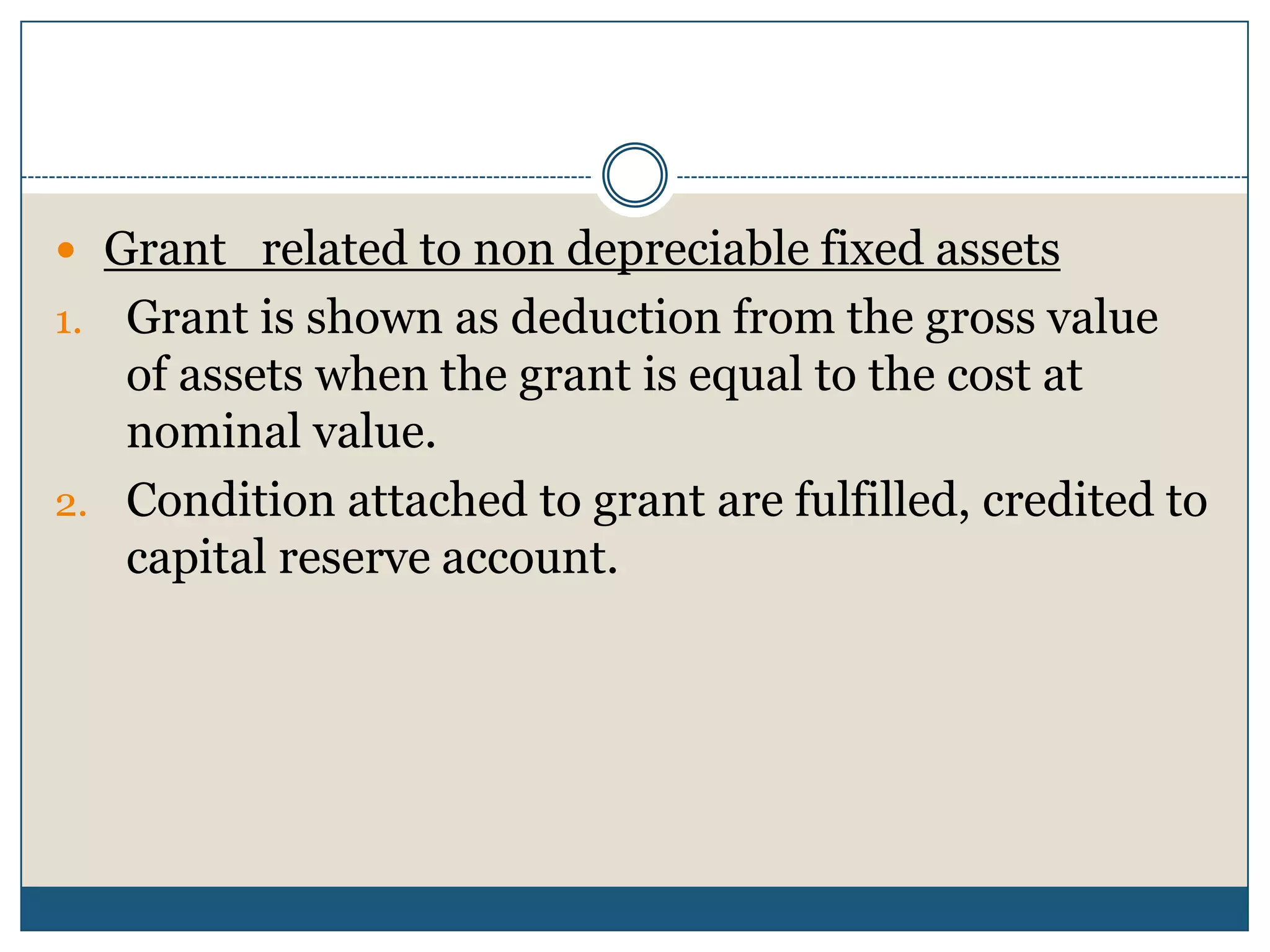

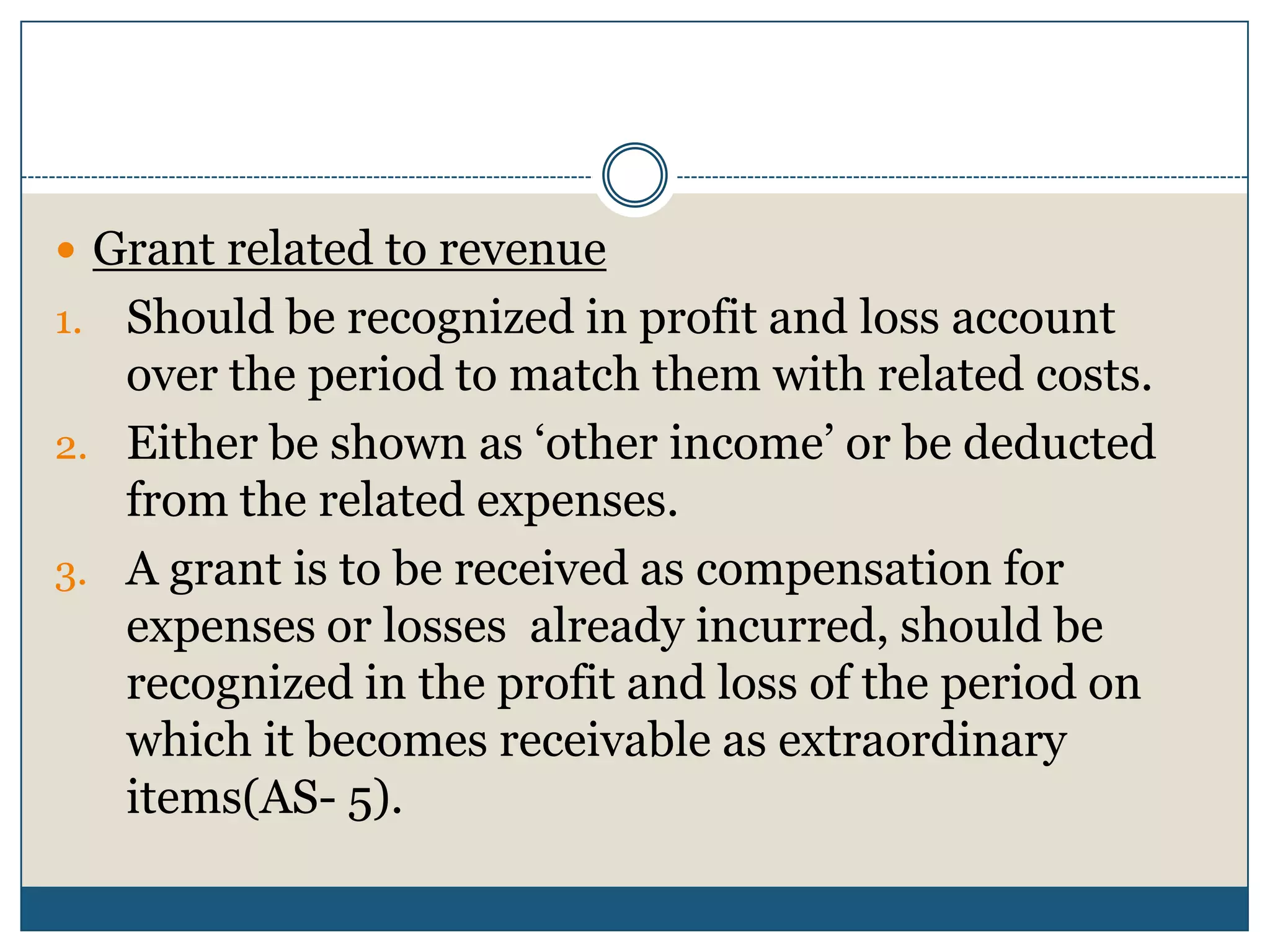

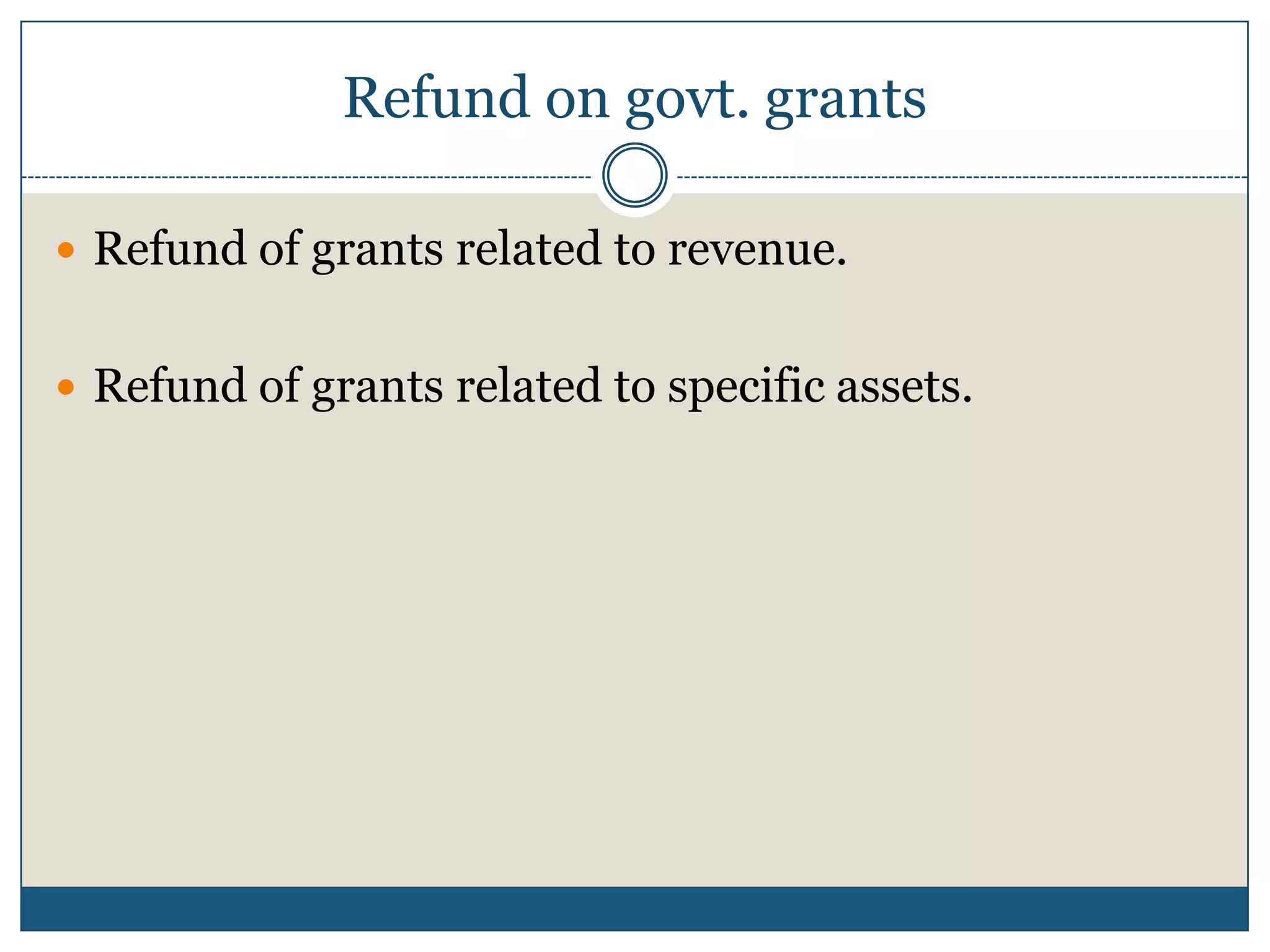

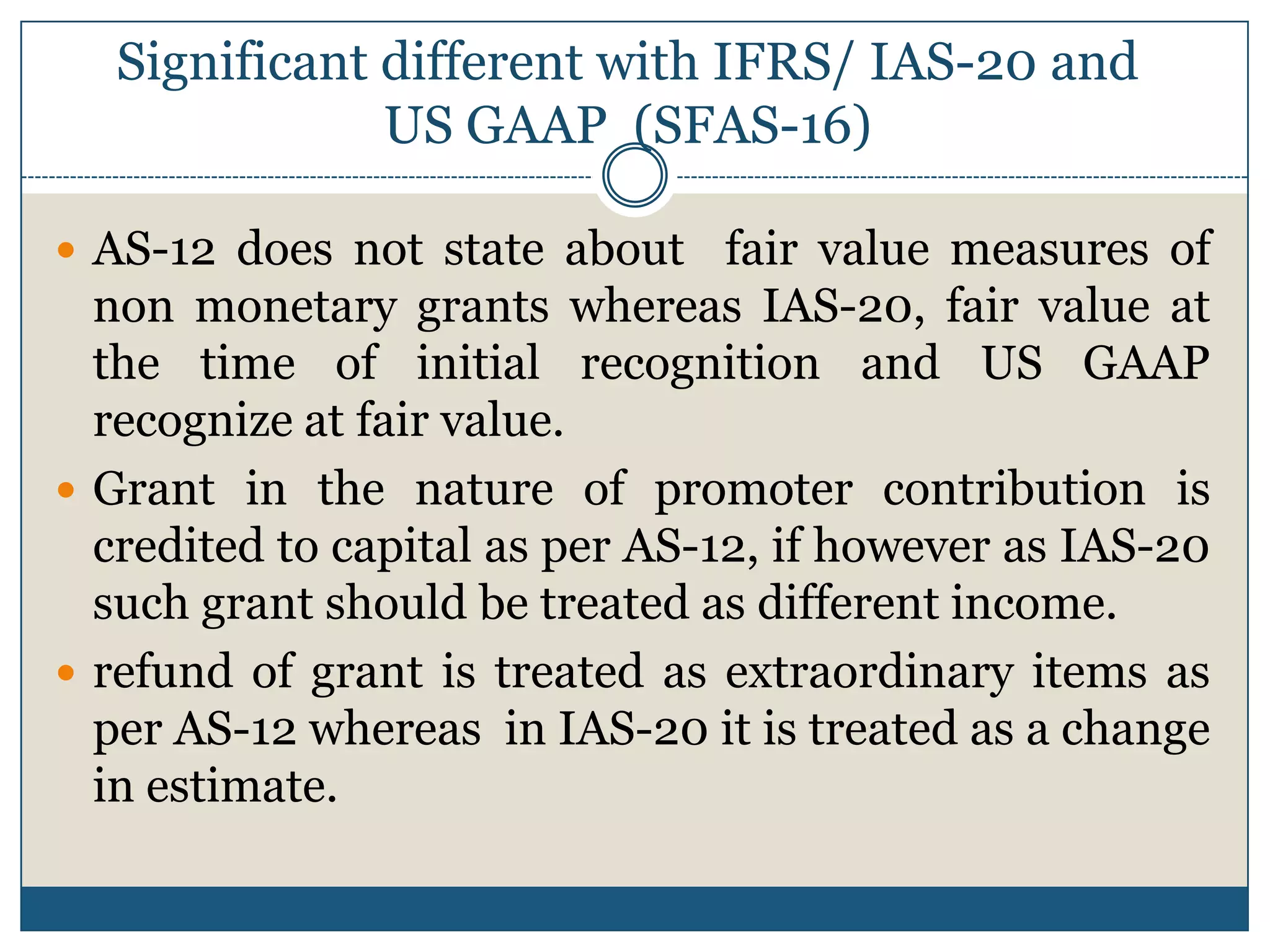

This document outlines accounting standards for government grants in India. It discusses the recognition and types of government grants, including monetary and non-monetary grants. It also addresses the treatment of monetary grants related to depreciable and non-depreciable fixed assets as well as grants related to revenue. The document concludes by discussing disclosure requirements and significant differences between this standard and IFRS/IAS-20 and US GAAP.