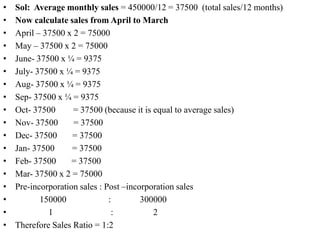

Downloaded 777 times

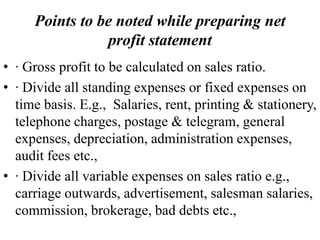

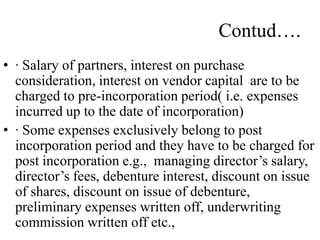

1) Profit earned before a company is incorporated is called pre-incorporation profit. It is considered capital profit and cannot be distributed as dividends. 2) To calculate pre-incorporation profit, expenses are divided between pre- and post-incorporation periods using time and sales ratios. Fixed expenses are divided by time ratio while variable expenses use sales ratio. 3) A net profit statement is prepared to analyze profit for the pre- and post-incorporation periods by allocating income and expenses accordingly.