This document provides an overview of Ind AS 38 on Intangible Assets. It discusses the objective and scope, key definitions, recognition and measurement criteria, disclosure requirements, and differences between Ind AS 38 and the previous Accounting Standard AS 26. Some of the key points covered include defining an intangible asset, the criteria for recognition of intangible assets, measurement at cost or revaluation model, amortization periods, impairment testing, and additional disclosures required under Ind AS 38.

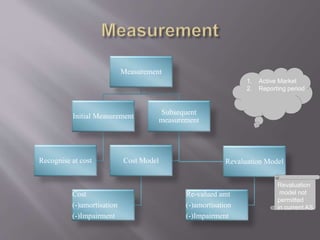

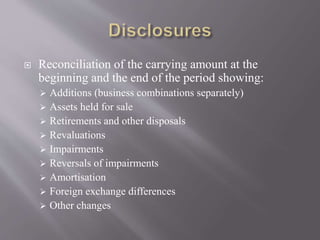

![ For each class of intangible asset, disclose: [IAS 38.118 and 38.122]

useful life or amortisation rate

Amortisation method

Gross carrying amount

Accumulated amortisation and impairment losses

Line items in the income statement in which amortisation is included

Basis for determining that an intangible has an indefinite life

Description and carrying amount of individually material intangible

assets

Certain special disclosures about intangible assets acquired by way of

government grants

Information about intangible assets whose title is restricted

Contractual commitments to acquire intangible assets](https://image.slidesharecdn.com/indas38-160313145702/85/Ind-as-38-27-320.jpg)

![Brennan, Niamh and Connell, Brenda [2000] Intellectual Capital: Current Issue...](https://cdn.slidesharecdn.com/ss_thumbnails/0410brennanconnellintellectualcapitalcurrentissuesandpolicyimplications-121116102513-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)