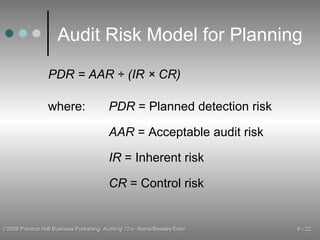

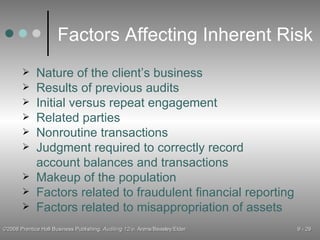

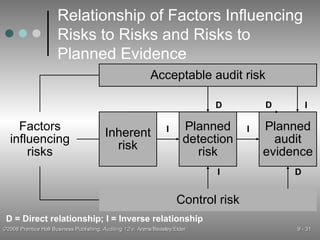

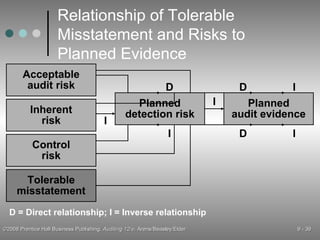

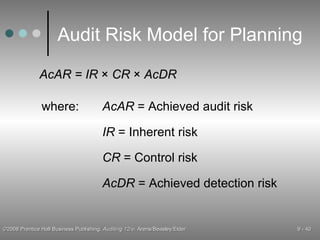

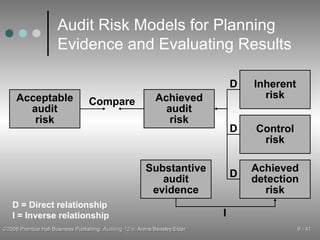

The document discusses the concepts of materiality and risk in auditing. It covers how materiality is used to determine the appropriate audit report and evaluate misstatements. The audit risk model components of inherent risk, control risk, and detection risk are explained along with how they impact evidence planning. Factors that influence the assessment of risks are also outlined.