Downloaded 53 times

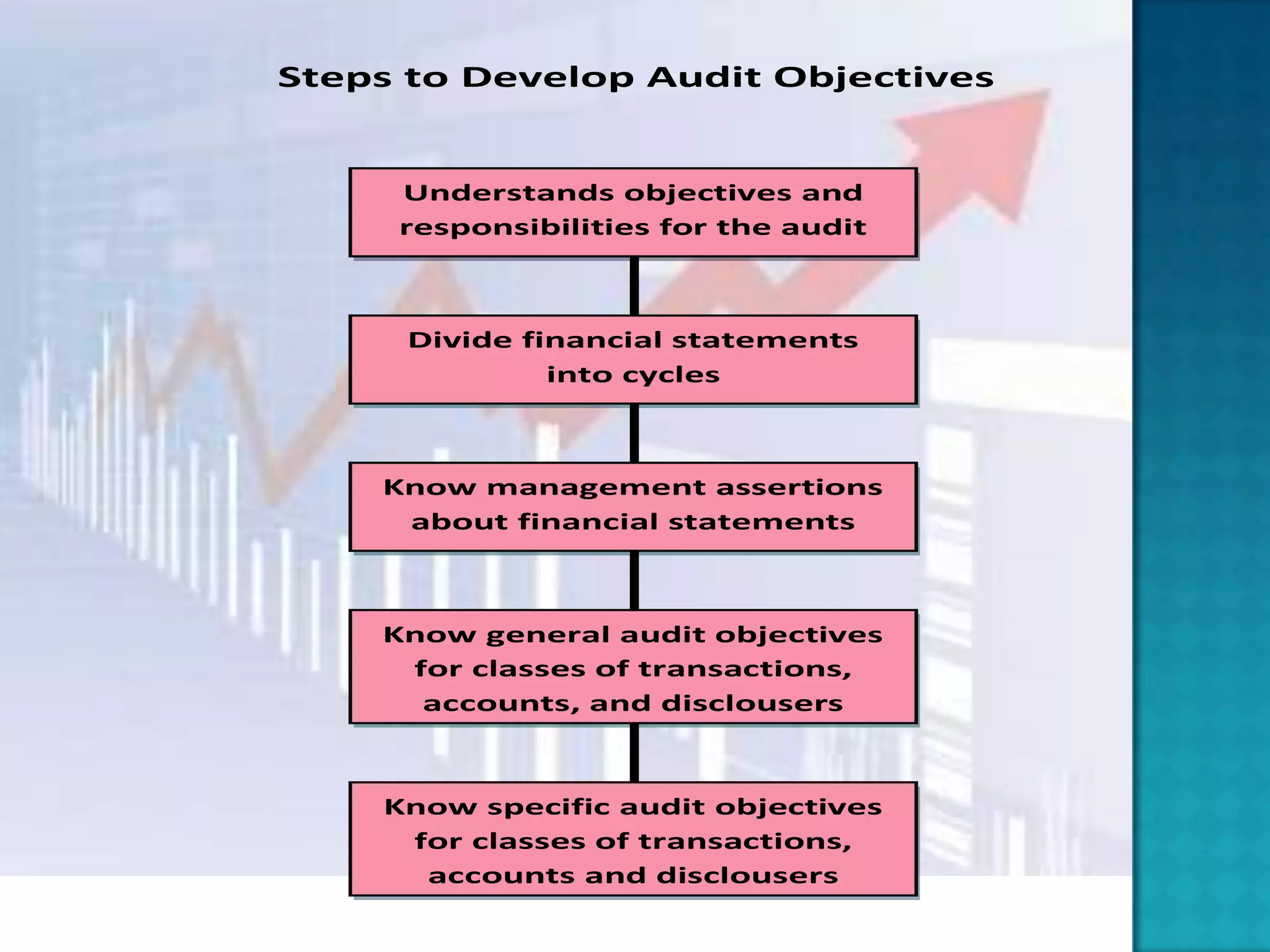

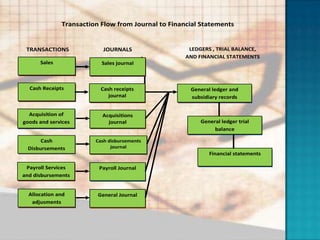

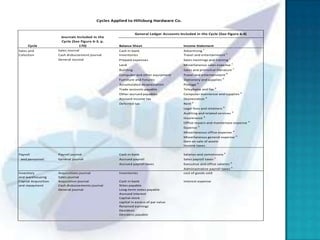

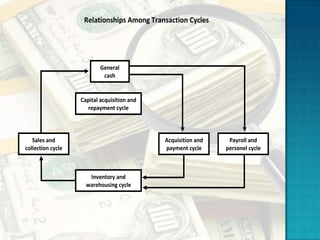

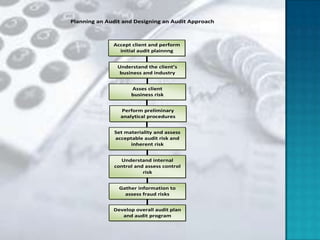

1. The document provides steps for developing audit objectives including understanding audit responsibilities and objectives, dividing financial statements into cycles, understanding management assertions and general/specific audit objectives. 2. It then provides examples of applying the audit cycle approach to a sample company, Hillsburg Hardware, outlining the general ledger accounts and journals included in each cycle. 3. Finally, it discusses key audit planning activities like understanding the client's business, assessing risks, developing the overall audit approach and audit program.

![Audit evidence a framework (ppt ch7[1].pdf)](https://cdn.slidesharecdn.com/ss_thumbnails/auditevidence-aframeworkpptch71-pdf-121211154609-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)