Modern Auditing:

Modern Auditing:

AssuranceServices and the Integrity

Assurance Services and the Integrity

of Financial Reporting, 8

of Financial Reporting, 8th

th

Edition

Edition

William C. Boynton

William C. Boynton

California Polytechnic State

California Polytechnic State

University at San Luis Obispo

University at San Luis Obispo

Raymond N. Johnson

Raymond N. Johnson

Portland State University

Portland State University

Chapter 3 – Client Acceptance and Planning the Audit

Evaluating the Integrityof

Evaluating the Integrity of

Management

Management

• Communicate with the Predecessor

Auditor

• Make Inquiries of Other Third

Parties

• Review Previous Experience with

Existing Clients

5.

Identifying Special Circumstances

IdentifyingSpecial Circumstances

and Unusual Risks

and Unusual Risks

• Identify Intended Users of Audited

Statements

• Assess Prospective Client’s Legal and

Financial Stability

• Identify Scope Limitations

• Evaluate the Entity’s Financial

Reporting Systems and Auditability

6.

Assessing Competence to

AssessingCompetence to

Perform the Audit

Perform the Audit

• Services Desired

• Identify the Audit Team

– Partner

– Manager(s)

– Senior(s)

– Staff Assistants

• Consider Need for Consultation and

Specialists

7.

Evaluating Independence

Evaluating Independence

•Identify Circumstances Impairing

Independence

• Identify Professional Staff Financial

and Business Relationships

• Identify Conflicts of Interest with

Other Clients

8.

Making the Decisionto Accept or

Making the Decision to Accept or

Decline the Audit

Decline the Audit

• Integrity of Management

• Special Circumstances and Unusual

Risks

• Competence Issues

• Independence Issues

9.

Preparing the EngagementLetter

Preparing the Engagement Letter

• Clear identification of entity and

financial statements to be audited

• Objective or purpose of the audit

• Reference to professional standards to be

followed

• Explain nature and scope of audit and

auditor’s responsibilities

10.

Preparing the EngagementLetter

Preparing the Engagement Letter

• Statement that not all material fraud

may be detected

• Reminder of management responsibility

for financial statements and internal

controls

• Indicate potential request for written

representations

• Describe any auxiliary services to be

provided

11.

Preparing the EngagementLetter

Preparing the Engagement Letter

• Basis on which fees will be computed and

billing arrangements

• Request to confirm terms of engagement

by signing and returning a copy to the

auditor

Study Break

Study Break

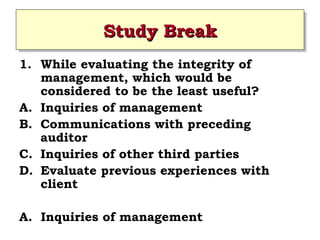

1.While evaluating the integrity of

management, which would be

considered to be the least useful?

A. Inquiries of management

B. Communications with preceding

auditor

C. Inquiries of other third parties

D. Evaluate previous experiences with

client

A. Inquiries of management

19.

Study Break

Study Break

2.Outside specialists include all of

the following except:

A. Appraisers

B. Internal auditors

C. Actuaries

D. Attorneys

B. Internal auditors

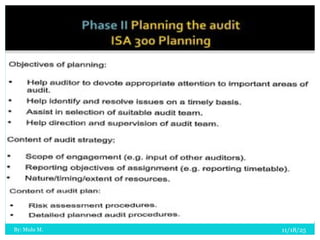

AUDIT PLANNING

• Auditplanning is a very important stage of the

audit because it helps direct the focus of the

audit. Within planning, risk is a key topic area

• A risk assessment carried out helps the

auditor to identify financial statement areas

susceptible to material misstatement and

provides a basis for designing and performing

further audit procedures

27

28.

• Audit riskis the risk that the auditor

expresses an inappropriate audit opinion

when the financial statements are materially

misstated.

• Audit planning sets the direction for the audit,

based on an assessment of the risks relevant

to the entity

28

29.

The importance ofplanning

1. Help the auditor Identify important areas

that require more attention

2. Identification of potential risks having effect

on audit as well as financial statements

3. Help the auditor identify and resolve

potential problems on a timely basis

4. Help the auditor properly organize and

manage the audit so it is performed in an

effective manner.

29

30.

5. Assist inthe selection of appropriate team

members and assignment of work to them.

6. Identification of the need for experts and co-

ordination of work of others

7. Facilitate the direction, supervision and

review of work.

30

31.

The overall auditstrategy and the

audit plan

• The audit strategy

• The overall audit strategy sets the scope, timing

and direction of the audit, and guides the

development of the more detailed audit plan.

• Examples of items to include in the overall audit

strategy could be:

1. Industry-specific financial reporting requirements

2. Number of locations to be visited

3. Audit client's timetable for reporting to its members

4. Communication between the audit team and the

client

32.

• The auditplan

• The audit plan converts the audit strategy into

a more detailed plan and includes the nature,

timing and extent of audit procedures to be

performed by engagement team members in

order to obtain sufficient appropriate audit

evidence to reduce audit risk to an acceptably

low level.

33.

• Examples ofitems included in the audit plan

could be:

1. Timetable of planned audit work

2. Allocation of work to audit team members

3. Audit procedures for each major account area

(eg inventory, receivables, cash etc)

4. Materiality for the financial statements as a

whole and performance materiality

• Any changes made during the audit

engagement to the overall audit strategy or

audit plan, and the reasons for such changes,

shall be included in the audit documentation.

• You must understand the difference between

the audit strategy and the audit plan.

34.

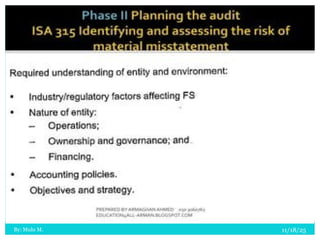

Introduction to risk

•A risk assessment carried out under the ISAs

helps the auditor to identify financial

statement areas susceptible to material

misstatement and provides a basis for

designing and performing further audit

procedures.

35.

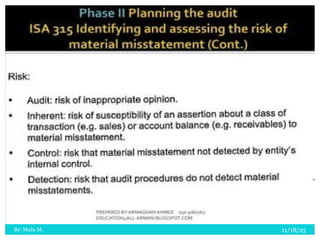

Overall Audit risk

•Audit risk is the risk that the auditor expresses

an inappropriate audit opinion when the

financial statements are materially misstated.

• It is a function of the risk of material

misstatement (inherent risk and control risk)

and the risk that the auditor will not detect

such misstatement (detection risk).

36.

• Audit riskhas two major components.

1.One is dependent on the entity, and is the risk of

material misstatement arising in the financial

statements (inherent risk and control risk).

2.The other is dependent on the auditor, and is the

risk that the auditor will not detect material

misstatements in the financial statements

(detection risk).

• Audit risk can be represented by the audit risk

model:

Audit risk =Inherent risk x control risk x detection risk

37.

1. Inherent risk

•Inherent risk is the risk that items will be misstated due

to the characteristics of those items, such as the fact

they are estimates or that they are important items in

the accounts.

• It is a risk that a misstatement could be material

individually or when aggregated with other

misstatements, assuming there were no related

internal controls.

• The auditors must use their professional judgment and

all available knowledge to assess inherent risk. If no

such information or knowledge is available then the

inherent risk is high.

• Inherent risk is affected by the nature of the entity; for

example, the industry it is in and the regulations it falls

under, and also the nature of the strategies it adopts.

38.

2. Control risk

•Control risk is the risk that a material

misstatement could occur that could be

material, individually or when aggregated

with other misstatements, that will not be

prevented or detected and corrected on a

timely basis by the entity's internal control.

39.

3. Detection risk

•Detection risk is the risk that the procedures

performed by the auditor to reduce audit risk to

an acceptably low level will not detect a

misstatement that exists and that could be

material, individually or when aggregated with

other misstatements.

• This is the component of audit risk that the

auditors have a degree of control over, because,

if risk is too high to be tolerated, the auditors

can carry out more work to reduce this aspect of

audit risk and, therefore, audit risk as a whole.

40.

• The followingprocedures therefore can help to

reduce detection risk:

– Adequate planning

– Assignment of more experienced personnel to the

engagement team

– The application of professional skepticism

– Increased supervision and review of the audit work

performed

• Auditors will want their overall audit risk to be at

an acceptable level, or it will not be worth them

carrying out the audit. In other words, if the

chance of them giving an inappropriate opinion

and being sued is high, it might be better not to

do the audit at all.

41.

• The auditorswill obviously consider how risky a

new audit client is during the acceptance process

and may decide not to go ahead with the

relationship.

• However, they will also consider audit risk for

each individual audit and will seek to manage the

risk.

• As we have seen above, it is not in the auditors'

power to affect inherent or control risk.

• These are risks integral to the client, and the

auditor cannot change the level of these risks.

• The auditors therefore manage overall audit risk

by manipulating detection risk, the only element

of audit risk they have control over.

42.

• It isimportant to understand that there is not

a standard level of audit risk which is generally

considered by auditors to be acceptable. This

is a matter of audit judgment and so will vary

from firm to firm and audit to audit.

• Audit firms are likely to charge higher fees for

higher risk clients.

• Regardless of the risk level of the audit,

however, it is vital that audit firms always

carry out an audit of sufficient quality.

43.

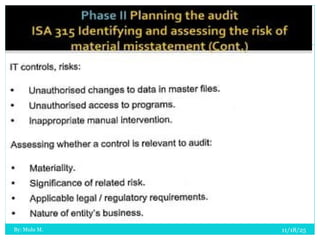

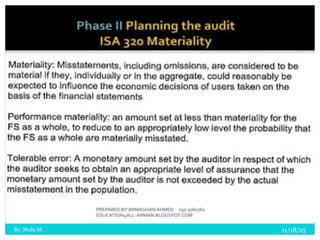

Materiality

• Materiality forthe financial statements as a

whole and performance materiality must be

calculated at the planning stages of all audits.

• The calculation or estimation of materiality

should be based on experience and judgment.

• Materiality for the financial statements as a

whole must be reviewed throughout the audit

and revised if necessary.

44.

• ISA 320Materiality in planning and

performing an audit provides guidance to

auditors in this area and states the objective

of the auditor is to apply the concept of

materiality appropriately in planning and

performing the audit

• ISA320 does not define materiality but the

following is generally used to explain

materiality:

45.

a) Misstatements areconsidered to be material if

they, individually or in aggregate, could

reasonably be expected to influence the

economic decisions of users.

b) Judgments about materiality are made in the

light of surrounding circumstances, and are

affected by the size and nature of a

misstatement or a combination of both.

c) Judgments about matters that are material to

users of financial statements are based on a

consideration of the common financial

information needs of users as a group.

46.

• The materialitylevel will impact on the

auditors decisions relating to:

–How many items to examine

–Which items to examine

–Whether to use sampling techniques

–What level of misstatement is likely to result

in a modified audit opinion

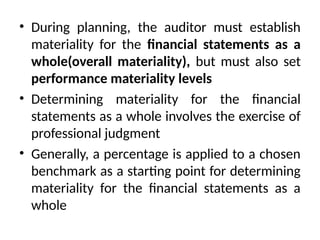

• During planning,the auditor must establish

materiality for the financial statements as a

whole(overall materiality), but must also set

performance materiality levels

• Determining materiality for the financial

statements as a whole involves the exercise of

professional judgment

• Generally, a percentage is applied to a chosen

benchmark as a starting point for determining

materiality for the financial statements as a

whole

49.

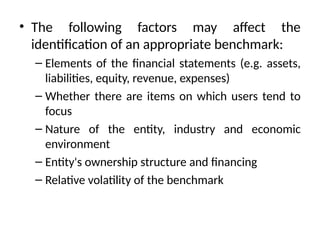

• The followingfactors may affect the

identification of an appropriate benchmark:

– Elements of the financial statements (e.g. assets,

liabilities, equity, revenue, expenses)

– Whether there are items on which users tend to

focus

– Nature of the entity, industry and economic

environment

– Entity's ownership structure and financing

– Relative volatility of the benchmark

50.

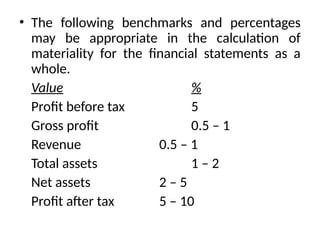

• The followingbenchmarks and percentages

may be appropriate in the calculation of

materiality for the financial statements as a

whole.

Value %

Profit before tax 5

Gross profit 0.5 – 1

Revenue 0.5 – 1

Total assets 1 – 2

Net assets 2 – 5

Profit after tax 5 – 10

51.

• Performance materialityis the amount or

amounts set by the auditor at less than

materiality for the financial statements as a

whole to reduce to an appropriately low level

the probability that the aggregate of

uncorrected and undetected misstatements

exceeds materiality for the financial

statements as a whole.

• Performance materiality is what is applied

during the testing