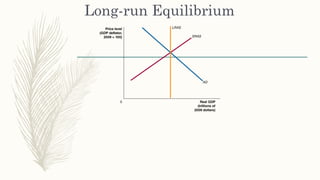

1. The document provides an overview of aggregate demand, aggregate supply, and how they interact in the short-run and long-run.

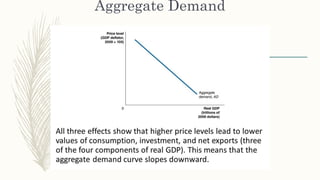

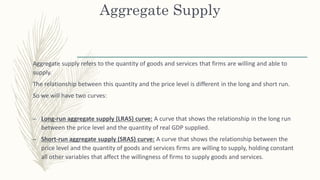

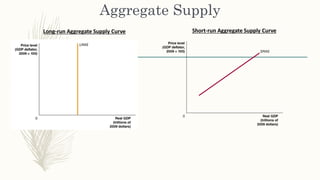

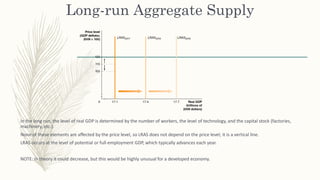

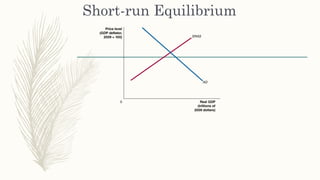

2. It defines aggregate demand as determined by GDP components (C, I, G, NX) which are influenced by prices. Aggregate supply is defined as the quantity of goods firms are willing to supply, shown on long-run and short-run curves.

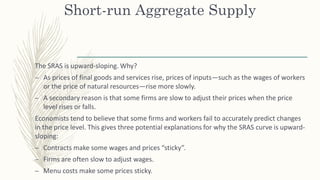

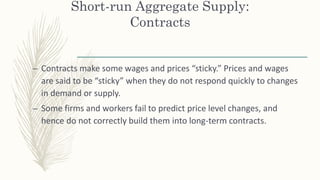

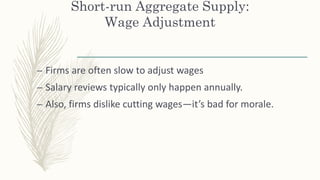

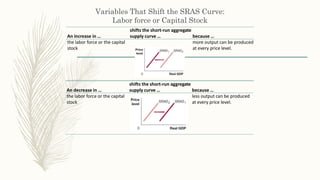

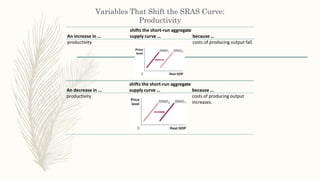

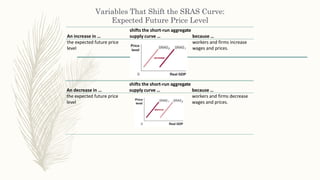

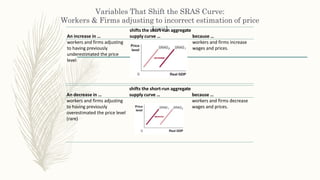

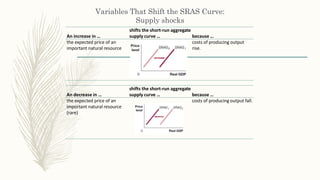

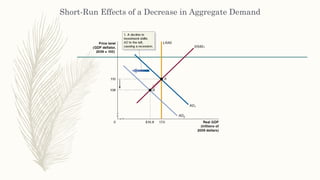

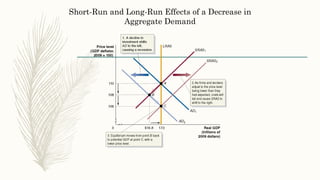

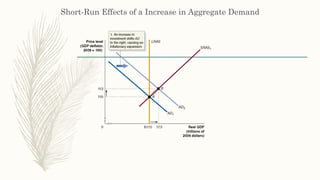

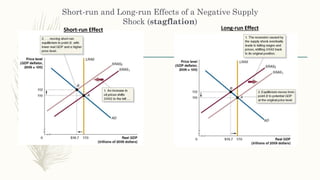

3. The short-run aggregate supply curve slopes up due to price stickiness from contracts, slow wage adjustments, and menu costs. Shifts can occur from changes to inputs, productivity, or supply shocks.