Download as PPS, PPTX

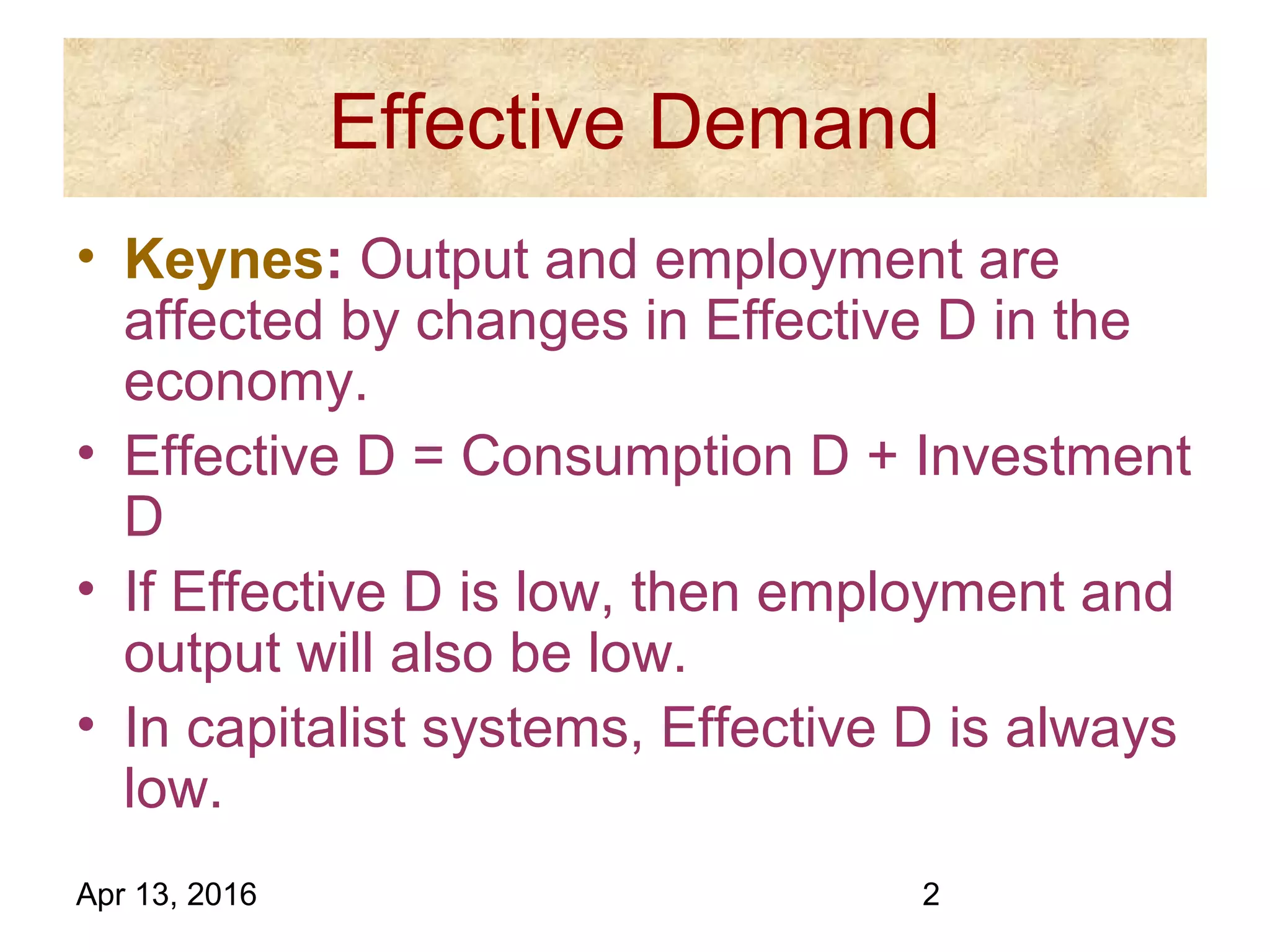

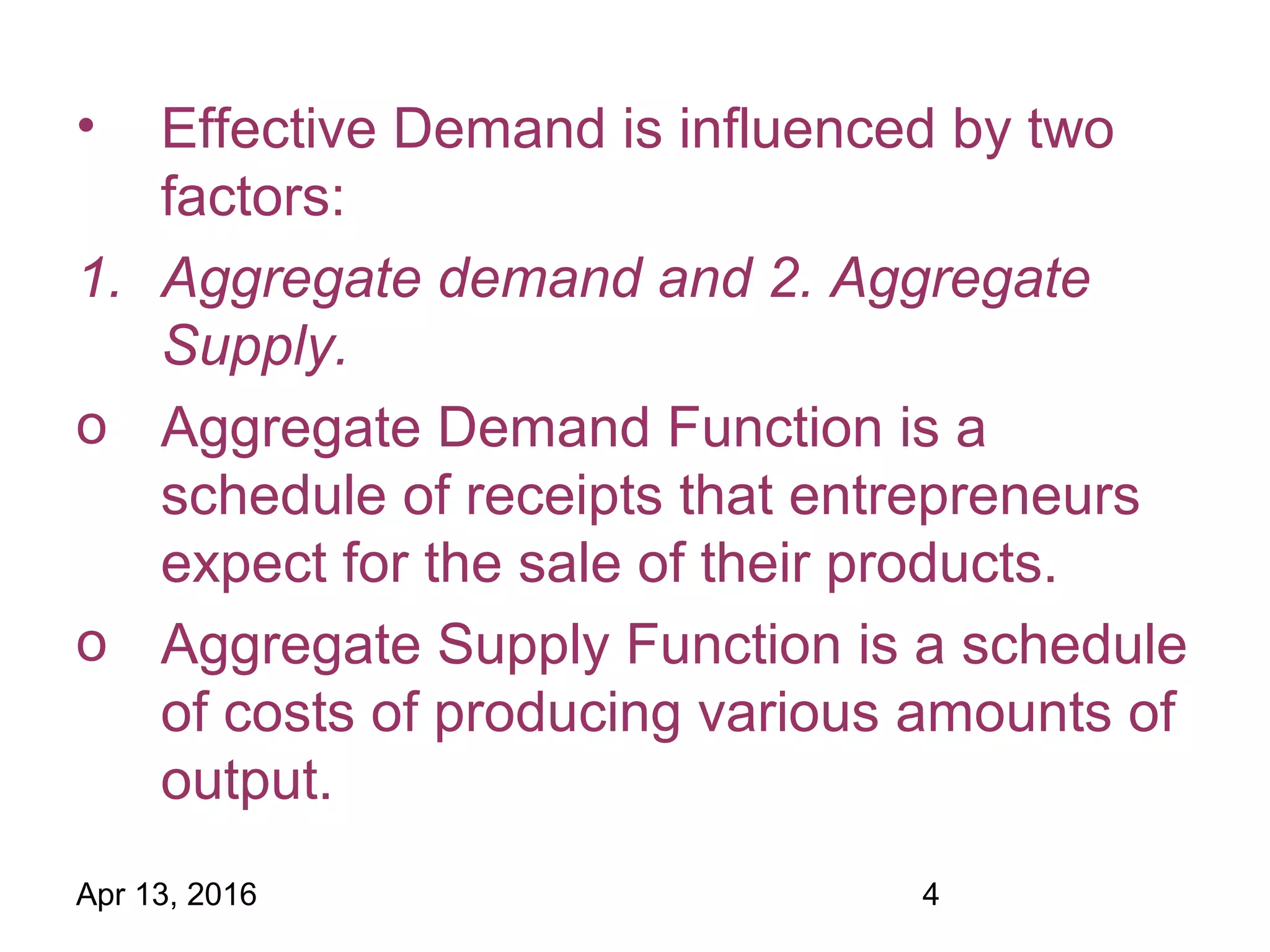

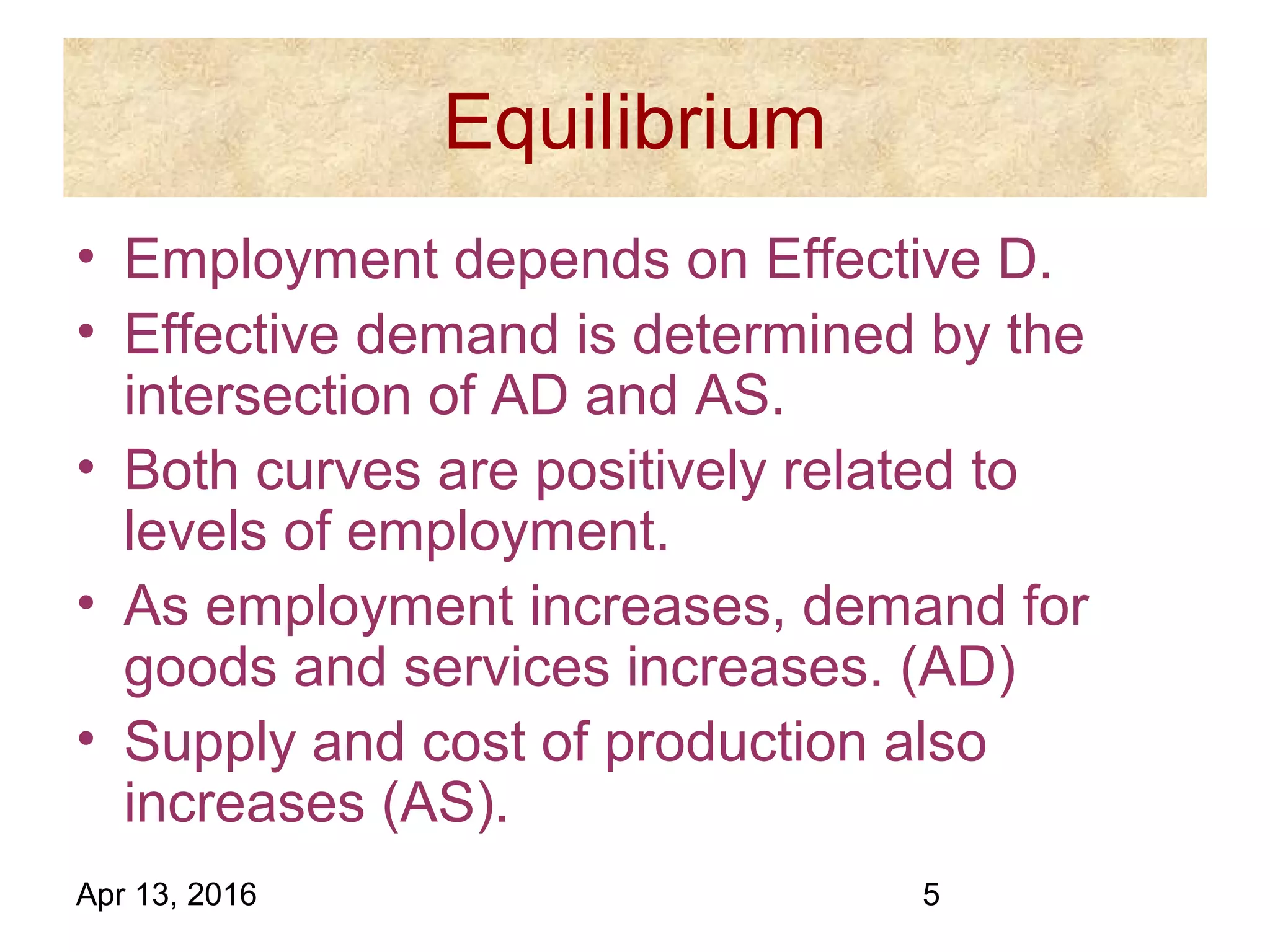

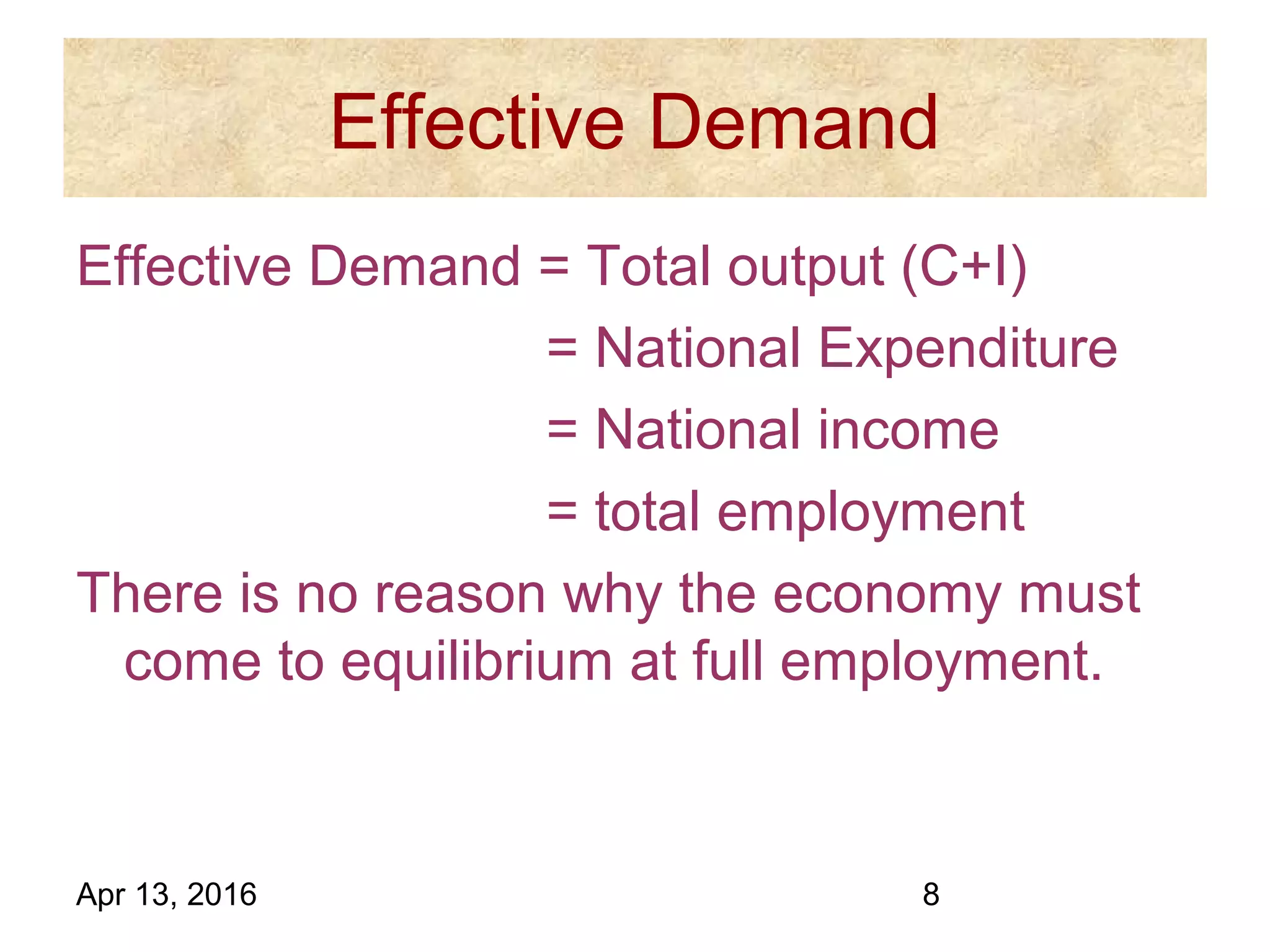

Effective demand refers to the total demand for goods and services in an economy, which includes consumption demand and investment demand. According to Keynes, effective demand determines the level of output and employment in an economy. Effective demand is low in capitalist systems because savings increase as income rises, creating a "leakage" out of the system that must be filled by investment in order to maintain output and employment levels. The economy reaches equilibrium at the point where aggregate demand and aggregate supply curves intersect, but this equilibrium may occur at less than full employment if investment is insufficient to make up the gap between income and consumption. The government therefore has an important role in managing aggregate demand to minimize unemployment.