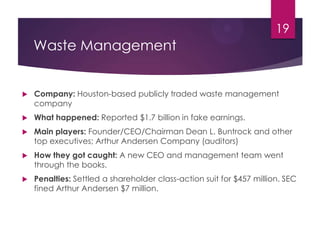

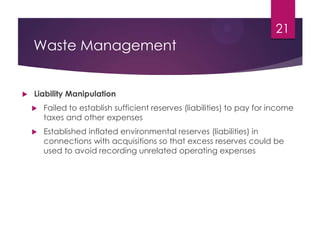

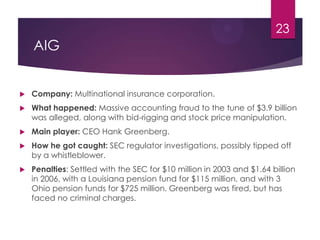

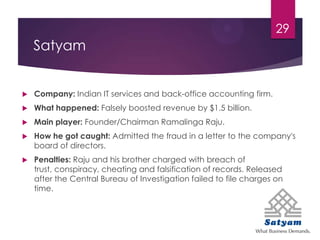

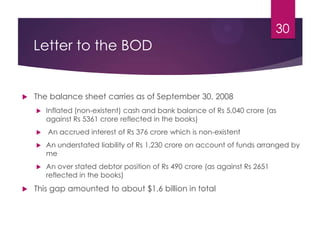

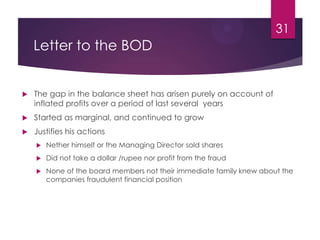

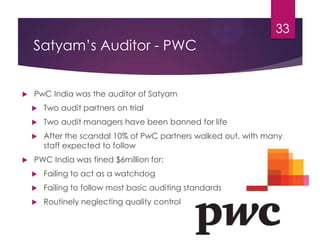

This chapter discusses various types of fraudulent schemes related to understating liabilities, overstating assets, and inadequate disclosure. It identifies schemes to underreport accounts payable, accrued liabilities, unearned revenue, and various types of debt. Asset fraud schemes involve overstating cash, receivables, inventory, fixed assets, and intangible assets. Disclosure fraud involves misrepresenting a company, its products, or omitting important information. Case studies of fraud at Waste Management, AIG, WorldCom, and Satyam are examined in relation to asset and liability manipulation.