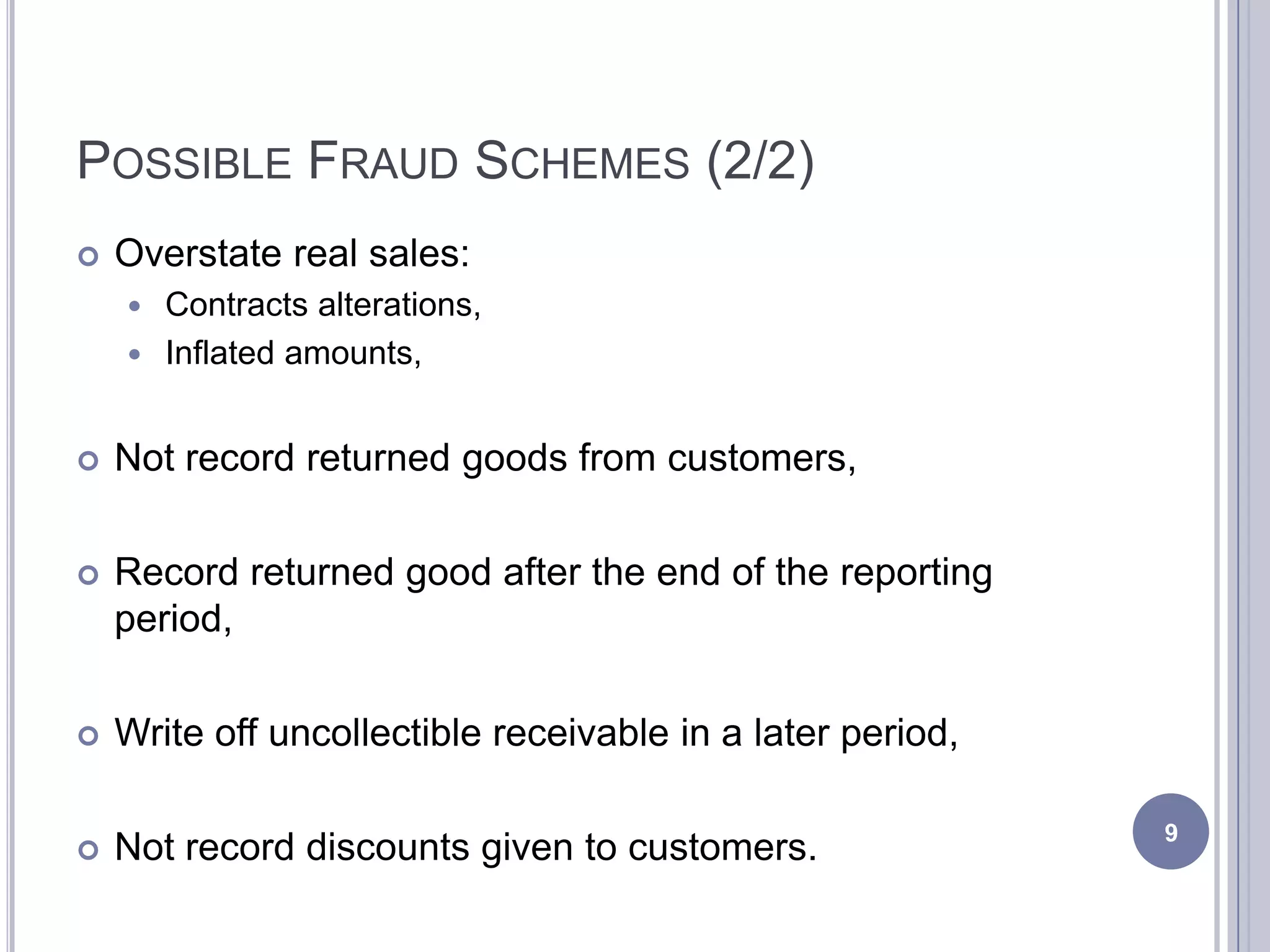

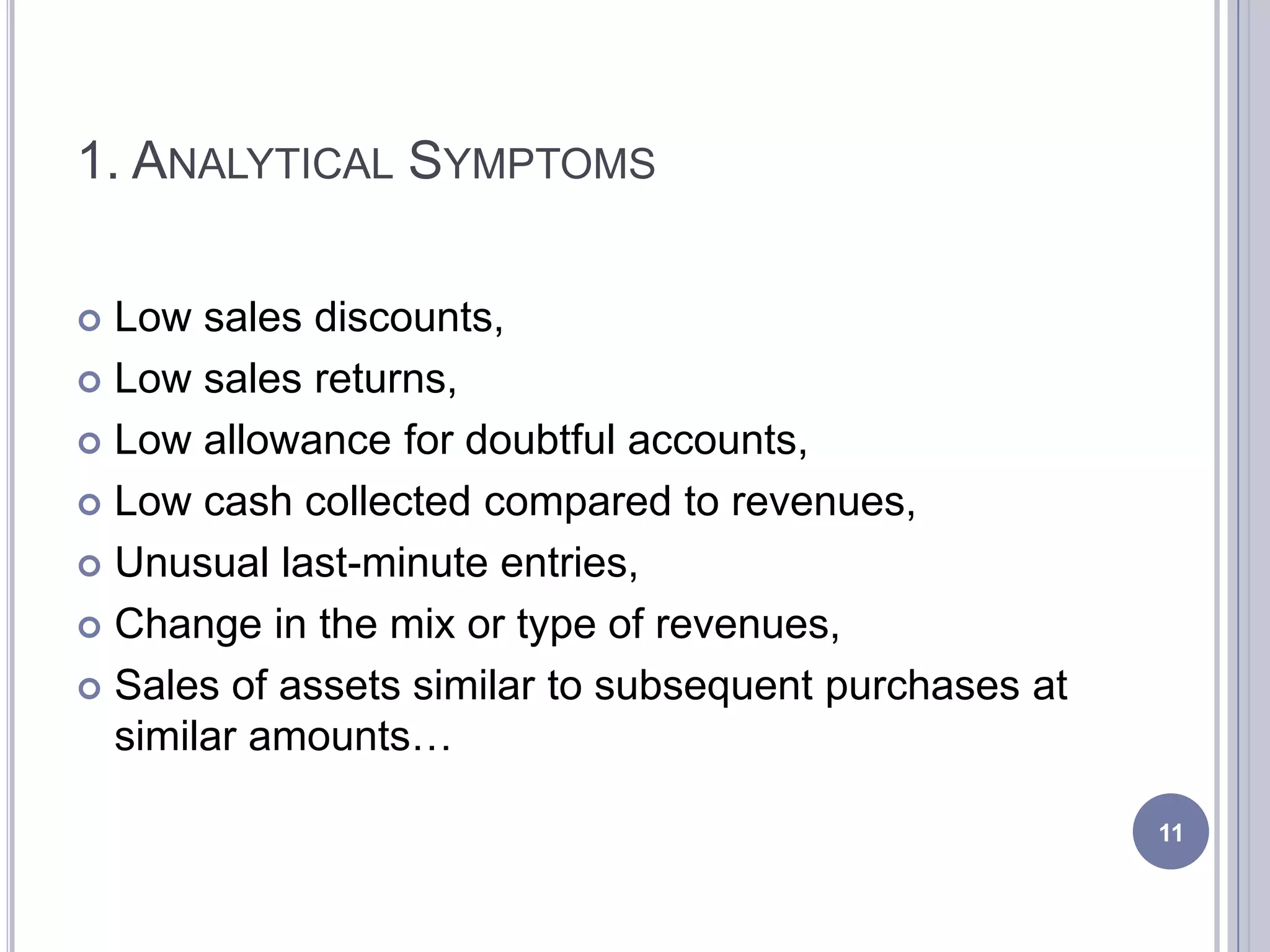

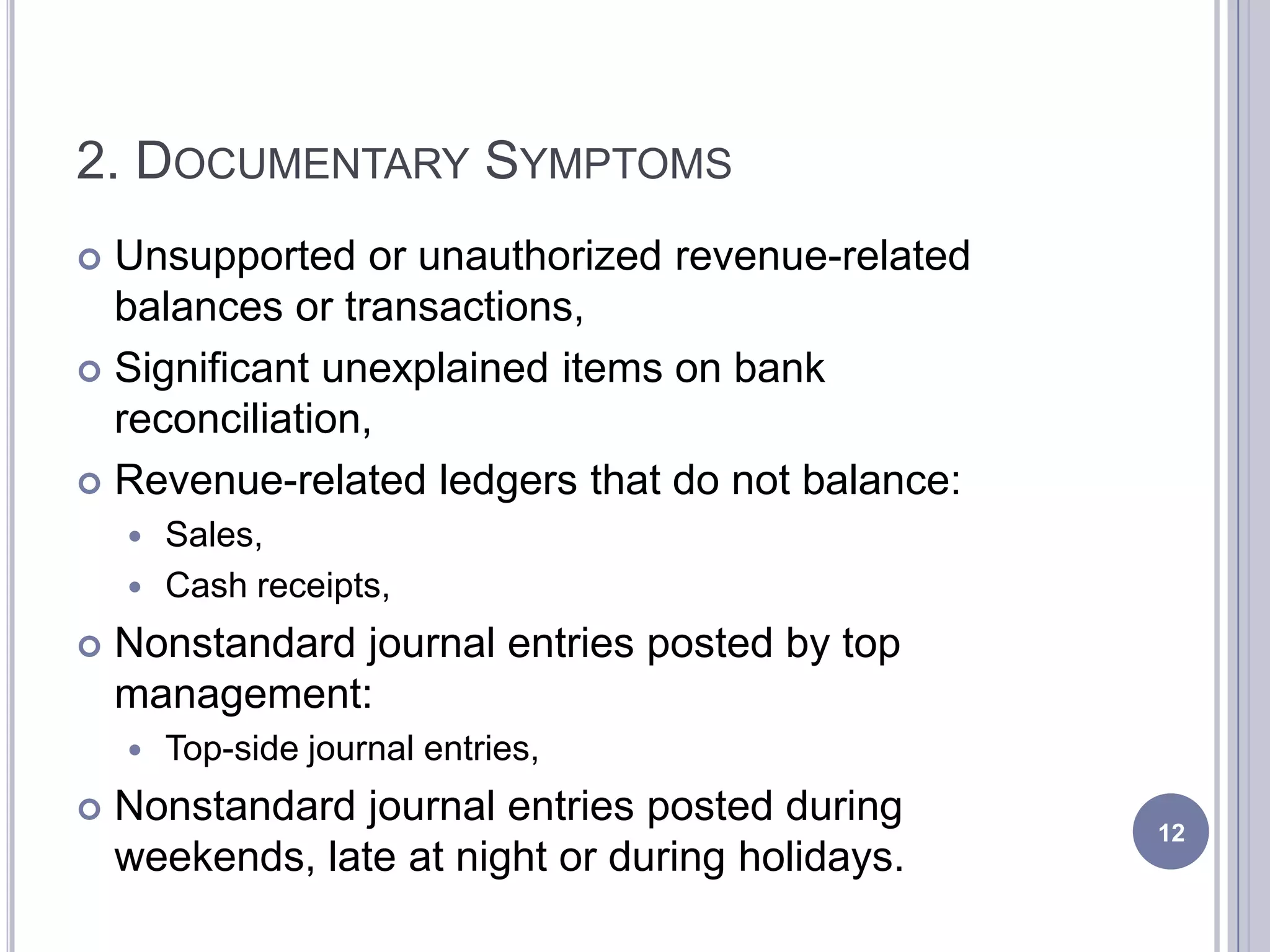

This document discusses revenue-related financial statement fraud. It begins by outlining key points and noting that over 50% of financial statement frauds involve revenue and receivables accounts. Common causes of this type of fraud include pressure to meet financial targets and easy manipulation of net income through revenues. Symptoms of revenue fraud are then categorized into six groups: analytical, documentary, control, behavioral, lifestyle, and tips/complaints. The Sunbeam Corporation case is provided as an example where a CEO created "cookie jar" reserves and overstated earnings.