Downloaded 68 times

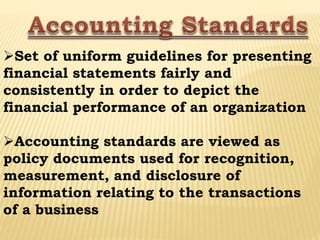

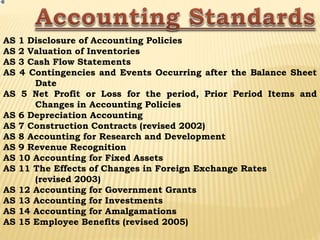

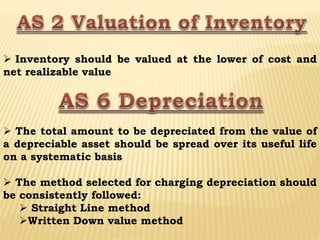

This document provides an overview of accounting standards and International Financial Reporting Standards (IFRS). It defines accounting standards as uniform guidelines for presenting financial statements consistently to depict an organization's financial performance. The document lists 32 Indian accounting standards and summarizes key points of AS 6 and AS 7 on inventory valuation and depreciation. It also explains that IFRS were developed to provide a global framework for financial reporting.