Download as PDF, PPTX

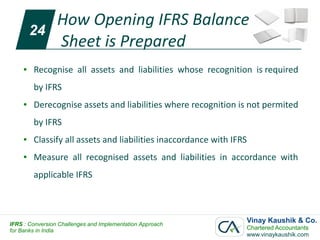

The document discusses the challenges of converting to IFRS for banks in India. It provides an overview of IFRS and the timeline for convergence in India. Banks with a net worth over 300 crores must converge their opening balance sheet as of April 1, 2013. Preparing the opening IFRS balance sheet involves recognizing all IFRS-compliant assets and liabilities, derecognizing any non-compliant items, and properly classifying everything. The document outlines the conversion process and comparative requirements under IFRS.