Download as PPS, PPTX

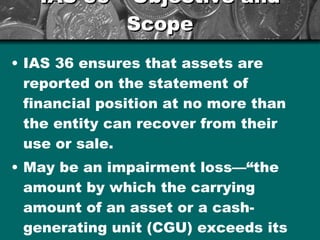

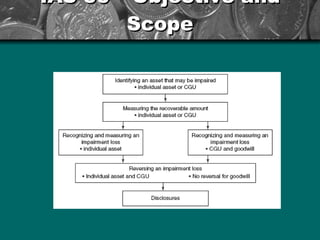

The document provides an overview of IAS 36 Impairment of Assets, including the standard's objective to ensure assets are reported at no more than their recoverable amount. It discusses identifying impaired assets, calculating recoverable amount, recognizing impairment losses, reversing impairments, and disclosure requirements. Examples are provided for testing assets and cash-generating units for impairment.